1. Weekly News

European Union and Ukraine

Ukrainian Sugar Exports to EU Halted After Quota Reached Early in 2024

Under the European Union's (EU) temporary trade liberalization measures for Ukraine, sugar is classified as a sensitive good, with import quotas set to manage specific volumes, according to recently released news from AgroPortal.ua. Once these quotas are reached, the European Commission (EC) returns to regular trade terms, including duties outlined in the Ukraine and the EU association agreement. In 2024, the quota for Ukrainian sugar exports was 262.6 thousand metric tons (mt). Due to a significant increase in export activity, this quota was used up by May-24, leading to a halt in Ukraine's sugar shipments to the EU. The following quota will become available in Jan-25.

Ukraine

Forecast for Ukraine's Sugar Production and Exports in 2024/25 Season

In the 2024/25 season, Ukraine is expected to produce between 1.6 to 1.7 million metric tons (mmt) of sugar, exceeding the country's estimated domestic consumption of 950 thousand mt. The surplus could lead to exports of 600 thousand mt to 750 thousand mt, particularly to the EU market. Ukrainian sugar holds a competitive edge due to lower production costs. The country's first sugar harvest began at the end of Aug-24, with average yields ranging from 35 mt/ha to 70 mt/ha.

India

India Plans to Extend Sugar Export Ban

India plans to extend its sugar export ban and raise domestic ethanol prices by Sep-24. Although no official reports have been made, the country's absence from the global market is anticipated to tighten global supply, driving up benchmark sugar prices in New York and the London Stock Exchange. India's sugar production is projected to fall to 32 mmt in the 2024/25 season, down from 34 mmt in the 2023/24 season, due to uneven rainfall in key regions such as Maharashtra and Karnataka.

India imposed a ban on sugar exports starting Oct-23. With limited production, the government is prioritizing ethanol production, aiming to raise ethanol blending in gasoline to 20% by 2025/26, from 13% to 14%. As part of this push, sugarcane juice and syrup will be permitted for ethanol production starting in Nov-24, and the ethanol purchase price is expected to increase by 5%. The global market will need Indian sugar exports by 2025, as Brazilian production is likely to decrease due to drought.

Brazil

Fires Damaged Sugarcane Crops in São Paulo

The sugarcane crops in São Paulo, Brazil, have been significantly damaged by fires. According to the Brazilian Sugarcane and Bioenergy Industry Association (UNICA), over 231.8 thousand hectares (ha) of sugarcane crops have been affected, impacting more than 75% of the region's sugarcane production. Mainly located in Ribeirão Preto, São José do Rio Preto, and São Carlos, the fires have caused substantial losses, aggravated by the ongoing drought. Consequently, consultancy firm Datagro has revised Brazil's sugarcane production estimates for the 2024/25 season to 593 mmt from 602 mmt in the previous estimate.

Brazil’s Sugar and Molasses Exports in Aug-24 Increased YoY in Volume but Decreased in Value

According to Brazil’s Secretariat of Foreign Trade (SECEX), the country’s sugar and molasses exports reached 3.925 mmt valued at USD 1.795 billion in Aug-24. This represents an 8.2% year-on-year (YoY) increase in volume and a slight 0.9% YoY drop in value. The average export price was USD 467/mt , marking an 8.4% YoY decrease from USD 499.4/mt in Aug-23.

Thailand

Thailand’s Sugar Production Reached 8.8 mmt in the 2023/24 Season

Thailand's sugarcane output reached 82.1 mmt in the 2023/24 season, producing 8.8 mmt of sugar. In the first half of 2024, the Thai market consumed 1.27 mmt of sugar. Therefore, the surplus will be used for export. Local sugar experts expect the country's sugarcane production in the 2024/25 season to increase within the range of 90 mmt to 100 mmt, resulting in sugar production rising to 9 mmt to 10 mmt.

