In W36 in the milk landscape, some of the most relevant trends included:

- A bearish sentiment has taken hold of the global dairy market, evidenced by a 4.3% drop in the GDT index and a 1.3% drop in the FAO Dairy Price Index, along with a widespread buyer retreat in the European dairy sector. This has translated into immediate price weakness for SMP in key European export-oriented markets.

- Structural consolidation in the European dairy industry is accelerating in response to tightening milk supplies, as seen in the Meggle-Rücker acquisition in Germany and FrieslandCampina’s plant closure in the Netherlands. These moves reflect a long-term trend towards greater efficiency and competition for a shrinking raw material base.

- The UK's dairy sector is demonstrating exceptional performance, with robust YoY growth in milk production and commodity exports continuing through late August. This strong supply base supported a 20% surge in export value in the first half of the year, driven by a successful strategic pivot to higher-value products and non-EU markets.

1. Weekly News

Global

Global Dairy Prices Weaken in August as Butter and Cheese Decline, SMP Rises

The Food and Agriculture Organization (FAO) Dairy Price Index registered its second consecutive monthly decline in Aug-25, falling by 1.3% to 152.6 points, though it remained a significant 16.2% above its value in Aug-24. The monthly decrease was primarily driven by softer international prices for butter and cheese. Butter prices fell by 2.5%, influenced by robust production in New Zealand and steady supplies from the European Union (EU), which boosted global availability while import demand from key Asian markets remained subdued. Similarly, cheese prices dropped by 1.8% as weaker domestic demand in Europe and softer import interest from Asia added downward pressure. Whole milk powder (WMP) prices also edged down slightly by 0.3%. In contrast, skim milk powder (SMP) prices moved against the trend, rising by 1.8%. This strength was attributed to limited exportable surpluses from New Zealand meeting steady demand from buyers in Southeast Asia, highlighting a divergence in global market dynamics across different dairy commodities.

Europe

European Dairy Prices Decline as Cautious Buyers and Strong Supply Create Pressure

European dairy markets are experiencing a significant downturn, with widespread price pressure on commodities across multiple commodity categories, especially cheese and butterfat, driven primarily by a strategic retreat from purchasing by major buyers. Procurement managers are reportedly delaying Q4-2025 purchases in anticipation of further price declines, creating a market with ample offers but very few bids. This buyer hesitation is compounded by strong global milk production, which continues to support high commodity output levels. For example, cheese output increased 1.52% in Europe in the first half of 2025 (H1-2025), with the United States (US) production increasing 1.66%, while New Zealand’s cheese exports surged 17.98%, leading to growing inventory levels for manufacturers. The impact is evident across various cheese categories, with prices for Gouda, Mozzarella, Emmental, and Cheddar all weakening significantly in recent weeks. The near-term outlook suggests continued price weakness, as robust global supply and intense export competition are expected to persist, rewarding patient buyers but posing significant challenges for European producers.

Germany

German Dairy Consolidation Continues as Meggle Buys Cheese Producer Rücker

German dairy company Meggle has announced the acquisition of fellow German cheese producer Rücker, a significant move that continues the trend of consolidation within the European dairy sector. The acquisition is a key part of Meggle's strategy to substantially expand its cheese business, a segment it has been actively growing since its 2021 purchase of Stegmann Emmentaler Käsereien from French cooperative Sodiaal. By acquiring Rücker, which generated USD 585 million (EUR 500 million) in revenue in 2024, Meggle gains one of Germany's largest private cheese producers, along with its extensive production capacity and expertise. Rücker processes approximately 700 million kilograms (kg) of milk annually to produce 90,000 metric tons (mt) of cheese, 20,000 mt of butter, and 20,000 mt of milk powder, and brings a portfolio of established northern German cheese brands into Meggle's fold. Rücker’s brand portfolio includes Rücker, known for northern German cheeses such as Alter Schwede, Alt-Mecklenburger, and Friesischer Hirtenkäse. Additional brands include oba and Waterkant for white cheeses, and Vega Lecker for plant-based offerings. The transaction, which is pending regulatory approval, will significantly bolster Meggle's position in the competitive European cheese market and expand its overall product offerings.

