.jpg)

1. Weekly News

European Union

EU Shifts to Soybean Products Despite Declining Soybean Oil Imports and Trade Uncertainty

European Union (EU) soybean oil imports have declined sharply, falling 66% year-on-year (YoY) as of November 24, 2024, reflecting a shift in trade preferences. This decline is offset by higher soybean and soybean meal imports, with the EU relying on domestic crushing to meet soybean oil demand. Total oilseed imports rose by 8% YoY, while meal imports grew by 14% YoY, driven by a 25% increase in soybean meal imports.

Rising sunflower oil prices and additional duties on Russian and Belarusian oilseeds reduced rapeseed and sunflower oil imports, prompting a shift to soybean-based products. Market uncertainty surrounding the European Union Deforestation Regulation (EUDR), set to take effect Dec-25, further influenced import behavior as stakeholders increased soybean and meal purchases to preempt regulatory challenges.

India

India's Soybean Oil Imports Rise 20% MoM in Nov-24 Due to Post-Festival Demand Surge

India's vegetable oil imports surged to a four-month high in Nov-24, driven by strong post-festival demand. Soybean oil imports rose 20% month-on-month (MoM) to 410,000 metric tons (mt), while sunflower oil imports increased 43% MoM to 341,000 mt. Palm oil imports also rose by 0.5% MoM to 850,000 mt. Total vegetable oil imports reached 1.6 million metric tons (mmt), up 12% from Oct-24. India, the world's largest vegetable oil importer, sources palm oil from Indonesia, Malaysia, and Thailand, as well as soybean and sunflower oils from Argentina, Brazil, Russia, and Ukraine.

Russia

Russia's Soybean Oil Growth Driven by Expanding Processing Capacity and Record Production

Russia's soybean oil production is poised for growth, supported by expanding oilseed processing capacity, which may increase by an additional 6 mmt, according to the Institute for Agricultural Market Studies (IKAR). This expansion will require from 4 to 6 mmt more raw materials and an additional 2 to 3 million hectares (ha) of oilseed crops, driven by their higher profit margins compared to grain alternatives. However, high interest rates could temper investor activity.

Despite challenging weather conditions, soybean production in Russia reached a record 6.9 mmt in 2024, marginally higher than the previous year. This aligns with the increased availability of soybean meals in the domestic market, with global prices declining—a positive trend for livestock farmers. The quality of soybeans, particularly protein levels, is influencing price segmentation. Furthermore, export restrictions on oilseeds and processed products to the EU since Jun-24 have minimally impacted soybean oil and meal but disrupted sunflower and rapeseed meal trade.

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W49 2023 to W49 2024)

.png)

Brazil

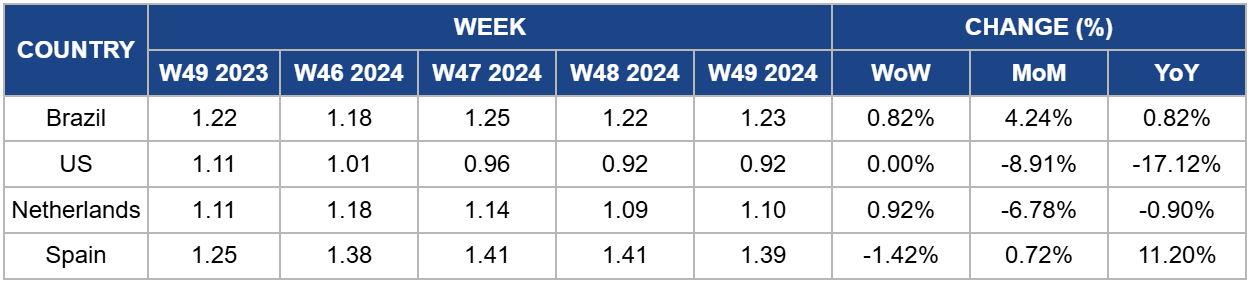

Brazil's soybean oil prices increased in W49, rising to USD 1.23 per kilogram (kg), marking a 0.82% increase week-on-week (WoW) and YoY. This slight rise may be influenced by ongoing discussions within the Brazilian Association of Vegetable Oil Industries (Abiove) regarding a potential reform of the soy moratorium. The proposed reform would alter the monitoring process to focus on individual fields rather than entire farms, which could affect soybean production practices and supply dynamics. If implemented, this reform could have a significant impact on future soybean oil prices. It could stabilize supply and mitigate price volatility if it leads to increased production efficiency or broader compliance with environmental regulations. However, resistance from regions like Mato Grosso, which has opposed adherence to the moratorium, could introduce uncertainties, mainly if it results in legal or tax-related disruptions. The evolving regulatory landscape will likely be a key factor influencing Brazil's soybean oil market and pricing trends in the coming months.

