Effects of El Niño on Mexican Agriculture

In Mexico, over 55% of the country faced extreme drought from Jan-23 to Aug-23, impacting states like Sonora, Chihuahua, and Sinaloa. The Bank of Mexico warned of potential agricultural losses of up to 0.16% of GDP in 2023, with a 25% crop loss risk if drought persists. As of Nov-23, 21% of the country faces extreme to exceptional drought, and a 95% likelihood exists for El Niño persisting from Dec-23 to Feb-24, intensifying drought in Central and Southern Mexico while bringing heavy rains to the Northern regions.

.jpg)

Understanding El Niño and Its Impacts on Latin America

El Niño, part of the El Niño-Southern Oscillation (ENSO), involves the abnormal warming of the eastern tropical Pacific Ocean, impacting ocean temperatures, currents, coastal fisheries, and global weather patterns. El Niño events occur irregularly every two to seven years, with episodes lasting between nine and 12 months, typically between June and August, leading to widespread climatic changes and disrupting the agriculture industry.

The National Oceanic and Atmospheric Administration (NOAA) officially declared the emergence of El Niño in Jun-23, and it has since gradually strengthened into the Northern Hemisphere winter.

The impact of El Niño varies significantly based on geographical location, leading to diverse climate effects across the globe and within Latin America (LATAM).

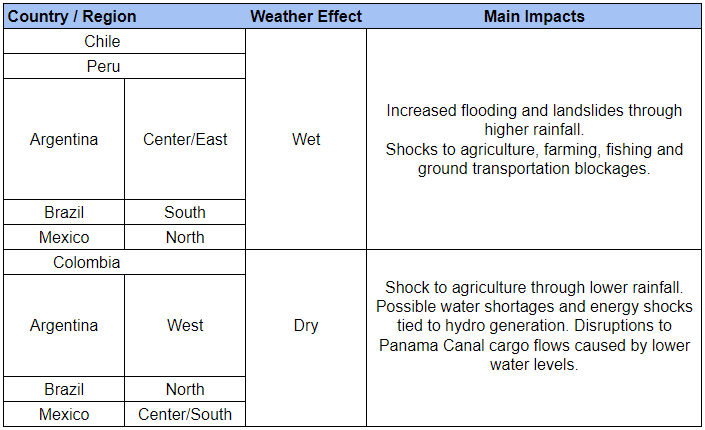

Impact of El Niño in Latin America

Based on data collected by NOAA from 1965 to 2023, El Niño 2023 has the warmest global temperatures on record so far, with above-average sea surface temperatures (SST) across the equatorial Pacific Ocean. El Niño has increased temperatures across LATAM, especially in the Eastern Pacific region. Central America, the Caribbean, and northern South America have also been affected. The situation in LATAM and the Caribbean is alarming, with direct economic losses estimated at USD 28 billion over the last 20 years, constituting 15% of global losses. So far, the effect of El Niño has varied in different LATAM countries.

El Niño’s Impact on Mexico

In Sep-23, the National System of Climate Change (SINACC) noted that over 55% of Mexico's territory endured extreme drought during the first eight months of 2023, impacting producing states like Sonora, Chihuahua, Sinaloa, and others, reaching unprecedented levels in the last five years.

The Bank of Mexico estimates potential agricultural losses of up to 0.16% of the Gross Domestic Product (GDP) in 2023, warning of a 25% crop loss if drought patterns persist. While northern regions grappled with drought, the south faced challenges from hydrometeorological events and tropical cyclones affecting 60% of the national territory. Hurricane Agatha in May-22 prompted AXA México's parametric insurance program, compensating over 700 small corn producers. With predictions of an intense hurricane season due to the El Niño phenomenon and rising sea temperatures, innovative solutions are crucial to combat climate change's effects on the agri-food industry.

According to the National Meteorological Service's (SMN) Drought Monitor, as of Nov-23, 21% of the country's municipalities (538 total) are experiencing extreme to exceptional drought, with an additional 41% (1.02 thousand municipalities) facing moderate to severe drought.

According to Mexico's SMN, there is a 95% likelihood that a strong El Niño event will persist in the Northern Hemisphere from Dec-23 to Feb-24. This phenomenon has led to drought in Central America and central/southern Mexico, while the northern regions may experience heavy rains, exemplified by flooding in the United States (US).

