1. Weekly News

Global

Global Sugar Production Rises as Stocks Decline Amid Shifting Market Dynamics

The United States Department of Agriculture (USDA) projects global sugar production to grow by 2.8 million tons, reaching 186.6 million tons. This growth is due to higher outputs in China, India, and Thailand despite a decline in Brazil. Thailand's strong performance has boosted global sugar exports, while India's record-breaking consumption highlights rising demand. However, global sugar stocks are expected to decline due to reduced reserves in Thailand, offsetting increases in India. These trends highlight a shifting balance in the global sugar market, shaped by varying production and consumption patterns.

India

India's Sugar Production Rises Amid Expected Export Declines

India's sugar production for the 2024/25 marketing year (MY) is projected to increase by 1.5 million tons, reaching 35.5 million tons, driven by favorable weather and higher yields. Rising incomes are expected to boost domestic sugar consumption, while imports are set to decrease due to higher production. However, exports are anticipated to decline slightly as government policies may prioritize meeting domestic demand through export restrictions.

Mozambique

Mozambique's Sugar Industry Recovers with Growth in Production and Exports

Mozambique's sugar production is expected to rise by 10% to 1.9 million tons in the 2024/25 agricultural campaign, up from 1.6 million tons the previous year. This growth follows challenges caused by floods that disrupted family and industrial production and led to the temporary closure of the Maragra sugar mill. Improved production has strengthened sugar exports, which generated USD 10.8 million in the same period last year, signaling recovery from the adverse climatic impacts of 2023.

Russia

Russia's Sugar Production Rises with Resumed Exports to Eurasia and Africa

Sugar production in Russia from Nov-23 to Oct-24 reached 6.97 million tons, marking an increase of 320 thousand tons from the previous period. Sugar reserves at factories grew by 239 thousand tons to 1.97 million tons compared to last year. Processing of sugar beets has concluded in the South but continues in regions such as the Central Black Earth, Volga-Urals, and Altai until Feb-25. Russia resumed sugar exports to markets in Eurasia and Africa in Sep-24. At the same time, neighboring countries like Belarus, Kazakhstan, Kyrgyzstan, and Azerbaijan are also forecast to boost beet sugar production in the 2024/25 season.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W49 2023 to W49 2024)

.png)

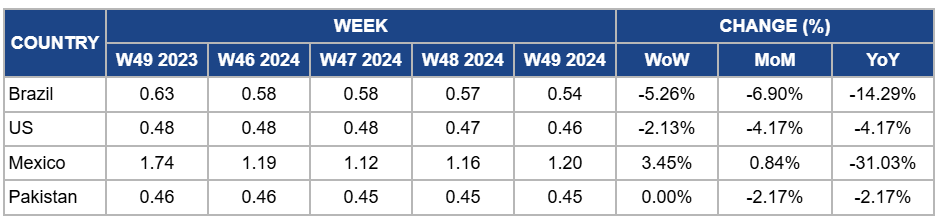

Brazil

Brazil's sugar prices dropped by 5.26% week-on-week (WoW) to USD 0.54 per kilogram (kg), reflecting a 6.90% month-on-month (MoM) decline and a 14.29% year-on-year (YoY) drop. The price dip is due to a challenging production season in Brazil's center-south region, where reduced sugarcane supply, worsened by drought conditions and a shift towards ethanol production, led to a 60% decline in sugar production in early November. Additionally, the 52.8% decrease in sugarcane crushing during this period further weakened sugar prices. Despite the lower sugar prices, the rising demand for ethanol and higher ethanol prices have offset some of the pressure in the domestic market. However, the sector's ongoing challenges have continued to impact domestic and international sugar prices.

United States

In the US, sugar prices dropped by 2.13% WoW to USD 0.46/kg in W49, with a 4.17% MoM drop and a 4.17% YoY decline. The price decline is due to continued concerns over reduced sugar production for the 2024/25 season, with lower yields and earlier harvests pulling some production into the 2023/24 season. The tightening supply situation and a 32% projected drop in sugar stocks have strained the market. Despite record-high production in 2023/24, reduced sugar imports and increased domestic consumption contribute to the shortfall. The USDA's forecasts and tight supply conditions have kept downward pressure on prices, though future adjustments in import policies or forecasts could stabilize or drive prices up.

Mexico

Sugar prices in Mexico increased by 3.45% WoW to USD 1.20/kg in W49, with a 0.84% MoM increase. The price increase is due to heightened demand for sugarcane during the year-end season, particularly in regions like Querétaro, where it is a key ingredient in holiday drinks and snacks. As the harvest season peaks, sugarcane demand could continue supporting local sugar prices. However, prices have dropped significantly by 31.03% YoY due to a larger base price from last year, when prices were higher, and a normalization of sugar production and supply in the country.

Pakistan

Pakistan's sugar prices remained stable at USD 0.45/kg in W49, with a 2.17% MoM and YoY increase. This is due to the ongoing challenges in the sugarcane industry, particularly the growing preference among farmers for manufacturing gurr (jaggery) instead of selling their crops to sugar mills. The attractive market rates for gurr, which offer immediate profits compared to the lower prices paid by sugar mills, have reduced the sugarcane milling supply. Despite the government's announcement to begin the cane-crushing season, many mills have not complied, prompting farmers to establish mobile jaggery production units. This trend has helped stabilize sugar prices, although concerns over rising input costs and the potential long-term impact on sugar supply remain.

3. Actionable Recommendations

Optimize Supply and Diversify Markets to Strengthen Demand

Sugar producers and exporters in India should focus on optimizing supply chains to ensure efficient distribution and cater to increased domestic consumption. Exporters should proactively seek diversification of international markets to offset the potential impact of export restrictions and maintain revenue streams. Collaboration with domestic buyers to align with rising consumption trends can help balance supply and demand while enhancing profitability.

Capitalize on Market Recovery Through Strategic Hedging

Sugar traders and producers should leverage the recent rebound in sugar futures by employing strategic hedging techniques to manage price risks. Traders can use futures contracts to lock in favorable prices, while producers should monitor supply trends and adjust export volumes to align with evolving market conditions. Collaboration with industry associations like UNICA can provide valuable market insights, helping mitigate potential supply challenges in early 2025.

Strengthen Export Strategies Amid Rising Competition

Russian sugar exporters should diversify their market base by targeting high-demand regions in Eurasia and Africa, focusing on competitive pricing and quality differentiation. Competitive pricing can be achieved by analyzing regional demand and adjusting prices accordingly, ensuring affordability without sacrificing margins. Quality differentiation can be realized by emphasizing superior sugar grades, organic or specialty options, and consistent quality control. Collaboration with domestic sugar factories to optimize supply chains and adjust export volumes can help maintain a steady flow of sugar exports. Additionally, exporters should closely monitor neighboring countries' increasing production to anticipate market dynamics and refine their strategies accordingly.

Sources: Tridge, Diarioeconomico, Freshplaza, NoticiasAgricolas, Portal Do Agronegócio, UkrAgroConsult, USDA, Zol