Indian Tea Export Set to Decrease 13% In 2021

Indian black tea production

India is the world’s second largest producer of tea after China with an annual production of around 139,490 MT and 1.1 million people employed in the industry. Around 90% of the tea produced in India is consumed domestically, yet India ranks fourth on global exporters list in terms of exported value.

The Indian tea industry considers 2020 to be an off-year, as Covid-related lockdown measures both in India during peak plucking seasons as well as other lockdown measures abroad affected production and exports tremendously. Hence, the baseline used for comparison of harvests post-Covid is typically 2019, where the tea production totaled 1,390,080 MT of which North India accounted for 84% (1,171,090 MT) and South India 16% (218,990 MT). For the calendar year 2021, the expectation, prior to data for November and December 2021 becoming available, is that the production will decrease by 40-45,000 MT compared to 2019 causing concern within the tea industry. The decrease in production for CY 2021 covers both a 39.000 MT decline in crop for North India and an increase of 25.000 MT in Southern India, and the expectation for November data is that North India production will be down 25% compared to November 2019.

Most of the tea produced in India is of the cut, tear, curl (CTC) type, that generally is cheaper and lower quality than orthodox tea. Orthodox tea production in India accounts for less than 10% percent of India’s total production with around 110,000 MT per annum. However, despite the relatively small proportion of all tea produced, orthodox tea remains an important export commodity as 90% of harvest tea is exported.

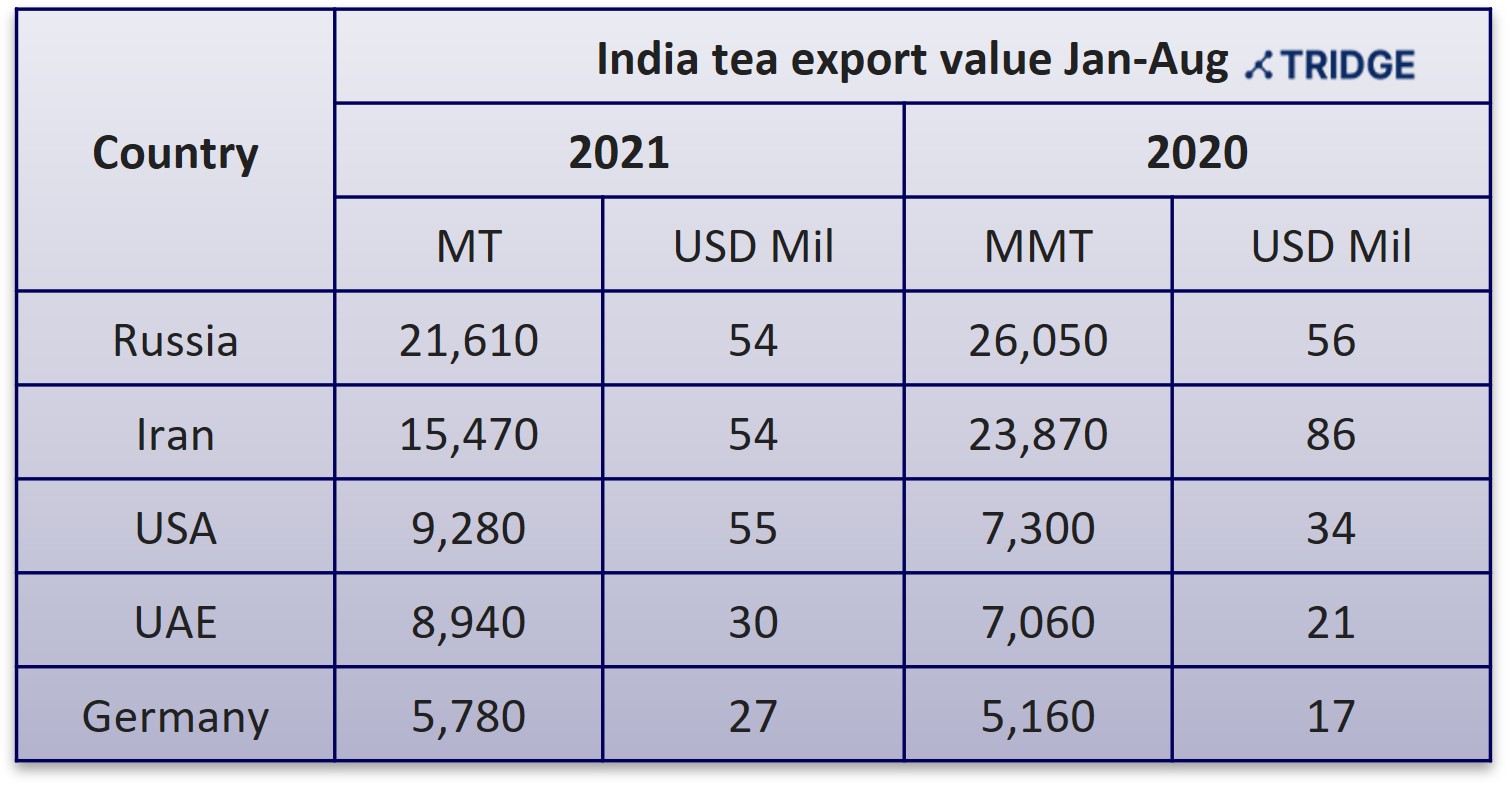

Export trends

In terms of export value India ranks fourth globally only behind China, Sri Lanka and Kenya.

