.jpg)

1. Weekly News

Europe

European Potato Production Update

Potato producers in Germany, France, Belgium, and the Netherlands expanded their harvest area by 7% year-on-year (YoY) in 2024, yielding a record 22.7 million metric tons (mmt), surpassing the five-year average. Germany recorded its highest-ever harvest at 12.7 mmt, while Poland's output is expected to rise modestly from 5.6 mmt to 5.8 mmt. However, Hungary experienced a contrasting trend, with both cultivation area and production declining significantly. Over the past decade, Hungary's potato production has dropped by 70%, leading to a domestic shortage. Despite this, potato prices in Hungary have fallen 15% YoY, whereas the price of imported French potatoes has seen a more modest decline of 7%.

Germany

German Potatoes Gain Market Share Over Dutch Potatoes

German potatoes are increasingly displacing Dutch potatoes in the chip processing industry. Between Jul-24 and Oct-24, Dutch chip factories imported 630.5 thousand metric tons (mt) of potatoes, primarily from Germany, marking a 9% YoY increase. This rise underscores Germany's growing influence in Dutch and Belgian potato markets. In contrast, the processing of Dutch potatoes has declined significantly, with only 580.3 thousand mt processed, a 16% decrease YoY. Dutch farmers supplied 110.7 thousand mt fewer potatoes to factories than the previous season, signaling a tightening domestic supply. Overall, potato processing in the Netherlands totaled 1.2 mmt in 2024, 4.6% less than the last year.

Greece

Greek Potato Season Ends Early Due to Reduced Planting and Drought

Greece's 2024 potato season is ending earlier than usual, particularly in the Nevrokopi region, due to a combination of reduced planting areas, severe drought, and abnormally high temperatures last summer. The planting area was halved from 1,700 hectares (ha) to around 850 ha, and water shortages made it difficult for producers to maintain harvest volumes. As a result, potatoes began to sprout earlier than usual, reducing their shelf life. Despite these challenges, high demand for yellow varieties from wholesalers has helped stabilize the market, and producers have found buyers.

Russia

Russia's Plans to Boost Potato Imports Due to Declining Domestic Production

Russia plans to increase potato imports from Egypt, Azerbaijan, China, and Pakistan to offset a forecasted decrease in domestic production. From Jan-24 to Apr-24, Russia imported 56.9 thousand mt of food potatoes, with Egypt contributing 85.3% of these imports, highlighting its dominant role as a supplier. Despite a record-breaking harvest of over 8.5 mmt in 2023, Russia's 2024 potato production is forecasted at 7.3 mmt, a decline attributed to adverse weather conditions. This figure aligns with the harvest levels of 2021 and 2022. The Deputy Prime Minister instructed the Ministry of Economic Development and Agriculture to explore increased imports from friendly countries to meet the anticipated demand.

Ukraine

Ukrainian Potato Prices Stabilized Due to Increased Imports

Due to increased imports, potato prices in Ukraine have stabilized at USD 0.55 to 0.60 per kilogram (kg). The summer heat significantly reduced the domestic vegetable and potato harvest, prompting reliance on external supplies. The Deputy Chairman of the All-Ukrainian Agrarian Council highlighted that the increased supply from imports has played a crucial role in stabilizing prices, especially for vegetables like potatoes. He also noted that prolonged dry conditions severely impacted the availability of local produce on store shelves, though some farms are still completing their harvest. This import-driven stabilization has helped mitigate the effects of a challenging growing season, ensuring market balance despite adverse weather conditions.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W47 2023 to W47 2024)

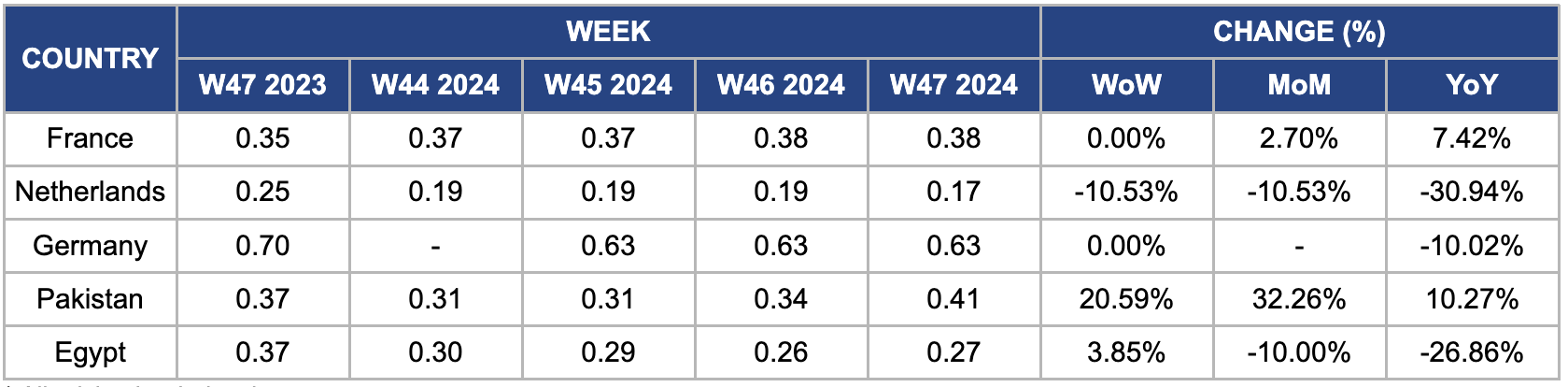

France

In W47, wholesale potato prices in France remained stable week-on-week (WoW) at USD 0.38/kg but saw a 2.70% rise month-on-month (MoM) and a 7.42% YoY increase. This price surge can be due to several factors, including rising production costs, declining yields, and challenges like climate change, wireworms, and chemical bans. These issues resulted in the loss of 11 thousand ha of potato cultivation in the latest season. Moreover, heavy rainfall during the harvest season downgraded yields and led to discarding large quantities of potatoes. With 97% of the harvest completed from a record 177 thousand ha, France's potato supply was further constrained, tightening the market.

