Macroeconomic Conditions: How Demographic Shifts Are Driving Agri-Food Demand Trends

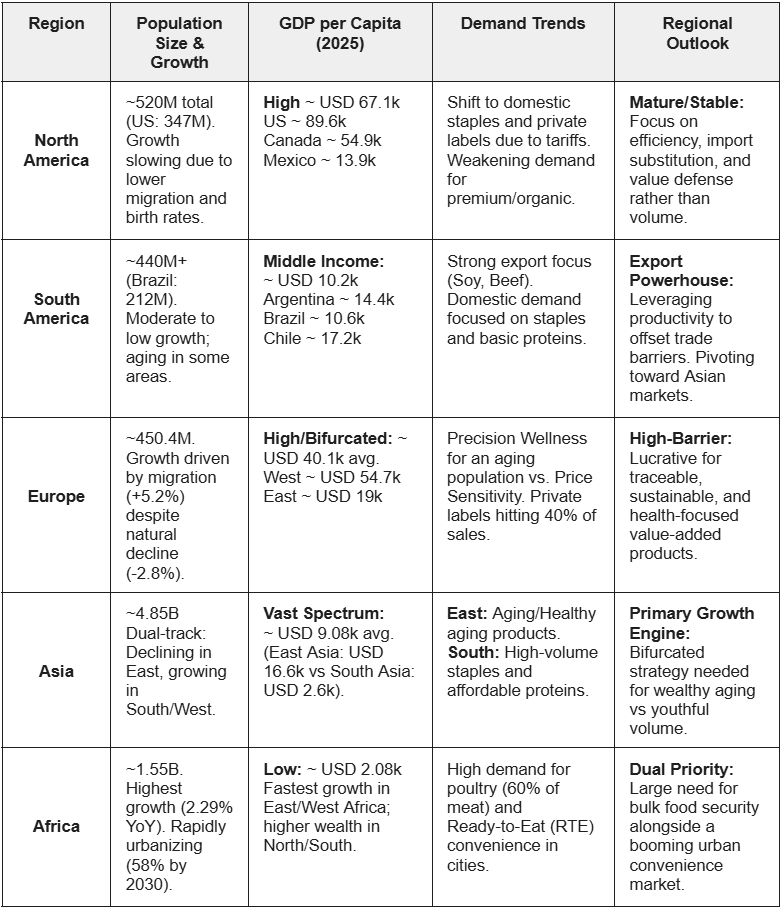

Table 1. Summary Table of Macro Economic Conditions by Region

North America

Figure 1. GDP per Capita in North America from 1980 to 2030

United States

In 2025, the US economy operated in a late-cycle slowdown, with elevated policy uncertainty, rather than a growth acceleration phase. Real gross domestic product (GDP) expanded by approximately 2% in 2025, supported mainly by AI-driven business investment and wealth effects, while consumer fundamentals weakened beneath the surface. For agriculture, this macro backdrop mattered less through headline GDP growth and more through tariffs, labor availability, interest rates, and consumer price sensitivity.

Trade policy was the most important macro variable for agriculture. The effective tariff rate rose sharply from ~2.5% at the start of 2025 to just above 10% by Aug-25, and under the baseline scenario is assumed to rise further to ~15% by Q1-2026, remaining elevated thereafter. For US agriculture, this had mixed effects. On the cost side, higher tariffs increased prices for imported fertilizers, agrochemicals, machinery, packaging, and food ingredients, pressuring farm margins and food processors. On the demand side, tariffs raised food prices gradually, contributing to higher inflation but also encouraging partial substitution toward domestic production in selected categories, notably grain- and oilseed-based processed foods (e.g., corn- and soy-derived ingredients replacing imported intermediates), and selected horticultural products such as processing vegetables (e.g., potatoes and processing tomatoes), where higher import costs improved the relative competitiveness of domestic supply. These effects primarily reflected demand reallocation rather than net consumption growth.

Monetary conditions were only modestly supportive. While the Federal Reserve System cut rates by around 1.50% in the second half of 2025 (H2-2025), long-term interest rates remained elevated, with the 10-year Treasury near 4%. This constrained capital-intensive agricultural investments, particularly in storage, processing capacity, and on-farm infrastructure. Credit conditions for farmers and agribusinesses tightened further as delinquency rates rose across consumer and small business lending.

For 2026, real GDP growth is expected to slow to ~1.9%, with inflation rising to ~3.1% as tariffs continue to pass through consumer prices. From an agricultural perspective, this signals a non-recessionary but demand-constrained environment: volumes hold up in staple categories, but value growth becomes increasingly difficult in discretionary and premium food segments.

