W48 2024: Wheat Weekly Update

.jpg)

1. Weekly News

Global

Global Wheat Harvest Forecast Hits Record 794.7 MMT Despite Regional Reductions

The United States Department of Agriculture (USDA) forecasts a record global wheat harvest of 794.7 million metric tons (mmt) for the 2023/24 season, reflecting a 0.6% year-on-year (YoY) increase. Russia noted crop reductions down 0.5 mmt to 88.1 mmt. Meanwhile, Brazil was down 0.5 mmt to 8.5 mmt, Argentina was down 0.5 mmt to 17.5 mmt, while Kazakhstan and the United Kingdom (UK) saw production gains. Global wheat export expectations were slightly adjusted, with decreases for Kazakhstan from 10.5 mmt to 10 mmt and Brazil from 3 mmt to 2.9 mmt. Wheat exports from Russia and the European Union (EU) remain stable at 48 mmt and 30 mmt, respectively, while Ukraine's exports are expected to stay at 16 mmt, down from 18.6 mmt last season.

Canada

Western Canadian Wheat Farmers Optimistic as 2024 Harvest Surpasses Expectations

Western Canadian wheat farmers are optimistic about the 2024 harvest, with the New Wheat Crop Report showing a resilient and high-quality crop despite challenges. Wheat production reached 34.3 mmt, 4% larger than last year and 8% larger than average, driven by solid yields for non-durum and durum wheat. Durum wheat production notably surged to 6 mmt, thanks to favorable early conditions across Alberta and Saskatchewan, which helped the crop withstand hotter, drier conditions later in the summer. Saskatchewan, Alberta, and Manitoba all experienced solid production. The Canadian Western Red Spring wheat crop achieved average protein content, with a high percentage grading as number one or two, meeting customer expectations. Global demand for Canadian wheat is strong, fueled by its high grading and consistent quality. Investments in agronomy and genetically advanced wheat varieties have helped sustain the competitiveness of Canadian wheat, bolstering its reputation for adaptability, quality, and economic impact.

Russia

Russia’s Wheat Exports to Kenya Surged

Russia has emerged as a critical supplier of wheat to Kenya, with the former exporting 820,700 metric tons (mt) to the latter by mid-Nov-24 in the 2024/25 season. Russian wheat has fulfilled 60% of Kenya’s estimated 2.6 mmt import needs in 2023. Wheat exports to Kenya have steadily increased, climbing from 1.1 mmt in the 2022/23 season to 1.5 mmt in 2023/24. Although Kenya accounts for only 4% of Russia’s total wheat exports, it plays a vital role in Russia's strategic efforts to ensure food security, underscoring Kenya's growing significance in the Russian wheat trade.

United Kingdom

UK Wheat Area to Increase 5% for 2025 Harvest

The UK's wheat area is forecasted to rise 5% for the 2025 harvest, driven entirely by winter wheat expansion following challenging weather in 2024. The projected wheat area of 1.61 million hectares (ha) remains below the 2019 to 2023 average of 1.71 million ha, while spring wheat plantings are expected to halve due to improved autumn conditions.

United States

US Winter Wheat Condition Improves to 55%, Surpassing Last Year’s Levels

The condition of United States (US) winter wheat improved significantly in W48. The share of wheat rated in good to excellent condition rose by 6 %, reaching 55%, up from 49% the previous week. This follows a similar improvement the week before when the rating climbed 5% from 44%. In comparison, only 50% of the crop was rated good to excellent at the same time last year, indicating a notable improvement in crop health this season.

2. Weekly Pricing

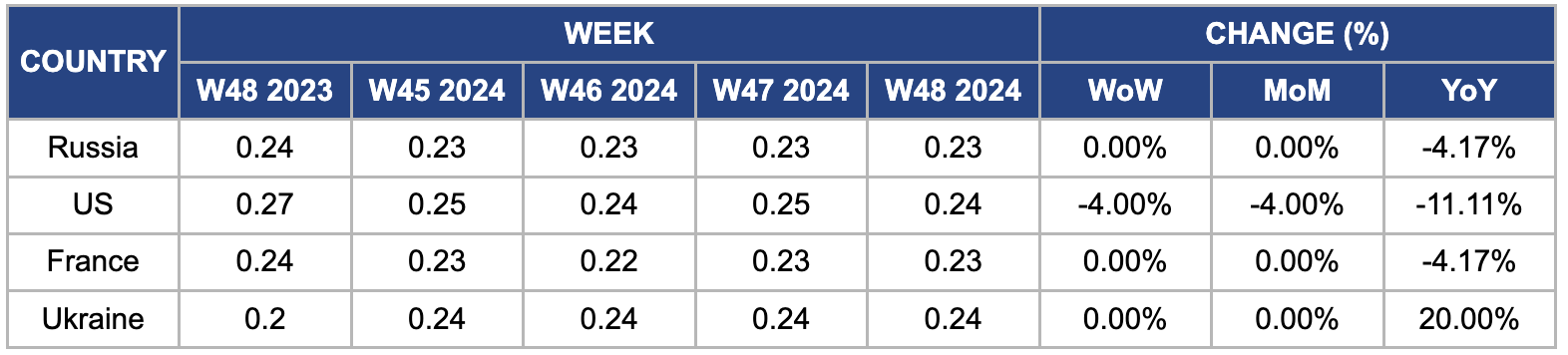

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W48 2023 to W48 2024)

Russia

In W48, Russian wheat prices remained stable on a week-on-week (WoW) basis but declined by 4.17% YoY, reaching USD 0.23 per kilogram (kg). The 2025 wheat harvest forecast was revised by 1.5 mmt to 81.6 mmt, primarily due to a revised winter wheat forecast of 54.3 mmt. This increase is due to a higher harvested area of 15.43 million ha and an improved yield forecast of 3.52 mt/ha, driven by favorable growing conditions in Southern Russia. The forecast for spring wheat production remains unchanged at 27.3 mmt. However, wheat prices dropped due to low international demand and new export regulations to control domestic prices.

