In W44, butter prices in Europe and the US showed mixed short-term movements but continued to trend lower MoM and YoY. Overally, European butter markets remain subdued due to cautious buyers, stable production, rising cream availability, and sufficient inventories. In the US, butter prices and futures saw slight weekly gains but significant monthly and yearly declines, driven by higher milk output, ample cream supplies, and weaker export demand. Globally, the FAO dairy price index fell in Oct-25, with butter prices dropping amid increased export availability from the EU and New Zealand and softened demand from Asia and the Middle East. The November 4 GDT auction mirrored this trend, with near-term contracts falling the most. Market strategies for buyers, processors, and exporters include securing long-term supplies, diversifying customer bases, developing value-added products, and aligning production with seasonal demand spikes.

1. Weekly Price Overview

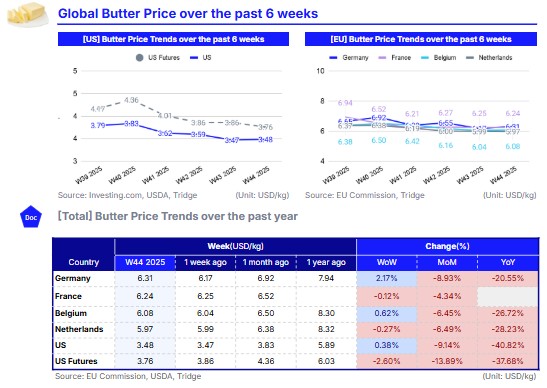

Cautious Buying and Softer Demand Keep Butter Markets Subdued in Europe and the US

In W44, butter prices in Germany averaged USD 6.31 per kilogram (kg) up 2.17% week-on-week (WoW) but down 8.93% month-on-month (MoM) and 20.55% year-on-year (YoY). Belgian butter prices stood at USD 6.08/kg, a modest 0.62% WoW rise but remaining 6.45% MoM and 26.72% YoY lower. In contrast, French butter averaged USD 6.24/kg, a slight 0.12% WoW drop and a 4.34% MoM decline. However, when measured in euros, French prices were 0.15% higher WoW at EUR 538.01/100kg, highlighting the effect of currency fluctuations. Meanwhile, Dutch butter slipped 0.27% WoW to USD 5.97/kg, though prices remained stable in local terms at EUR 515.0/100kg.

Overall, European butter prices have been fluctuating over the past month, reflecting subdued market activity as buyers remain cautious amid softer demand. Production levels are stable, cream availability continues to build, and inventories are sufficient to meet near-term needs.

In the United States (US), butter prices averaged USD 3.48/kg, a 0.38% WoW increase but a 9.14% MoM drop and a significant 40.82% YoY decline. Similarly, US butter futures fell 2.60% WoW to USD 3.76/kg, down 13.89% MoM and 37.68% YoY. The pronounced MoM and YoY declines suggest that improved milk output, ample cream supplies, and weaker export demand have expanded domestic butter stocks, driving a market correction from last year’s elevated levels. The slight WoW gain likely reflects short-term or seasonal demand ahead of the holiday period, though overall market sentiment remains bearish compared to 2024.

2. Price Analysis

Global Dairy Prices Decline as Ample Supplies and Weak Import Demand Pressure Markets

According to the Food and Agriculture Organization (FAO), the global dairy price index averaged 142.20 points in Oct-25, representing a 3.42% MoM decline, with all major dairy commodities recording price drops. Specifically, the butter price index fell, averaging 184.80 points, down 6.46% MoM. This decline was mainly driven by ample export availability from the European Union (EU) and New Zealand, where favorable seasonal temperatures supported milk production, while import demand from Asia and the Middle East weakened.

The FAO findings are consistent with the fortnightly held Global Dairy Trade (GDT) auction, where butter prices averaged USD 6,371 per metric tons (mt) in the November 4 event, marking a 4.3% decrease. At the event, butter prices declined across all available contracts, with near-term ones experiencing the sharpest drops, with Dec-25 contracts falling by 4.8%, while Jan-26 contracts declining by 5.5%. North Asia accounted for 73% of total butter purchases, highlighting the region’s continued, though price-sensitive, demand.

The United States Department of Agriculture (USDA) indicates that export interest in the EU remains subdued, with only light inquiries from Asia, the Middle East, and the US. The quiet demand reflects steady production schedules and rising cream availability, which continue to expand exportable supplies. In Oceania, export demand remains stable, but strong competition from the US and Europe is keeping market prices under pressure.

3. Strategic Recommendations

Leverage Market Opportunities While Managing Butter Price Volatility

Given the persistent MoM and YoY declines in butter prices across Europe and the US, buyers and processors can take advantage of the lower price environment by securing long-term supply contracts with reliable producers in the EU, the US, and Oceania. This ensures stable access and reduces exposure to short-term volatility. Exporters in Europe and New Zealand should diversify their customer base beyond traditional Asian and Middle Eastern markets. They can target regions with stable but price-sensitive demand, such as North Asia, which accounted for 73% of butter purchases at the recent GDT event.

To address subdued domestic demand and rising cream availability, processors and manufacturers can focus on value-added or blended butter products. Flexible production schedules will allow them to respond quickly to market fluctuations. Additionally, monitoring seasonal demand spikes, such as holiday periods, and aligning sales and marketing efforts can help capitalize on short-term price increases.