Netherlands

In W47, wholesale potato prices in the Netherlands decreased by 10.53% WoW, 10.53% MoM, and 30.94% YoY, reaching USD 0.17/kg. This year's potato season in Europe has been particularly difficult for farmers, beginning with an insufficient seed supply that led to rising seed prices. The weather worsened the situation, with heavy rainfall delaying planting and harvesting. Research suggests that climate change is intensifying the hydrological cycle, increasing the frequency of extreme precipitation events, and raising flood risks. The European potato sector is projected to experience a nearly 9% YoY decrease in production this year, with the Southern Netherlands seeing severe impacts due to prolonged rainfall, which extended the planting window beyond the typical 10-week period.

Germany

In W47, wholesale potato prices in Germany remained stable WoW at USD 0.63/kg, though there was a significant 10.02% YoY decrease. A bumper harvest of 12.7 mmt drove this stability in 2024, a 9% YoY increase and 17% above the five-year average. Supported by a 9% expansion in planting areas, this surplus is expected to push prices down, particularly for smaller sack sizes. Despite challenges like late diseases linked to weather conditions, the harvest is considerably larger than last year's. However, potato consumption in Germany has declined, with a 28% decrease since 1990, as consumers increasingly shift towards rice and pasta.

Pakistan

In W47, wholesale potato prices in Pakistan surged 20.59% WoW, 32.26% MoM, and 10.27% YoY, reaching USD 0.41/kg. This price increase is due to several factors, including a 25% reduction in seed availability due to currency depreciation raising production costs. Rising export demand from regional markets such as Afghanistan and the Middle East has further strained domestic supplies. Logistical challenges, compounded by localized supply shortages, have also pushed prices upward.

Egypt

In W47, Egypt's wholesale potato prices rose by 3.85% WoW to USD 0.27/kg. This increase can be due to several factors, including lower potato yield, which dropped from 14 to 16 mt per acre in 2023 to 9 to 12 mt per acre in 2024. This decline is partly due to climate change and a shortage of United States (US) dollars, which has affected potato seed imports. Moreover, while supply is expected to rise as more winter crops come to market, the reduced yield in the short term has led to the price increase. Other factors, such as economic challenges like high inflation and currency depreciation, have also contributed to higher costs in the potato sector.

3. Actionable Recommendations

Explore New Export Markets

Facing domestic challenges such as declining yields and increasing production costs, French and Hungarian potato producers should look to diversify their export markets to offset domestic shortfalls. Despite domestic declines, Hungarian exporters could explore niche markets that require specific potato varieties, such as premium or organic potatoes. This strategy could help tap into premium segments in the EU or even beyond, to markets in the Middle East or North Africa, where demand for quality potatoes is rising. By exploring and entering new export markets, French and Hungarian producers can mitigate the impact of domestic supply challenges, enhance their profitability by targeting higher-value segments, and reduce dependence on declining domestic markets. This would also help stabilize the market by offsetting local production issues with a diversified export strategy.

Leverage Climate Resilience Practices

Greek, Dutch, and French potato producers should invest in climate-resilient farming practices and varieties to safeguard future yields. In regions like Greece, where drought has significantly reduced planting areas, introducing drought-tolerant potato varieties and improving irrigation systems could help mitigate future challenges. Similarly, in the Netherlands and France, where heavy rainfall and flooding have damaged crops, utilizing advanced drainage systems and adjusting planting calendars could help reduce the risk of yield losses. Precision agriculture technologies could optimize water use and minimize crop vulnerability to extreme weather. By adopting climate-resilient farming practices, potato producers can protect their harvests from adverse weather conditions, reduce potential losses, and stabilize their supply, ensuring they can consistently meet domestic and export demands.

Expand Strategic Sourcing for Potato Exports

Potato producers and exporters in Poland, Russia, and Egypt should diversify their sourcing strategies to mitigate production shortfalls. As countries like Russia and Egypt face declining domestic potato production, there is an opportunity for other major producers like Germany, the Netherlands, and Poland to supply these markets with quality potatoes. Russian potato production is forecast to decrease due to adverse weather. Egypt is experiencing a drop in yields due to climate change and currency depreciation, which will drive the need for imports. By strengthening export relationships with these regions and ensuring a stable supply of potatoes, exporters can fill the gaps in the market and capitalize on rising demand for potatoes in the short and medium term. Expanding exports to countries with forecasted supply deficits will help producers tap into new markets, stabilize their revenues, and create long-term trade agreements that buffer against potential regional disruptions.

Sources: Ahdb, AkkerbouwActueel, Nieuwe Oogst, Vedomosti, East Fruit, Mezo Hir