Impact of 2025 US Import Tariffs on Trade Routes and Freight Prices: Shifting US-China Trade Dynamics

Agricultural sectors such as soybeans, corn, beef, and tea have been heavily impacted, with China pivoting to Brazil, Argentina, and Australia to replace US imports. The end of de minimis exemptions for small parcels from China further strained trade. A 90-day tariff rollback between the US and China starting May 14 offers temporary relief, but global sourcing and shipping patterns remain in flux.

[Editor’s Note]

Despite a 90-day tariff pause starting May 14, April’s US–China tariff clash has already hit global freight. US–China West Coast rates plunged 44.55% in three months, while Asia–Europe routes held steady amid fears of overflow. Southeast Asia–US volumes rose 20% due to frontloading, straining logistics—especially for perishables. Recovery is possible, but long-term stability hinges on resolving trade tensions and easing infrastructure bottlenecks.

Initially introduced in Feb-25 and progressively adjusted, the United States (US) import tariff hike has significantly disrupted supply chains across various sectors, including agriculture and freight prices and volumes. The most impactful update came on April 2, when the US imposed a baseline 10% tariff on all imports, with higher rates for goods from countries with which the US has trade deficits, like China, the European Union (EU), Vietnam, South Korea, Japan, and others. Although these elevated tariffs were later suspended for 90 days, China was subjected to an even higher tariff of 145%. In response, China retaliated with a 125% tariff on imports from the US. However, the two countries have agreed to roll back their reciprocal tariffs by 115%, starting May 14. Despite this agreement, the tariffs implemented in Apr-25 have had a severe impact on the trade flows of key agricultural commodities such as soybeans, corn, beef, tea, and more. The resulting shifts in trade patterns have also disrupted traditional shipping routes, contributing to significant fluctuations in global freight prices and container volumes.

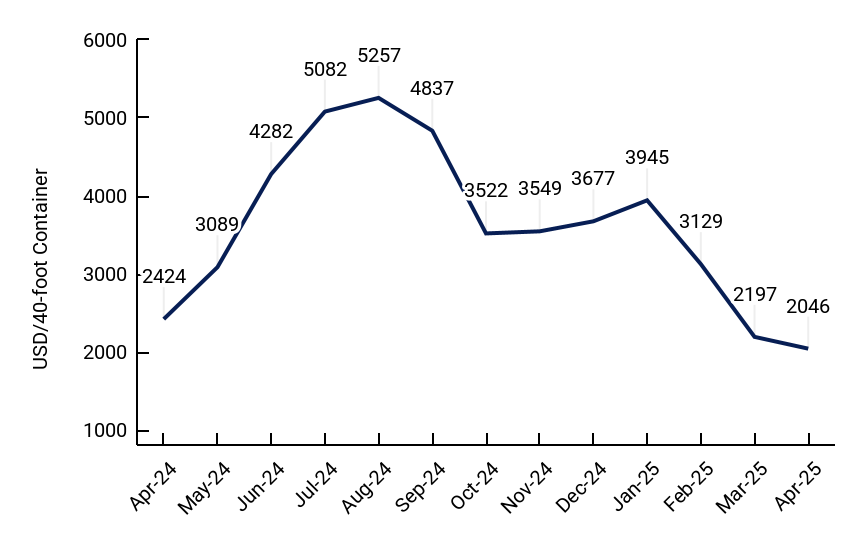

According to the Freightos Baltic Index (FBX), global freight prices averaged USD 2,045.93 per 40-foot container in Apr-25, marking a 6.87% month-on-month (MoM) drop and a 15.61% year-on-year (YoY) decline. The drop is primarily linked to the US–China trade tensions resulting from the ongoing tariff war. Other than the implementation of US tariff increases, the downward trend observed since Feb-25 has also been driven by a seasonal slowdown in demand following the Lunar New Year (LNY), and the conclusion of pre-LNY frontloading activities.