Population Size and Growth

The US population stood at approximately 347 million in 2025, but population growth slowed materially due to a sharp decline in net migration. Net adult migration is now assumed at ~3.3 million between 2025 and 2030, down sharply from earlier expectations. This has two agricultural implications: slower long-term food demand growth and tighter labor availability, especially for labor-intensive segments such as fruits, vegetables, meat processing, and dairy. For 2026, the population growth forecast remains subdued, reinforcing the view that US food demand growth will be driven by prices and mix rather than volume expansion.

GDP per Capita

US GDP per capita remained very high in 2025, estimated at USD 89.6 thousand, supporting strong baseline purchasing power relative to most global markets. However, real per-capita income growth weakened as wage growth slowed, inflation remained elevated, and employment conditions softened. For agriculture and food markets, this means the US continues to support high absolute spending levels, but incremental growth is harder to capture, particularly for higher-priced or non-essential food products. In 2026, GDP per capita remains high, but consumers become increasingly price-sensitive, especially in lower- and middle-income segments.

Demand Trends

Staple foods and necessity-driven categories remain structurally resilient. Demand for grains, oilseeds, basic proteins (poultry, pork), dairy staples, and processed essentials remains stable in both 2025 and 2026. Tariff-driven food inflation supports nominal revenues, even as real volume growth slows. Health-driven consumption trends also support fresh produce, functional foods, and protein alternatives, although growth is uneven and income-segment dependent.

Input demand linked to productivity remains relatively strong. Despite higher borrowing costs, precision agriculture, digital farm management tools, and yield-enhancing inputs benefit indirectly from AI-driven investment and efficiency-seeking behavior across the farm sector. Demand for premium, discretionary, and value-added food products is forecasted to weaken in 2026. Categories such as premium organics, specialty imported foods, and higher-priced branded products face volume pressure as consumers trade down.

Import-dependent agricultural and food products face particular headwinds. Higher tariffs, slower consumer spending growth (real PCE slowing from 2.6% in 2025 to 1.6% in 2026), and rising price sensitivity limit growth opportunities for foreign suppliers targeting the US mass market.

Outlook

In 2025/26, the US remains a large but mature agricultural market, offering stability rather than growth. It is an attractive destination for staple foods and essential agricultural products, categories benefiting from import substitution and domestic sourcing, and productivity-enhancing agri-inputs and technologies that help offset higher costs and labor constraints. Opportunities also persist for premium or differentiated products aimed at higher-income consumers. However, the market is less attractive for undifferentiated, price-sensitive agricultural imports, products dependent on population growth or broad-based income expansion, and categories exposed to housing, credit, or discretionary spending cycles. Under the baseline scenario, the US supports volume defense and price-driven value capture, but does not offer broad-based demand expansion, making growth strategies reliant on rapid market scaling unlikely to succeed.

Canada

Canada entered 2025 in a materially weaker macroeconomic position than expected a year earlier, primarily due to rising global trade protectionism and elevated uncertainty stemming from the United States (US) tariff policy. Real gross domestic product (GDP) growth slowed sharply in the first half of 2025 (H1 2025), with annual growth projected at around 1.1% in 2025 and 1.2% in 2026, well below earlier expectations. Trade-exposed sectors have been the most affected, as higher tariffs and policy uncertainty weighed on exports, business investment, and manufacturing activity. While inflation has stabilised near the Bank of Canada’s 2% target and interest rates have declined, overall economic momentum remains subdued. For agriculture, this environment implies stable but cautious domestic demand, limited upside from macro-driven consumption growth, and continued cost pressure from imported inputs affected by tariffs and supply chain frictions.

Population Size and Growth

Canada’s population remains large by developed-market standards (around 41 million), but population growth slowed markedly in 2025 as immigration targets were reduced and temporary resident inflows declined sharply. This moderation has eased pressure on housing and services but also reduced a key driver of food demand growth seen in prior years. Looking into 2026, population growth is expected to remain positive but structurally lower than the 2022–2024 period. As a result, food demand growth increasingly reflects substitution and value shifts rather than volume expansion, limiting opportunities for broad-based agricultural demand growth.