Netherlands

Shrinking Dutch Livestock Numbers Could Drive Growth of Hybrid Dairy Products

A forecast by Dutch bank ABN-AMRO of an 8% decline in the Netherlands' dairy cow population by 2030 is creating a significant strategic opportunity for hybrid dairy products, which blend traditional cow's milk with plant-based ingredients. According to ABN-AMRO, the shrinking domestic milk supply will put pressure on dairy processors, but innovating with hybrid products offers a way to add value and adapt to changing resource availability. This strategy is supported by consumer research showing that 35% of Dutch consumers are willing to try hybrid milk, primarily for environmental and health reasons, provided the price is comparable to conventional milk. This trend is already materializing in the Dutch retail sector, with major supermarket chain Albert Heijn recently launching its own line of hybrid milk products. The move targets consumers who seek a middle ground between conventional dairy and purely plant-based alternatives, offering a familiar taste profile with perceived sustainability benefits.

Shrinking Dutch Herd Drives Dairy Plant Consolidation and Higher Consumer Prices

The 8% forecasted decline in the Netherlands' dairy cow population by 2030 is also driving significant consolidation within the processing sector, a trend highlighted by FrieslandCampina's recent closure of its Den Bosch butter factory, which produced two million packs of butter weekly. The shrinking national herd, a result of government-led farm buyout schemes, is creating overcapacity among dairy processors, forcing them to restructure. FrieslandCampina's decision to consolidate its butter production into a new, more sustainable facility in Lochem exemplifies the industry's response: shutting down older or less efficient plants to align processing capacity with the reduced raw milk supply. This reduced supply of domestic milk and subsequent industry restructuring will have a direct impact on Dutch consumers in the form of continued price increases for dairy products such as cheese, milk, and butter on supermarket shelves in the coming years.

United Kingdom

UK Milk Deliveries Show Continued Strong YoY Growth

Milk production across Great Britain remains robust, with daily deliveries for the week ending August 30 running 5.1% higher than the same week last year, according to the latest data from Agriculture and Horticulture Development Board (AHDB). Deliveries are up 0.9% week-on-week (WoW) and averaged 33.57 million liters (L) per day. This strong performance continues a consistent trend of year-on-year (YoY) growth seen throughout the summer months. In Jul-25, Great Britain's monthly milk deliveries totaled 1,067 million L, a 4.3% increase compared to Jul-24, while the year-to-date (YTD) figure (since Apr-25) is up by 5.3%. The data for the entire United Kingdom (UK) shows an even stronger trend, with Jun-25 deliveries up by 6.3% to 1,357 million L, driven by particularly high growth in Northern Ireland (+9.5%). The AHDB estimate for Jul-25 UK production is 1,308 million L. The sustained increase in milk flow provides ample raw material for the UK's dairy processing sector, supporting both domestic supply chains and the country's export capabilities. This increased availability is a key factor for the UK market, especially as it contrasts with reports of tightening milk supplies in other parts of Europe.

GB Organic Milk Production Shows Substantial Year-on-Year Growth

Organic milk production in Great Britain (GB) is demonstrating substantial YoY growth, with daily deliveries for the week ending August 30 increasing by 8.7% compared to the same week in 2024. Deliveries are up 1.9% WoW and averaged 915,700 L per day. This recent surge is part of a sustained upward trend throughout 2025. According to the latest AHDB data, monthly organic deliveries in Jul-25 were up 8.0% YoY, reaching 29.1 million L. The cumulative data for the season YTD (since Apr-25) is even more striking, showing a remarkable 12.2% increase in organic milk volumes compared to the previous year. This significant expansion in the organic milk pool points to strong consumer demand and successful efforts by farmers to scale up production. The growth provides processors with a greater volume of high-value raw material, enabling them to expand their organic product lines to meet rising market demand.