United States

In W49, the United States (US) soybean oil prices remained stable at USD 0.92/kg but decreased 8.91% MoM. The price drop is driven by the rising demand for imported used cooking oil (UCO) as a biofuel ingredient.. With a lower carbon intensity than soybean oil, UCO has gained popularity due to federal and state incentives to reduce biofuels' carbon footprint. UCO imports into the US nearly doubled from Jan-24 to Sep-24 compared to the same period in 2023, reflecting the increasing reliance on this alternative feedstock. Despite the rise of UCO, soybean oil remains a vital biofuel feedstock. Any disruptions to the UCO supply, such as potential tariffs on imports from China—responsible for over half of US UCO imports—could lead to a shift back to domestic soybean oil. Recently, China has reduced export tax rebates on UCO, which may limit supply and drive higher demand for soybean oil. If UCO imports face further restrictions or higher tariffs, biofuel producers could increasingly turn to soybean oil, potentially exerting upward pressure on prices. The soybean oil market is still volatile due to changing trade policies and shifting feedstock preferences, making future prices uncertain.

Netherlands

In W49, soybean oil prices in the Netherlands rose to USD 1.10/kg, reflecting a 0.92% WoW increase. However, future price trends remain uncertain as the Netherlands, a major importer and re-exporter of soybean oil, faces mounting regulatory challenges from the EUDR. This regulation aims to limit trade in products linked to deforestation, potentially disrupting the soybean oil supply chain. Soybean imports have decreased by 21% since 2002, and further reductions could tighten supply, putting upward pressure on prices. Although prices have softened recently, the upcoming EUDR could have significant implications for the market, potentially raising costs in the medium term depending on how import volumes and compliance costs evolve. Regulatory changes and tightening supply may lead to higher soybean oil prices shortly, especially if trade disruptions intensify.

Spain

Spain's soybean oil prices decreased to USD 1.39/kg in W49, reflecting a slight 1.42% WoW decline, though prices rose 0.72% MoM. Despite domestic interest in non-genetically modified (GM) soybeans, Spain faces significant challenges in expanding domestic soybean cultivation, particularly in regions like Castilla y León. Factors such as low yields, agronomic difficulties, and stiff competition from larger global producers have hindered the economic viability of domestic soybean farming. As a result, Spain remains highly dependent on soybean oil imports, a reliance that could impact future price trends. With global market conditions, including supply chain disruptions and regulatory pressures, influencing trade dynamics, Spain's dependency on imported soybean oil may subject local prices to fluctuations in the international market. These factors suggest that while current prices have softened, Spain could face price volatility in the medium to long term, driven by global soybean production and trade changes.

3. Actionable Recommendations

Diversify Sourcing Strategies for Soybean Oil

Given the sharp decline in EU soybean oil imports and the increased reliance on domestic crushing, stakeholders should consider diversifying their sourcing strategies. Companies can mitigate the impact of price volatility and supply chain disruptions by exploring suppliers from emerging markets like Russia, where soybean oil production is set to grow, and Brazil, which is undergoing regulatory changes affecting soybean production. Additionally, sourcing from alternative regions, such as Argentina and India, where soybean oil demand is rising, can help ensure a stable supply of soybean oil in the face of regulatory challenges like the EUDR.

Monitor Regulatory Developments and Adapt to the EUDR

With the upcoming EUDR to affect the soybean oil trade starting Dec-25, stakeholders should stay informed about regulatory changes and adapt sourcing strategies accordingly. The EUDR could tighten the soybean oil supply in the EU, leading to higher prices. Companies importing soybean oil into the EU should explore alternative sourcing options, adjust procurement timelines, and engage in early compliance initiatives to mitigate potential disruptions. Additionally, establishing partnerships with proactive suppliers to meet these regulations will ensure a more reliable supply chain.

Invest in Supply Chain Resilience Through Long-Term Contracts

To counteract price fluctuations and market uncertainty in soybean oil, businesses should secure long-term contracts with multiple suppliers across different regions. By committing to agreements with suppliers in Brazil, the US, and Russia, companies can hedge against price volatility and ensure a consistent supply of soybean oil. This strategy also allows businesses to manage price risks more effectively, especially in markets where production costs and regulatory changes can significantly impact pricing. Additionally, fostering strong relationships with suppliers can promote sustainability and improve supply chain stability.

Sources: Agro Investor, Agroconf, Noticias Agricolas