GDP per Capita

Real GDP per capita has come under pressure, reflecting weak productivity growth and slower economic expansion. According to the IMF, Canada’s GDP per capita was USD 54.93 thousand in 2025. While wage growth has outpaced inflation for several quarters, gains are uneven and confidence-sensitive. Household spending has held up better than business investment, supported by easing inflation and lower interest rates, but consumers remain price-conscious. For agriculture, this means purchasing power supports staple consumption but constrains discretionary food spending, reinforcing a demand environment focused on essentials rather than premium volume growth.

Demand Trends

In 2025, Canadian agricultural demand remained defensive rather than expansionary. Staple categories such as grains, oilseeds, dairy basics, poultry, pork, and processed essentials have shown stable demand, supported by necessity consumption and domestic sourcing preferences. In contrast, demand growth has weakened for discretionary, premium, and highly price-sensitive food categories. Import substitution trends have modestly benefited domestically produced staples and processed foods, as higher tariffs and Buy Canadian policies improved relative competitiveness. However, Canada is not experiencing major new market openings or consumption booms comparable to developing regions. Agricultural inputs linked to productivity, cost efficiency, and domestic supply resilience (e.g. feed grains, oilseeds, functional ingredients) are better positioned than undifferentiated imports reliant on price competition.

Outlook

Canada in 2025/26 should be viewed as a stable but low-growth agricultural market. It is an attractive target for defensive strategies, including staple foods, domestically aligned supply chains, and products supporting productivity or cost control. However, it offers limited upside for volume-led growth strategies or for undifferentiated, price-sensitive agricultural exports. Success in Canada will depend on market positioning, substitution dynamics, and alignment with domestic sourcing and resilience trends, rather than on macroeconomic expansion or rapid demand growth.

Mexico

In 2025, Mexico operated in a context of macroeconomic stabilization rather than acceleration. Inflation fell sharply from above 8% to around 3.4% by year-end, supported by tight monetary policy, while the policy rate peaked near 11% before declining to ~7.25% by Dec-24. This disinflationary process eased cost pressures across the economy, including food production and processing, although financing costs for farmers and agribusinesses remained elevated for much of the year. The exchange rate remained notably stable, with the peso trading below 18–20 MXN/USD for most of 2025, reducing volatility for agricultural imports and exports. However, economic sentiment was constrained by uncertainty surrounding the United States-Mexico-Canada Agreement (USMCA) review and potential US tariff adjustments on Mexican products, which weighed on longer-term investment decisions, including in export-oriented agri-food value chains.

Looking into 2026, the macro outlook is mixed but constructive. Gradual interest rate cuts are expected to continue as long as inflation remains below 3.5%, supporting domestic credit, investment, and consumption. At the same time, risks tied to trade policy and US demand remain the main downside for agriculture, particularly for products heavily integrated into North American supply chains.

Population Size and Growth

Mexico’s population is approximately 130 million, with population growth slowing but remaining positive. Unlike developed markets, demographic dynamics continue to support baseline food demand growth, particularly for staple and low-cost food categories. However, growth is increasingly concentrated in lower-income households, reinforcing price sensitivity in food consumption.

GDP per Capita

Mexico’s GDP per capita remains structurally low relative to developed markets, at USD 13.97 thousand, but real purchasing power improved modestly in 2025 due to declining inflation and a 13% increase in the minimum wage. This wage policy strengthened domestic consumption, particularly for basic goods, including food. Nevertheless, high levels of labor informality, around 55% of employment, limit income stability and constrain sustained demand growth for higher-value agricultural and food products. In 2026, GDP per capita is expected to improve marginally in real terms, but consumption patterns will remain necessity-driven rather than premium-led.

Demand Trends

Agricultural demand in Mexico during 2025 was defensive and staple-focused, rather than expansionary. Demand for basic grains (corn, wheat), oilseeds, poultry, eggs, pork, dairy staples, and processed essentials remained stable, supported by population size, minimum wage increases, and the central role of food in household budgets. These categories benefit directly from domestic consumption resilience and government support mechanisms.

By contrast, demand growth weakened for premium, imported, or highly value-added food products, as households remained price-sensitive and informal employment limited discretionary spending. Import substitution trends modestly favored domestically produced staples and locally processed foods, particularly where exchange-rate stability and trade frictions raised the relative cost of imports. However, Mexico is not experiencing a broad opening of new agricultural consumption markets, unlike parts of South America, where rising incomes have supported rapid category expansion. Growth opportunities in Mexico are incremental and concentrated in volume-driven staple categories, not in premium or discretionary segments.

On the supply side, agriculture remains exposed to labor informality, productivity constraints, and climate variability, which cap the speed at which domestic production can respond to demand or export opportunities.