Maize Challenges and Outlook in Mexico

The expected production of white maize is estimated at 22.90 million metric tons (mmt) as of Oct-23, a 1.2% decrease compared to 2022. In addition, yellow maize is expected to reach only 2.94 mmt, marking a 12.4% YoY decrease. In Mexico, where rainfed areas and marginal production systems are common, maize yields are vulnerable to interannual variations in precipitation influenced by El Niño.

The National Chamber of Industrialized Maize (CANAMI) anticipates that lower maize production due to drought in key states like Sinaloa and Sonora will have severe consequences, especially for companies in animal feed production.

A scarcity of yellow maize domestically has led to the importation of 12 mmt in 2022, constituting 67% of the industry's needs. The ongoing drought, affecting 78% of the country, is expected to reduce 2023 spring/summer production by 1 mmt. Production in fall/winter may face more severe challenges as major producers like Sinaloa and Sonora have low water reserves, with dams at only 28% capacity. With Mexico importing 40% of its yellow maize needs (18 mmt on average), the consequences of the drought may increase imports to 23 mmt in 2024.

The agricultural sector in Sinaloa faces significant challenges in deciding which crops to plant for the autumn-winter 2023/24 cycle. The region is grappling with extreme drought, impacting water availability and the spring-summer crop cycle. With only 33 percent water availability compared to the previous year, a substantial reduction in maize and sorghum planting area by around 50% is anticipated. Despite lower international prices, the drought's effects on the current and upcoming cycles are forecasted to counterbalance the decline. Producer organizations are collaborating with the State Government to optimize water use and implement effective marketing strategies in response to the market conditions for corn and beans.

Sorghum Production Overview Amid Unprecedented Drought Conditions

The impact of drought on crucial crops is severe, with devastating consequences for sorghum. States like Chihuahua report a 96% loss in sorghum harvest in the municipality of Parral. The President of the National Agricultural Council emphasizes the extensive impact, noting that sorghum cannot be planted in the north of Mexico due to water scarcity.

From Oct-22 to Sep-23, the Mexican production of sorghum amounted to 4.4 million tons with a surface of 1.47 million hectares (ha), a 69.88% decrease compared to the 2021/22 autumn-winter cycle obtaining a volume of 2.59 million tons with a surface of 830.99 ha.

Furthermore, despite initial challenges with a lack of rain in Tamaulipas, Mexico, farmers in the Altamira region anticipate a successful sorghum harvest. The social sector farmers, facing unaffordability for maize, shifted to sorghum. Over 25 thousand ha were yielded with sorghum due to unfavorable conditions for soybean and maize cultivation. Sorghum produced good results, with yields exceeding 3 metric tons per ha.

Sorghum prices, ranging between USD 287.43 and 344.92/ton (MXN 5,000 to 6,000/ton), prove advantageous for farmers, contributing to a positive economic impact on the Altamira countryside.

Impacts of El Niño on Mexican Sugarcane, Harvest Challenges, and Production Trends

In Mexico, the El Niño weather phenomenon, characterized by increased winter rainfall and arid summer conditions, posed challenges for sugarcane development. The sugarcane crop heavily relies on mid-year rainfall for growth and maturation, and summer drought adversely impacted yields, especially as over 60% of Mexican sugarcane is not irrigated. The occurrence of El Niño varies, and while the significant El Niño of 2014/16 did not lead to a reduction in sugar production, the minor El Niño in 2018/19 resulted in widespread drought and decreased sugar output.

However, as of Oct-23, the expected production of sugar cane is estimated at 51.12 mmt, marking an 8% year-on-year (YoY) decrease compared to 2022, with 55.55 mmt.

During Oct-23, the price fluctuations in cane sugar were attributed to the seasonal nature of its harvest, which does not occur from August to October. Consequently, inventories have witnessed a notable decline of 15.9% compared to the previous month. This trend aligns with the typical seasonal patterns of sugar production and availability.

As reported by the National Committee for the Sustainable Development of Sugarcane (CONADESUCA), the 2022/23 sugar cane harvest revealed an industrialized area of 806 thousand ha, cane production of 47.5 million tons, and sugar production of 5.2 million tons. This positions the sugar industry as highly competitive, contributing 6.21% to the agricultural gross domestic product (GDP). The industry has proven resilient despite political and agro-climatic challenges such as El Niño. The recently enacted Law for the Sustainable Development of Sugar Cane ensures national supply and leverages opportunities in the North American market through the United States–Mexico–Canada Agreement (T-MEC) agreement.