Figure 1. Freightos Baltic Index Trend

US 2025 Tariffs Trigger Trade Route Realignments and Freight Volatility

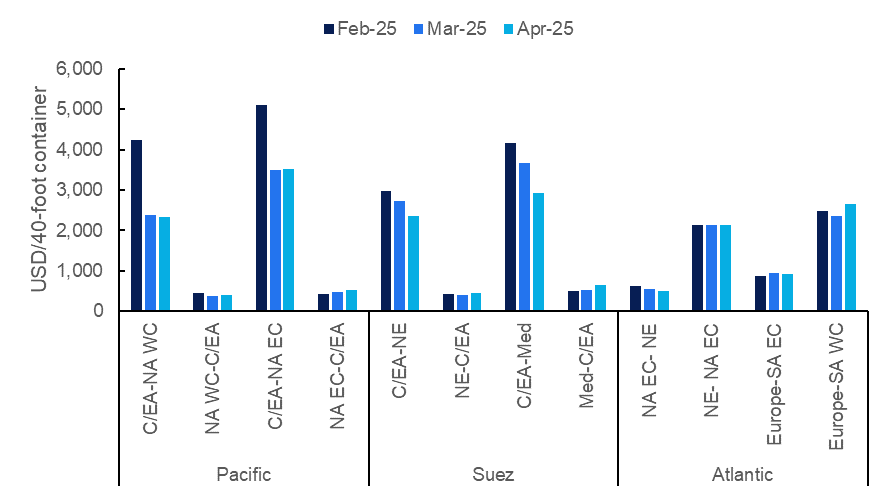

The uncertainties triggered by the US tariff hikes have led to freight price fluctuations across major global trading routes. According to Freightos data, in the last week of Apr-25, Asia-US West Coast (WC) ocean rates fell by 0.64% week-on-week (WoW) to USD 2,328/40-foot container from USD 2,343, while rates on the Asia–US East Coast (EC) route fell by 2.08% WoW to USD 3,395 from USD 3,467. Over the past three months, China/East Asia (C/EA)-North America (NA) WC prices fell from USD 4,229.2/40-foot container in Feb-25 to USD 2,345.25/40-foot container in Apr-25, a significant 44.55% drop.

Figure 2. Freight Price Trends Across Major Global Shipping Routes

These price drops are largely attributed to US importers canceling orders in response to the steep tariffs imposed by the US government. Many US-bound vessels from China have been departing half-empty, as shippers canceled shipments that had more than doubled in cost due to the tariff increases. As a result, China–US ocean freight demand has reportedly plummeted by 30% to 50% in Apr-25. Having stockpiled inventory ahead of the tariff hikes, many importers are now adopting a wait-and-see approach, as reflected in the surge in demand for bonded US warehouse space.

In contrast, Asia–Europe shipping routes have seen fewer blank sailings despite elevated capacity levels, suggesting a growing demand, possibly driven by diverted US orders. According to Freightos, rates on the Asia–North Europe (NE) route remained relatively stable at USD 2,337/40-foot container in the last week of Apr-25, while rates on the Asia–Mediterranean (Med) route rose by 5% WoW to USD 3,082.

Amid concerns that high US tariffs could redirect transpacific trade flows, the European Commission (EC) is closely monitoring containerized imports from China, fearing a potential influx of Chinese goods into Europe. Although there is no clear evidence yet of Chinese export volumes exceeding seasonal levels, the EC has taken a precautionary stance by deploying an Import Surveillance Task Force to track any unusual shifts in trade flows. A sudden surge in container traffic could worsen existing port congestion at several major European hubs. Meanwhile, alternative markets such as India are also bracing for a potential rise in Chinese exports, as China seeks to diversify away from the US market.

Although the tariff standoff has temporarily slowed China–US trade, the 90-day suspension of tariffs on other countries has prompted frontloading along those trade routes ahead of the Jul-25 deadline, in case negotiations collapse. As a result, there has been a notable increase in export volumes from other Far East countries via transpacific routes, with recent estimates suggesting that bookings from Southeast Asia to the US have risen by 20% in Apr-25. This uptick is partially offsetting the decline in freight demand from China. In response, carriers are considering redeploying blanked China–US capacity to these alternative lanes to accommodate rising demand. However, a sharp shift in volumes could strain infrastructure, potentially leading to port congestion, shipment delays, and equipment shortages, as the network adjusts to this rapid geographic reallocation of trade flows.