UK Dairy Export Value Jumps 20% in H1-2025 on Strong Non-EU Growth

UK dairy exports showed strong growth in H1-2025, with the total value of shipments rising by 20% to USD 1.49 billion (GBP 1.1 billion), significantly outpacing a 2.5% increase in volume at 688,800 mt. This performance was primarily driven by a surge in exports of milk powders and whey products, which saw volume increases of 28.3% and 26.6% respectively, reaching two-year and five-year highs. Crucially, this growth was led by a strategic expansion into non-EU markets, with milk powders increasingly destined for nations in Africa and Asia, while whey products found new buyers in New Zealand, the US, China, and the Philippines. While some categories like cheese (-0.7%), milk and cream (-0.9%), and yoghurt (-16%) saw slight volume declines, the overall strong performance, particularly in high-value powders, positions the UK well to capitalize on forecasts of rising global dairy demand. However, continued success will depend on the UK dairy industry’s ability to navigate an increasingly competitive global market.

2. Weekly Pricing

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W36 2024 to W36 2025)

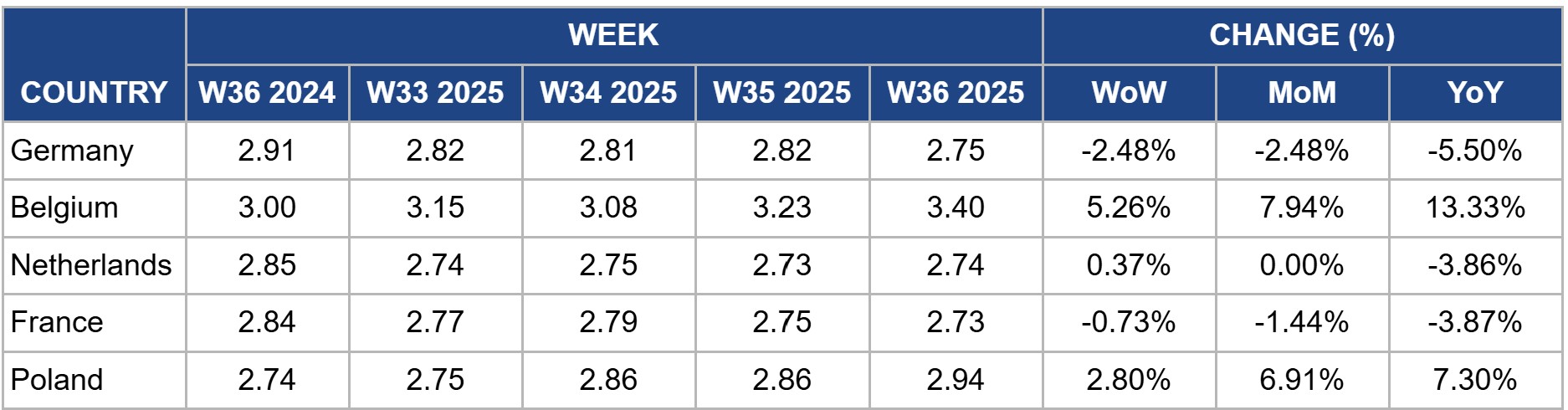

Germany

In Germany, the price of SMP was USD 2.75/kg in W36, a sharp decrease of 2.48% WoW and 2.48% month-on-month (MoM), pushing the price to 5.50% below its level YoY. The German market experienced a significant downturn, erasing the firming trend seen in recent weeks. This sharp price drop is a direct reaction to the negative sentiment in the international market, highlighted by the 4.3% fall in the Global Dairy Trade (GDT) index in early Sep-25 and reports of a widespread price decline in the European dairy sector. With buyers reportedly retreating in anticipation of further price drops, the German market, which is highly sensitive to export demand, has come under immediate pressure. The significantly negative YoY performance indicates that weak international demand is now heavily outweighing any domestic supply tightness.

Belgium

In Belgium, the price of SMP surged to USD 3.40/kg in W36, a substantial increase of 5.26% WoW and 7.94% MoM, contributing to a 13.33% YoY rise. The Belgian market is a clear outlier, completely defying the bearish trend seen elsewhere in western Europe. This exceptional price strength is driven almost entirely by acute domestic supply constraints, with raw milk deliveries and SMP production having fallen significantly YTD. As post-holiday demand continues to return, buyers are competing for a limited local supply, forcing prices higher. Belgium's price action demonstrates a market where severe local shortages are currently insulating it from the immediate impact of weaker international sentiment, keeping its prices at a significant premium.