In 2020, tea worth USD 692 million was exported from India with primary destinations being Iran, Russia, USA, UAE and UK. Currently, country-specific export data is available only for Jan-Aug 2021, but if the pattern from the first eight months of 2021 are representative for the full year, export volumes to Russia and Iran fall significantly, volumes for USA and UAE increase slightly while UK is replaced by Germany on the list of top five export markets.

Data source: Tea Board India

Export for CY 2021 estimated to reach 180,000 MT, down 13% from 207,580MT in 2020. The estimated fall is bad news for Indian exporters as it follows a 18% YoY drop in 2020 with the 2019 export totaling 252,150 MT. Comparing the estimated 2021 exports to the figures of 2019, the export volume is down 28.6%.

Data for Jan-October 2021 show that the exported quantity has declined 8.71% YoY from 172,190 MT in 2020 to 157,200 MT in 2021. Meanwhile, the export value has increased 1.58% from USD 5.44 billion in 2020 to USD 5.53 billion in 2021.

Challenges for Indian tea export

The reasons for the drop in exports are numerous, yet the Indian Tea Association ascribes the drop to mainly three factors: higher shipping costs, shortage of available containers and a pending resolution about Iran’s payment issues.

Shipping issues

As the prices of shipping worldwide have gone up due to increased demand and lockdown-related bottlenecks in ports, the tea exporters bear most of the extra cost since buyers refuse to share the burden of increased shipping prices. As an example, prices for a container from Kolkata to Rotterdam cost USD 9,500 in October 2021, and adding the premium prices for loading and ground handling, the total costs approached USD 20,000, which pressed the profit margins of tea exporters. The majority of sales cost and freight (CNF) contracts run for 1-2 year and buyers are unwilling to negotiate any revision of the prices. In addition, buyers are now seeking free on board (FOB) terms when closing deals, so that the seller will hold the risk of delays or damage to the shipped tea.

Previously, the Indian government has subsidized tea exports aiming to ease transport costs for exporters and bringing in foreign exchange. In 2009, tea exporters were eligible for a transferable duty credit of 7% of FOB value for value-added teas and 5% for bulk tea whereas the subsidies in 2021 are down to 1% as measurements have been taken by the Indian government to comply with rules laid out by the World Trade Organization.

Apart from the increased costs, the current shipping situation also offers unreliability with regards to timely delivery of shipments as normal delivery times were extended by 4 to 6 weeks from the autumn and towards the end of 2021. According to Sea-Intelligence, a logistics analyst firm, the probability of ships arriving on time in 2021 has been as low as 40% compared to the 2019 figure of more than 80% and this threatens the cash flow of tea exporters. Without price reductions on shipping and increased container availability and reliability, Indian tea exporters are looking into a rough 2022 - especially if deal structures remain unchanged.

Iran payment issues

Iran is a major buyer of Indian orthodox tea and in 2019, prior to the outbreak of Covid, they imported 54,450 MT corresponding to 21% of India’s total tea export volume. However, US-led economic sanctions against Iran have distorted the trade between India and Iran causing payment issues, since the two countries were not able to engage in dollar-denominated trades. As a workaround, a Vostro payment mechanism was set up whereby Indian oil refineries deposited rupees into designated banks as payment for the import of Iranian crude oil and then Iran used the deposited rupees to pay for any imports from India. With this mechanism in place, Iran managed to outcompete Sri Lanka as Iran’s main tea trading partner.

However, since May 2019 when sanctions against Iran were tightened, India has not imported oil from Iran leading to the rupee accounts running dry. Indian tea exporters are desperately hoping for a solution to the Iranian payments crisis, since Iran’s consistent demand for orthodox tea offers great market potential and because exporters have substantial outstanding dues waiting to be cleared. For the period of January-August 2021, the tea exports to Iran are down 35.2 percent YoY, with exports having dropped to 15,470 MT in 2021 from 23,870 MT during the same period of 2020. If a solution to the payment problem is found, sector experts have estimated that India could return to export levels in excess of 50,000 MT per year as experienced prior in 2019.

Nevertheless, India may face fierce competition from its southern neighbor Sri Lanka, as Iran and Sri Lanka finalized a dealin December 2021, wherein Sri Lanka will settle a USD 251 million oil debt by supplying tea to Iran.

Statistics from Tea Board India

STiR: Tea Logistics and Shipping Slip from Bad to Worse

STiR: The Worsening Logistics Situation

Firstpost: Iran to accept tea in payment for Sri Lankan oil debt

The Hindu Business Line: Indian tea sector set to face challenging times ahead

The Hindu Business Line: India’s tea exports expected to drop 13% in the 2021 calendar year

The Hindu Business Line: India’s tea exports expected to drop 13% in the 2021 calendar year

The Economic Times: Exporters confident of shipping 35 million kg of tea to Iran this year

The Economic Times: Iran keen to lift whole leaf teas from India, ready to pay good price