Global Food Prices Hit 18-Month High Amid Supply Challenges and Demand Surges

Global food prices reached their highest level since Apr-23, with the Food and Agriculture Organization (FAO) Food Price Index averaging 127.4 points in Oct-24, a 2% increase from its revised Sep-24 level, according to FAO. The rise was driven by higher prices across nearly all major commodities, except meat. This upward momentum reflects a confluence of supply constraints, demand surges, and geopolitical factors, creating significant ripple effects across global markets.

Key Commodity Trends

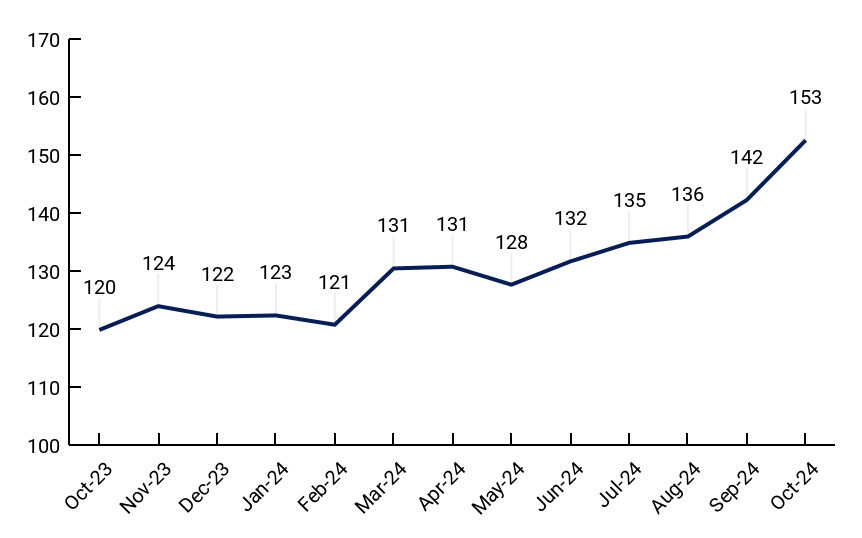

Vegetable Oils

The FAO Vegetable Oil Price Index climbed significantly in Oct-24, averaging 152.7 points, a substantial 7.3% increase compared to Sep-24. This marked the highest level in two years. The price surge was fueled by higher quotations across key oils, including palm, soya, sunflower, and canola, which saw robust demand amidst tighter supplies. Adverse weather conditions in major producing regions and logistical challenges exacerbated supply pressures, further elevating prices. The rising demand for vegetable oils in both food and biofuel production also contributed to this upward trend, with global markets facing persistent supply uncertainties.

Figure 1. FAO Vegetable Oils Index

Cereals

The FAO Cereal Price Index experienced a modest rise of 0.8%, averaging 114.4 points in Oct-24. Global wheat prices led the increase, marking the second consecutive month of gains. Concerns over unfavorable weather conditions during winter crop sowing in several major exporting regions, including the European Union (EU), Russia, and the United States (US), played a significant role in driving prices higher. Additionally, Russia’s reinstatement of an unofficial price floor for wheat and escalating geopolitical tensions in the Black Sea region added further upward pressure. These developments have heightened uncertainty in global grain markets, with many stakeholders closely monitoring weather patterns and political developments.

Dairy

Dairy prices continued their upward trajectory, with the FAO Dairy Price Index rising by 1.9% to 139.1 points in Oct-24. International cheese prices saw the most significant increase due to limited availability for spot imports, primarily driven by strong domestic demand in the EU, where seasonal declines in milk production further constrained supply. Similarly, global butter prices climbed for the 13th consecutive month, bolstered by low stock levels and reduced milk output in Western Europe. However, milk powder prices, especially skim milk, fell during this period. Increased seasonal milk production in Oceania and weaker global import demand were key factors in this decline, highlighting regional disparities in the dairy market.