On the air cargo front, the impact of tariffs has been minimal, largely due to the de minimis exemption, which allowed Chinese e-commerce exports, valued under USD 800, to enter the US duty-free. According to the Freightos Air Index, air freight rates on the China–NA route rose by 1% WoW to USD 5.58 per kilogram (kg) in the last week of Apr-25, while rates on the China–NE route declined by 1% WoW to USD 3.71/kg. However, the suspension of de minimis eligibility for goods from China and Hong Kong on May 2, is expected to significantly disrupt China–US air cargo volumes and rates. Despite this, the May 12 agreement between the US and China to mutually reduce tariffs for 90 days has provided some relief. Under the revised terms, the tariff on small packages, valued up to USD 800, was reduced from 120% to 54%. Meanwhile, the flat fee of USD 100 per item for shipments sent after May 2 remains in place, but a planned USD 200 surcharge that was scheduled to begin on June 1 has been cancelled.

Tariff Increase Prompted Global Shift in Agricultural Trade Routes and Suppliers

The tariff hikes and retaliatory measures, coupled with fluctuating freight prices, have significantly impacted the global agricultural market and are expected to reshape trade supply chains, particularly regarding sourcing partners. For example, the US tea industry faces potential supply disruptions due to elevated import tariffs. The US relies on China, India, Argentina, and Sri Lanka for over 60% of its tea imports. With China subject to a 125% import tariff, tea from Chinese suppliers has become virtually unaffordable for many US consumers and could prompt a shift to alternatives like South Korean and Japanese green tea. Meanwhile, India, Argentina, and Sri Lanka are currently subject to a baseline 10% tariff, but they also face suspended tariffs ranging from 46% to 88%, set to be reinstated on July 9, unless further exemptions are granted.

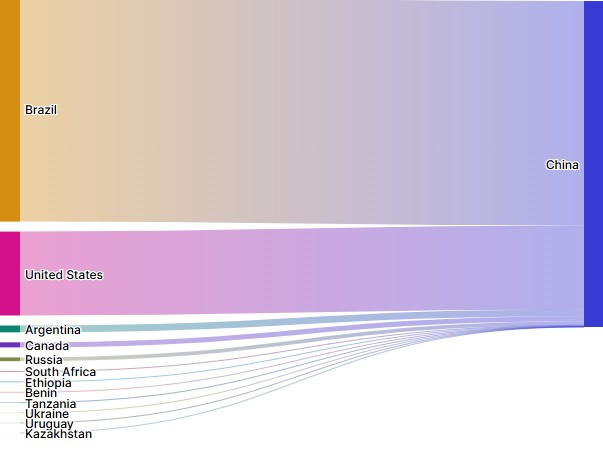

In the soybean and corn markets, China is actively diversifying away from the US, increasingly turning to Brazil as its primary supplier. The US–China tariff conflict has also affected the beef trade, resulting in a notable decline in US beef exports to China. This has been exacerbated by the expiration of export registrations for US meat plants, which China has not renewed since March 16. In response, China is expected to boost imports from alternative suppliers, including Brazil, Argentina, and Australia. These evolving trade relationships are likely to reshape traditional shipping routes and lead to further adjustments in freight costs across affected sectors.

Figure 3. Soybean Trade Flow Between China and its Top Trading Partners

Source: Tridge Eye

Looking ahead, the global market may experience temporary relief following the May 12 agreement between the US and China, under which both countries committed to rolling back reciprocal tariffs by 115% for a 90-day period starting May 14. This is expected to ease immediate supply chain pressures and revive trade flows between the two economies. A near-term rebound in ocean freight demand could signal the start of frontloading. However, a sharp rise in demand may lead to tight capacity and equipment shortages as vessels and containers are still being repositioned. US ports may also see a surge in vessel and container arrivals in the coming weeks. If the agreement holds and leads to a lasting resolution, it could help stabilize global freight prices and offer greater predictability for shippers amid ongoing trade uncertainty.