United States

In W48, wheat prices in the US fell by 4% WoW and 4% month-on-month (MoM), reaching USD 0.24/kg. This decline followed improved crop conditions in the US. The country has seen a significant increase in winter wheat conditions and exports. As of November 24, the USDA reported that farmers had completed 97% of the expected winter wheat planting for the 2025 harvest, matching last year's rate but slightly falling short of the five-year average. Notable increases in planting occurred in California and North Carolina, with 16 out of the 18 major wheat-producing regions either finishing or nearing the end of planting.

France

In W48, French wheat prices dropped by 4.17% YoY, reaching USD 0.23/kg from USD 0.24/kg. This decline is due to a stronger euro and increased competition from the Black Sea region, where recent tenders from Tunisia and Algeria favored competitively priced Russian wheat. The depreciation of the ruble has benefited Russian exporters. Additionally, poor harvest conditions in France, including heavy rainfall that negatively impacted crop quality and yields, have contributed to the price drop. Strained diplomatic relations with Algeria, aggravated by France's recognition of Morocco's sovereignty over Western Sahara, have further reduced Algeria's wheat imports from France.

Ukraine

In W48, Ukrainian wheat prices remained stable WoW and MoM at USD 0.24/kg but rose by 20% YoY. This YoY increase is mainly due to concerns over drought conditions affecting winter wheat planting for the 2025 harvest. The ongoing war and challenging weather have reduced the area sown for winter wheat in Ukraine, with an estimated 4.2 million ha planted in 2024, down from 4.4 million ha the previous year. The smaller expected harvest and reduced carryover stocks will likely limit the country's exportable surplus, putting upward pressure on prices as global demand remains strong.

3. Actionable Recommendations

Focus on Quality to Command Premium Prices

As global wheat supply increases and competition intensifies, particularly from major producers like Russia and the Black Sea region, wheat exporters, especially in countries like Canada and France, should prioritize producing high-quality wheat to differentiate themselves in the market. This strategy involves investing in advanced crop management techniques, including soil health improvements, precision agriculture practices, and selecting wheat varieties that enhance protein content and overall grain quality. By prioritizing quality over volume, producers can target niche markets that demand premium wheat products, such as specialty milling wheat for the food industry or high-protein wheat for animal feed. These high-value markets are often less price-sensitive, enabling producers to secure better margins and increase profitability, even when overall market prices are under pressure. Moreover, focusing on quality helps meet international buyers' specific requirements, strengthen long-term trade relationships, and ensure stable demand for premium wheat.

Diversify Export Markets

With global wheat exports facing increased competition, particularly from Russia and the Black Sea region, wheat exporters must strategically diversify their export markets, especially those from countries like the EU, Canada, and Ukraine. This diversification is critical to reducing dependence on traditional markets, often subject to shifting geopolitical tensions, trade barriers, and price volatility. To capitalize on rising wheat consumption, exporters should focus on emerging markets in regions like Africa, Southeast Asia, and the Middle East, where population growth drives greater demand for staple crops. In these regions, wheat consumption is increasing rapidly, fueled by urbanization and changing dietary preferences. By tapping into these expanding markets, wheat exporters can reduce the risk of over-reliance on a few essential buyers and increase their global reach. Establishing long-term trade relationships with countries in these regions will secure steady demand and help exporters better withstand fluctuations in international wheat prices. Moreover, cultivating strong trade partnerships in diverse markets can buffer against geopolitical tensions, trade disruptions, or protectionist policies that may arise in key importing nations. By diversifying their customer base and expanding into regions with growing wheat demand, exporters can safeguard their business against market volatility and position themselves for sustained success in the global wheat trade.

Invest in Crop Resilience and Technology

To ensure stable production, Canadian wheat producers must invest in crop resilience and cutting-edge agricultural technologies. The unpredictability of climate change poses a significant challenge to wheat farming, making it crucial for producers to implement strategies that improve crop resilience and reduce vulnerabilities to adverse weather conditions. One of the most effective ways to enhance resilience is by adopting drought-resistant seed varieties better equipped to withstand periods of water scarcity and maintain yields under stress. Moreover, improving irrigation efficiency, such as using precision irrigation systems and optimizing water usage, can help mitigate the impact of droughts and ensure crops receive the necessary moisture for growth. Beyond seed varieties and irrigation, leveraging technology and data analytics can provide valuable insights into weather forecasting and yield predictions, allowing farmers to make more informed decisions about planting, fertilization, and harvest timing. By integrating advanced technologies such as satellite imaging, climate modeling, and remote sensing, wheat producers can better predict and manage environmental risks, leading to more consistent crop production.

Sources: Zol, UkrAgroConsult, Zol, Gospodarz, UkrAgroConsult, Portal Do Agronegócio