Challenges in the Mexican Avocado Industry

The avocado industry faces challenges such as the impact of climate change, including the El Niño phenomenon and rising freight rates affecting transportation, with significantly lower volumes impacting European exports. The usual peak supply period from September to December is experiencing a dramatic shipment decline.

Climatic issues attributed to El Niño have led to the predominance of medium and small-sized avocados, making it challenging to compete with other growing countries for exports to the European market. The focus has shifted to national markets, Japan, Canada, and other destinations where costs can be recovered. Higher shipping costs exacerbated the unprofitable situation, leading Mexican exporters to concentrate on markets with more potential profitability.

Avocado production in Michoacán, Mexico, reached 1.56 million tons as of Oct-23, representing an almost 2% increase compared to the same period in 2022. The production increase is attributed to increasing avocado plantations, offsetting the large losses from the drought. Michoacán remains the leading avocado-producing state, contributing 72% to the national harvest. Jalisco follows with 260.11 thousand tons, and the State of Mexico, Nayarit, and Morelos round out the top five. Tancítaro leads in municipal production with 202.64 thousand tons, followed by Salvador Escalante, Ario, Uruapan, and Tacámbaro.

Despite concerns regarding environmental impacts linked to El Niño and labor-related issues, Michoacán is poised for another historic year in avocado production.

As a reference, prices dipped to USD 2.83 per kilogram (kg) at the Tijuana border due to a supply surplus during Nov-23. Despite challenges, prices are expected to rise gradually in Dec-23, fueled by increased demand from the US during the holiday season and reduced supply from local and international sources.

El Niño's Impact and Harvest Dynamics on the Mexican Tomato Industry

Sonora, a key tomato-producing state in Mexico, grappled with challenges posed by the peso-dollar exchange rate and drought due to El Niño. Data from the Agri-Food and Fisheries Information System (SIAP) of the Ministry of Agriculture indicates that Sinaloa, Michoacán, Guanajuato, and Sonora are the primary contributors to tomato production in Mexico. While the industry employs approximately 500 thousand people nationwide, recent years have seen setbacks such as droughts and pest issues affecting tomato cultivation.

Gourmet varieties like Cherry and Grape were successfully harvested in late 2022 and Jan-23, with the main harvest of Bola and Saladette varieties commencing in Jul-23. Despite a slight harvest delay due to El Niño-induced weather conditions, the overall crop development remained positive.

As of the 2023/24 season, tomato-producing states Michoacán, Zacatecas, and Jalisco reduced the export volumes of high-quality products due to cold weather attributed to El Niño that impacted harvest forecasts. During W44, the market showed initial signs of a price increase trend, which is expected to continue until significant volumes from Sinaloa impact prices in late Jan-24. For reference, at the end of W44, Free on Board (FOB) McAllen market prices for Roma tomatoes were USD 17 for 19/25 pounds (lbs) jumbo size, USD 14 for 16/25 lbs x-large, USD 12 for 13/25 lbs large, and USD 10 for 11/25 lbs medium size. With the year-end approaching and cold weather setting in, market prices for Roma tomatoes are forecasted to continue rising. However, the declining volume due to lower temperatures in the region may accelerate and intensify price increases by the end of 2023.

El Niño Outlook, Growing Strength, and Persistence Forecasted for the Rest of 2023 and Early 2024

As of late Nov-23, observations point to a strengthening El Niño, with above-average sea surface temperatures across the equatorial Pacific. The latest forecast by NOAA suggests a high likelihood of El Niño persisting from Jan-24 to -Mar-24. The plume forecast (a strong indicator of severe weather, including tornadoes, large hail, or powerful winds) has a 62% chance of El Niño's continuation from Apr-24 to -Jun-24 in the Northern Hemisphere spring.

Furthermore, forecasts for Q1-2024 predict above-average rainfall in the southern cone countries such as Peru, Ecuador, and Mexico, while dry conditions are anticipated to continue in Brazil, Guyana, and Suriname. The current dry weather in Central America is forecasted to last until the end of 2023.