2.Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

* Varieties: Refined sugar

Yearly Change in Sugar Pricing Important Producers (W36 2023 to W36 2024)

* Varieties: Refined sugar

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

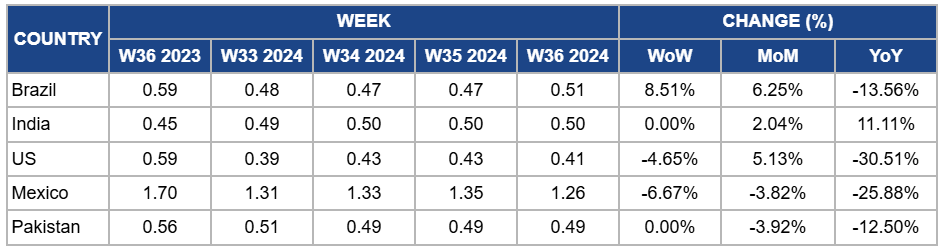

Brazil

In W36, Brazil’s sugar price rose 8.51% week-on-week (WoW) and 6.25% month-on-month (MoM) to USD 0.51 per kilogram (kg). This rise is attributed to supply disruptions caused by fires that have affected sugarcane plantations in critical regions of São Paulo. In addition, Brazil has been reducing ethanol production from sugarcane since Apr-24, aiming to benefit from rising sugar prices. Despite the short-term and medium-term price increases, the YoY prices declined by 13.56%, indicating weaker global demand amid higher supply from competing markets.

India

In W36, India’s sugar price held steady at USD 0.50/kg, showing no WoW change. However, MoM prices increased by 2.04%, and YoY prices surged by 11.11%. This price growth reflects global supply concerns following India's continued export ban and its focus on ethanol production. The anticipated increase in ethanol prices starting Sep-24 is expected to support domestic sugar prices further by reducing the availability of sugar for export.

United States

In W36, sugar prices in the United States (US) dropped by 4.65% WoW to USD 0.41/kg. Despite a 5.13% MoM increase, prices declined significantly by 30.51% YoY. The price drop reflects the impact of global supply factors, particularly Brazil’s production disruptions, which have added volatility to the market. The US has been diversifying its sugar sources, which has helped stabilize prices in the face of global market pressures.

Mexico

In W36, Mexico’s sugar price fell 6.67% WoW to USD 1.26/kg, contributing to a 3.82% MoM decline and a 25.88% YoY drop. The decrease is attributed to seasonal market adjustments and fluctuations in the Mexican peso against the US dollar. Mexico has been facing challenges in its sugar production due to climate change, but government efforts to improve sugarcane yields and replant vines could help mitigate these issues in the 2024/25 season.

Pakistan

In W36, Pakistan’s sugar price remained stable at USD 0.49/kg, with no WoW or MoM change, reflecting a 12.50% YoY decline. The price stabilization is mainly due to Pakistan's resumption of sugar exports and the availability of surplus sugar stock in the domestic market. These measures have alleviated pressures on sugar prices, helping maintain affordability for consumers despite external market volatility.

3.Actionable Recommendations

Invest in Fire Prevention and Optimize Sugarcane Export Strategies

To address the impact of fires and drought on sugarcane crops, Brazil should prioritize enhancing fire prevention measures, such as improving monitoring systems, creating firebreaks, and implementing stricter enforcement of land management practices. Additionally, investing in sustainable irrigation techniques will help mitigate the effects of drought. Brazil can also capitalize on the global supply gap by optimizing its export strategies, leveraging rising demand to secure better trade deals and increase revenue while balancing domestic needs.

Expand Diversified Sourcing and Stabilize Domestic Supply

The US should further diversify its sugar import sources to mitigate global price fluctuations and ensure a stable domestic supply. Expanding partnerships with countries like the Philippines and exploring additional trade agreements with sugar-producing nations will help counter the volatility caused by production disruptions in Brazil. Developing strategic sugar reserves could also serve as a buffer against future supply shocks.

Expand Diversified Sourcing and Stabilize Domestic Supply

Mexico needs to focus on improving sugarcane productivity and crop resilience to climate change through research into drought-tolerant varieties and the expansion of modern farming techniques. The government should support replanting initiatives and boost agricultural financing. By increasing local production and stabilizing domestic prices, Mexico can remain competitive in domestic and export markets.

Sources: Tridge, AgroPortal.ua, Voh, Noticias Agrícolas, Cultivar, Portal Do Agronegócio, Agrodigital