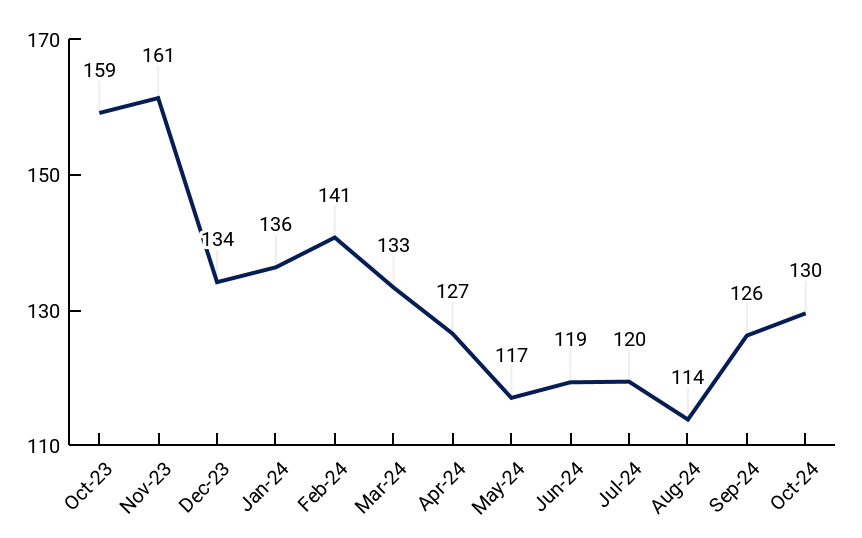

Sugar

The FAO Sugar Price Index recorded its second consecutive monthly increase, rising by 2.6% to an average of 129.6 points in Oct-24. This was largely attributed to concerns over the production outlook in Brazil, the world’s largest sugar producer, following extended periods of dry weather that threatened the 2024/25 harvest. Additionally, higher international crude oil prices stimulated the diversion of sugarcane toward ethanol production, further tightening global sugar supplies. However, improved rainfall in late Oct-24 and the weakening of the Brazilian real against the US dollar moderated the overall price increase. Despite these mitigating factors, the sugar market remains volatile, with weather, energy, and currency dynamics shaping price movements.

Figure 1. FAO Sugar Index

Meat

In contrast to other commodities, meat prices saw a slight decline in Oct-24, with the FAO Meat Price Index averaging 120.4 points, a 0.3% decrease from the previous month. The decline was driven primarily by sharp drops in pig meat prices, as increased slaughter rates in Western Europe and weaker global demand weighed heavily on the market. Poultry prices also dipped, reflecting higher export volumes that offset domestic consumption pressures. However, beef prices remained stable, with strong demand balancing increased supplies from Oceania’s new production season. The meat sector’s mixed performance highlights the varied supply and demand dynamics across different regions and product categories.

Outlook

The surge in global food prices highlights ongoing vulnerabilities in international agricultural markets. Vegetable oil prices are expected to remain high in Nov-24 due to persistent supply chain disruptions and strong biofuel demand. Similarly, sugar prices could stay elevated as weather-related uncertainties in Brazil and energy market linkages continue to impact global supplies.

Cereal markets face significant risks tied to weather conditions and geopolitical developments, particularly in the Black Sea region. In particular, wheat prices could see further volatility if adverse weather persists or geopolitical tensions escalate. Meanwhile, the dairy sector will likely experience continued upward pressure on cheese and butter prices, driven by strong demand and supply constraints in key regions like the EU.

Meat prices may see a further decline in certain categories, such as pig and poultry, as ample supply and weak demand continue to weigh on markets. However, beef prices are expected to remain steady, supported by robust global demand.

As global markets navigate these challenges, stakeholders across the agricultural supply chain must remain vigilant, adapting strategies to mitigate risks associated with climate variability, geopolitical uncertainties, and fluctuating consumer demand.