Outlook

Mexico in 2025/26 represents a large, structurally resilient, but low-income agricultural market. It is an attractive target for staple foods, cost-competitive agricultural products, and inputs aligned with domestic production and food security, particularly those benefiting from population scale and minimum wage-driven consumption support. However, it offers limited upside for premium, high-margin, or highly differentiated agricultural products, and does not constitute a “blooming” market in consumption terms. Under the baseline scenario, Mexico supports stable volumes rather than rapid growth, making it a suitable market for defensive positioning and scale-driven strategies, but less attractive for growth strategies dependent on rising purchasing power or broad-based market expansion.

South America

Figure 2. GDP per Capita in South America from 1980 to 2030

Brazil

In 2025, Brazil entered a phase of moderating but still solid economic growth. After expanding by 3.2% in 2023 and 3.4% in 2024, GDP growth slowed to around 2.2% in 2025, reflecting tighter global conditions but still supported by strong domestic consumption and recovering investment. Fiscal performance remained disciplined, with the primary balance staying within target ranges, reinforcing macro credibility. Investment activity continued to recover, reaching 17.3% of GDP by mid-2025, driven by machinery, equipment, and capital goods—sectors closely linked to agricultural productivity and logistics.

Labor market conditions were notably strong. Unemployment fell to 5.6% in Q3-2025, the lowest level for that period since 2012, while formal employment exceeded 59% of the labor force. Rising real incomes and declining inequality supported domestic demand, including food consumption, even as growth decelerated.

Inflation pressures eased partly due to the appreciation of the Brazilian real against the US dollar in 2025, which reduced imported cost pressures. At the same time, Brazil’s international reserves, around 16% of GDP, provided a strong buffer against external shocks, reinforcing exchange rate stability and policy credibility

Population Size and Growth

Brazil’s population exceeds 210 million, making it the largest consumer market in Latin America. Population growth is slowing, but the absolute size of the domestic market remains a structural anchor for agricultural demand. This supports large, stable consumption of staple foods, proteins, and processed agricultural products, even in periods of slower economic growth.

GDP per Capita

GDP per capita levels place Brazil in the upper-middle-income category, with gradual improvements supported by rising real wages and increased formalization of employment. In 2025, income dynamics favored basic consumption rather than discretionary spending. For agriculture, this translated into steady demand for staple foods and animal proteins, while limiting rapid expansion in premium or higher-value food categories within the domestic market.

Demand Trends

In 2025, agricultural demand was driven by both domestic consumption and exports. Domestically, demand remained firm for staple foods, poultry, beef, sugar, vegetable oils, and basic processed foods, supported by income gains and labor market strength. Export demand remained the dominant growth engine, with Brazil consolidating its position as a leading global supplier of soybeans, coffee, sugar, beef, chicken, and orange juice.

However, trade conditions deteriorated with the US. The imposition of additional US tariffs, raising the effective tariff rate on Brazilian exports to around 31%, significantly affected key agricultural categories such as coffee, meat, sugar, and wood products. Between Aug-25 and Oct-25, Brazilian exports to the US fell sharply, contributing to a widening bilateral trade deficit. This reinforced Brazil’s reliance on diversification toward Asia, the Middle East, and other emerging markets for agricultural exports.

At the policy level, Brazil advanced structural initiatives with long-term implications for agriculture. The launch of the Tropical Forest Forever Facility (TFFF) at COP-30 positioned conservation as a monetizable asset, potentially reshaping land-use incentives, especially in frontier agricultural regions. Additionally, the approval of progressive income tax reform, effective from 2026, reduced the tax burden on lower- and middle-income households, supporting domestic consumption while preserving fiscal neutrality.

Outlook

In 2026, Brazil’s agricultural outlook remains structurally strong but more complex. Economic growth is expected to remain moderate, supported by easing monetary conditions, stable inflation, and continued labor market resilience. Domestic food demand should remain stable, with incremental upside in basic proteins and processed staples rather than premium categories.

Externally, trade risks persist, particularly related to US tariff policy, which may continue to pressure specific export flows. At the same time, Brazil’s competitiveness, scale, and diversified export base position it well to redirect volumes toward alternative markets. Environmental finance initiatives such as the TFFF could increasingly influence investment flows, land values, and production decisions, especially for export-oriented agribusinesses.

