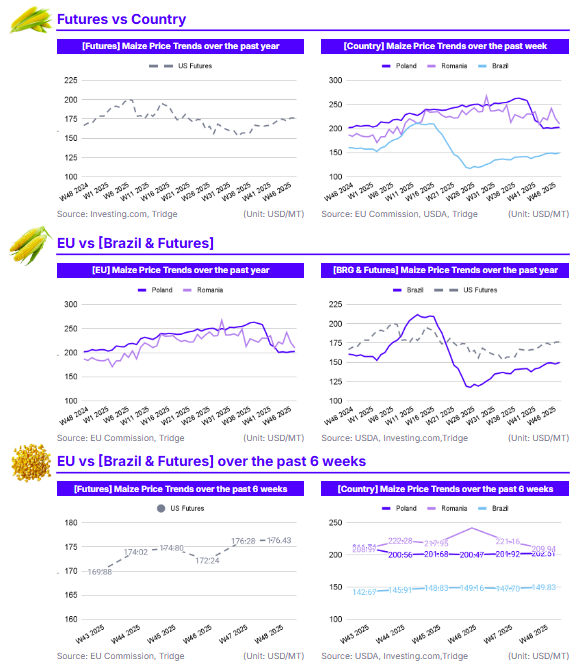

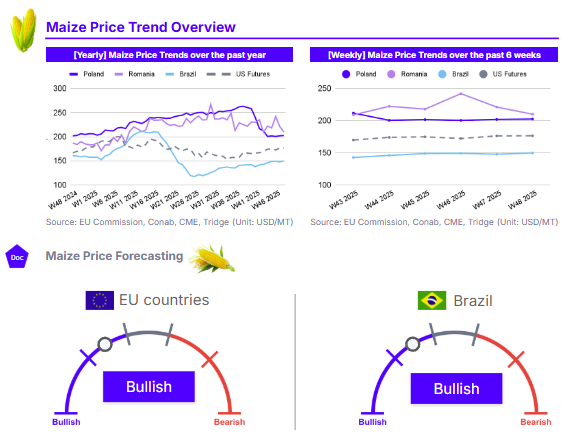

In W48 2025, maize prices showed mixed regional trends driven by supply factors and firm global demand. Romania's price corrected sharply, falling 5.08% WoW to USD 209.94/mt, following a previous spike, although the underlying structural deficit maintains a 12.25% YoY gain. Poland's price stabilized at USD 202.51/mt, confirming a low-price floor has been established by its large 10.31 mmt harvest. Both US Futures (USD 176.43/mt) and Brazil (USD 149.83/mt) saw slight WoW gains, supported by persistent export demand and market confidence following the November WASDE report, which lifted US export forecasts. Overall, global prices are firming despite record harvests, primarily due to rising global consumption exceeding production, which is resulting in lower 2025 ending stocks. European buyers are advised to capitalize on Poland's cost-effective supply while large scale buyers are advised to consider the US market on account of its record harvest and abundant available exportable volumes.

1. Weekly Price Overview

EU Supply Correction Halts Romania's Surge While Brazil, Poland and US Prices Edge Higher

In Romania, the price of maize was USD 209.94 per metric ton (mt) in W48, experiencing a 5.08% decline week-on-week (WoW). This sharp drop likely represents a market correction following the significant price spike seen in W46, even though the underlying structural problem persists, with the 2025 crop expected to be 33.28% below the five-year average due to severe weather. Poland demonstrated stability, rising marginally by 0.29% WoW to USD 202.51/mt. This stability reflects a market that has fully absorbed the supply from its large 10.31 million metric tons (mmt) 2025 harvest, keeping the price flat and competitive despite lower production across the rest of the European Union (EU).

Both Brazil and US Futures posted slight WoW gains, indicating generalized upward pressure across the Americas. Brazil's price saw a modest 1.44% WoW increase to USD 149.83/mt, while US Futures posted a minimal 0.08% WoW gain, reaching USD 176.43/mt. These gains are supported by a combination of factors. Brazil's price movement reflects continued strong export performance and domestic demand, while the US market holds firm, supported by the November WASDE report’s confirmed reduction in 2025/26 corn yield, which tempered bearish sentiment despite awaiting a record crop.

2. Price Analysis

Global Prices Trend Upward on the Back of Higher Global Consumption and Lower Ending Stocks, Despite High Production

In Romania, maize prices stand at USD 209.94/mt, maintaining a substantial 12.25% gain year-on-year (YoY) despite falling 5.55% month-on-month (MoM). The 12.25% YoY surge is the key long-term price signal, indicating persistent and severe structural supply issues compared to the previous year, with 2025 production at 33.28% below the five-year average. The recent 5.55% MoM price decline is identified as a market correction following a price spike, rather than a fundamental market shift.

Poland’s price shows remarkable stability, increasing 0.97% MoM to USD 202.51/mt, with a minimal 0.29% YoY gain. Poland’s minimal 0.29% YoY price gain despite a 23.19% larger harvest (10.31 mmt) compared to the 5 year average, confirms that the large local supply is being offset by lower production across the wider EU region. This makes Poland a consistent performer, maintaining a flat price YoY despite supply volatility elsewhere in the region.

Both US Futures and Brazilian prices posted strong MoM gains, reflecting a strengthening future demand environment. US Futures rose 1.39% MoM to USD 176.43/mt, reflecting a robust 5.94% YoY increase, while Brazil’s price increased 2.68% MoM to USD 149.83/mt, despite remaining 6.66% lower YoY. The US market's 5.94% YoY strength is rooted in the November WASDE report's projections for increased demand, specifically lifting the export forecast and raising the season-average price to USD 4.00 per bushel, which reinforces market confidence in future demand. Brazil’s 2.68% MoM rise is driven by anticipation of strong export and domestic demand, particularly from the ethanol sector, moving the price upward despite the structural downward pressure from the large 2024/25 crop. Overall, global prices are firming despite bumper harvests, primarily due to rising global consumption resulting in lower 2025 ending stocks.

3. Strategic Recommendations

Prioritize Poland for Cost-Effective EU Maize Procurement

European buyers and importers seeking to secure maize within the EU should prioritize Poland as a primary sourcing origin. This recommendation is driven by Poland's strong 2025 harvest, which contrasts with lower production across the wider EU region. Favorable weather has resulted in a large Polish harvest, estimated at 10.31 mmt, which is 23.19% above the five-year average. The market correction seen in prior weeks has largely concluded, with the price stabilizing at around USD 200/mt since W44, confirming a price floor has been established. This makes Poland a highly cost-effective origin within the EU, especially when compared to its regional competitor, Romania, where drought-reduced supplies have driven prices up 12.25% YoY. Poland has solidified its position as a major producer and exporter in the EU, and its price competitiveness and ample harvest present a clear procurement opportunity.

Prioritize the US for Large-Volume Supply Based in the Americas

Global importers needing to secure large-volume contracts should focus on the US as the primary procurement destination. The fundamental driver for this strategy is the large 2025/26 crop, though the November WASDE report tightened the outlook. The official forecast revised US corn production downward, though it remains large at 426.72 mmt (16.8 billion bushels) and raised exports to a record 78.74 mmt (3.1 billion bushels). This immense supply, coupled with record export demand, has pushed the season-average farm price forecast higher. The US market offers exceptional liquidity with the harvest nearly complete, ensuring readily available physical supply. This large supply volume has anchored US prices, making it a reliable and stable source for large-volume procurement. The US market’s inherent stability and supply assurance are evident in the current futures price of USD 176.43/mt, which remains highly competitive on the global stage.