Netherlands

In the Netherlands, the price of SMP was USD 2.74/kg in W36, a slight increase of 0.37% WoW, but flat MoM and down 3.86% YoY. The Dutch market remains stagnant, showing neither the sharp decline seen in Germany nor the surge in Belgium. The modest WoW uptick suggests a minimal return of demand, but the flat MoM figure indicates a lack of any real upward momentum. The market appears to be caught between conflicting forces: a tightening domestic milk supply is providing some price support, but this is being effectively neutralized by the weak international outlook, confirmed by the recent poor Global Dairy Trade (GDT) auction results, and intense competition among domestic processors.

France

In France, the price of SMP was USD 2.73/kg in W36, down 0.73% WoW and 1.44% MoM, pushing the price to 3.87% below its level YoY. The French market continues to soften, unable to find a floor. The price weakness is likely a result of two compounding factors: lingering market uncertainty and logistical issues following the Lumpy Skin Disease (LSD) outbreak, combined with the new wave of bearish sentiment sweeping across Europe. The downturn in the international cheese and SMP markets is preventing any potential price recovery, and the market's fundamentals are now being overshadowed by these negative short-term pressures, as reflected in the significant negative YoY price.

Poland

In Poland, the price of SMP rose to USD 2.94/kg in W36, an increase of 2.80% WoW and 6.91% MoM, resulting in a strong 7.30% YoY gain. After stabilizing last week, the Polish market is now showing significant strength, largely defying the bearish international news from the recent GDT auction. This upward momentum is likely being driven by a surge in demand from key export destinations. In particular, strong purchasing activity from Algeria, one of Poland’s largest markets for milk powders, is believed to be a primary catalyst. This aligns with recent trade data from other European exporters, such as the UK, which has also reported a significant increase in milk powder shipments to Algeria, indicating robust demand that is currently overriding the weaker sentiment seen in other European markets.

3. Actionable Recommendations

Leverage Current Market Weakness for Short-Term Gains

The current dairy market is decidedly bearish, with falling prices at GDT auctions in early Sep-25 and a clear retreat from purchasing in the European dairy sector creating a significant short-term opportunity for buyers. Where possible, procurement managers should shift their purchasing strategy to capitalize on this weakness by avoiding getting locked into long-term contract commitments and focusing on the spot market for immediate needs. This hand-to-mouth approach allows businesses to take full advantage of potential further price declines, reducing input costs and improving near-term margins. By remaining patient and disciplined in this buyer's market, companies can optimize their purchasing costs before sentiment inevitably shifts. This strategy is about maximizing gains from the current downturn by maintaining flexibility and resisting the urge to lock in volumes too early. However, this strategy should not be executed at the cost of long-term partnerships and volumes, especially in the ever-decreasing supply of the European market.

Intensify Non-EU Focus to Counteract European Market Weakness

While the broader European dairy market is showing signs of price and supply issues, the UK is in a position of relative strength, with robust milk production growth and a highly successful export performance in H1-2025. The 20% surge in export value was driven by expanding trade in powders and whey to non-EU nations in Asia and Africa. UK exporters should double down on this proven strategy to insulate themselves from the current downturn in continental Europe. This is an ideal time to invest in building relationships in these high-growth markets, leveraging the UK’s ample milk supply to guarantee volumes and secure long-term contracts. By further diversifying away from the increasingly volatile EU market and cementing its position as a key supplier to these emerging regions, the UK dairy industry can sustain its growth trajectory.

Prioritize Consolidation and Innovation to Survive Supply Squeeze

The future of the European dairy sector holds increased consolidation and an ever-growing battle for milk supplies. The acquisition of Rücker by Meggle and the closure of a FrieslandCampina plant are not isolated events but signals of an accelerating trend. All European processors, particularly small to mid-sized operations, must urgently review their long-term strategic viability. This requires a two-pronged approach. First, realistically assess operational efficiency and scale; if vulnerable, proactively explore modernization and increased efficiency, strategic partnerships, mergers, or a sale to a larger entity. Second, invest in innovation to create higher-value products from an increasingly limited milk pool. The emergence of hybrid dairy products is a prime example of adapting to new market realities. Cooperatives and processors that fail to either improve efficiency, consolidate, or innovate risk being left behind.

Sources: Tridge, AHDB, Dairy Industries International, ABC.az, Green Queen, Just Food, Vesper, FAO