Brazil in 2025–2026 should be viewed as a structurally attractive and resilient agricultural market, driven primarily by export capacity rather than rapid domestic consumption growth. It remains a strong target for staple commodities, proteins, and efficiency-driven agri-investments. While trade frictions and regulatory shifts introduce volatility, Brazil’s scale, productivity, and macroeconomic stability continue to underpin its central role in global agricultural markets.

Argentina

In 2025, Argentina entered a phase of macroeconomic reordering, characterized by strict monetary discipline, fiscal adjustment, and a clear policy focus on disinflation. Inflation decelerated sharply but remained elevated, with Dec-25 Consumer Price Index (CPI) at 31.5% year-on-year (YoY), reflecting both progress and ongoing price rigidity. The monetary framework remained tight throughout the year, resulting in high real interest rates and constrained credit conditions. For agriculture, the macroeconomic environment created clear trade-offs. Improved monetary discipline reduced price distortions and increased predictability in input and output markets. At the same time, elevated interest rates constrained access to credit, limiting working capital availability for smaller producers and for production systems with high input requirements.

The exchange-rate regime remained managed but more predictable than in prior years, improving planning for export-oriented sectors. Given agriculture’s strong export orientation, this relative Foreign Exchange (FX) stability supported export flows, particularly in grains and oilseeds, while still preserving competitiveness. However, lingering capital controls, tax distortions, and uncertainty around policy durability continued to limit longer-term investment in agricultural infrastructure and value-added processing.

Population Size and Growth

Argentina’s population stands at approximately 45.5 million, with very low population growth and low population density. Demographic dynamics are broadly neutral for agricultural demand; the market is large enough to absorb staple consumption but does not benefit from population-driven volume growth. As a result, food demand growth is primarily influenced by income levels, inflation, and purchasing power rather than demographics.

GDP per Capita

GDP per capita remains low by upper-middle-income standards, at around USD 14,721 (EUR 12,500), reflecting constrained household purchasing power after years of high inflation and economic adjustment. In 2025, real incomes stabilized as inflation decelerated, but consumption capacity remained uneven. For agriculture, this reinforces demand for affordable staples while limiting expansion in higher-value or discretionary food categories, except for export-oriented segments.

Demand Trends

In 2025, demand remained resilient for essential food products such as grains, vegetable oils, bread, pasta, poultry, and basic dairy, as households prioritized necessities amid inflation and income pressure. Demand for premium foods, branded products, and higher-value proteins remained subdued in the domestic market, while export demand continued to drive growth in soy, corn, wheat, beef, and oilseed products. No major new domestic consumption markets emerged; volume stability rather than expansion defined internal demand.

Outlook

In 2026, Argentina’s agricultural demand outlook remains stable but uneven. Continued disinflation and macro stabilization may gradually improve real incomes, supporting marginal recovery in food consumption, but meaningful domestic demand growth is unlikely. Argentina remains a strong target for agriculture primarily as an export platform rather than a consumption growth market. Opportunities favor staple foods, cost-efficient production systems, and export-linked value chains, while strategies dependent on rapid domestic demand expansion face structural limitations.

Chile

In 2025, Chile consolidated its macroeconomic normalization after the post-pandemic adjustment period. GDP growth reached around 2.4%, driven primarily by a strong recovery in domestic demand rather than exports. Private consumption benefited from real wage growth and easing financial conditions, while investment rebounded sharply, particularly in machinery, equipment, mining, energy, and infrastructure. Inflation declined steadily, reaching 3.4% by October 2025, within the Central Bank’s target range, allowing for gradual monetary easing and improved financing conditions for firms.

Fiscal policy remained anchored in consolidation. The government reaffirmed its commitment to the fiscal rule, targeting a cumulative adjustment of around 1% of GDP over 2025–27, supported by spending restraint and tax-base broadening. Institutional reforms, notably the Framework Law on Sectoral Permits and advances in digital government, improved the investment climate by reducing regulatory uncertainty and processing times—an important factor for agribusiness, logistics, and export-oriented projects.

Externally, Chile benefited from improved terms of trade, supported by strong copper demand and lower energy prices. While export growth underperformed expectations in 2025 due to mining-related investment disruptions, macro stability, low effective tariff exposure to the US, and Chile’s integration into global trade agreements (notably the CPTPP) preserved external resilience.

Population Size and Growth

Chile has a population of roughly 20 million and exhibits low population growth, limiting demographic-driven expansion in food demand.

GDP per Capita

Chile maintains one of the highest GDP per capita levels in Latin America, placing it firmly in the upper-middle-income category. In 2025, recovering real incomes supported household consumption, particularly for food and essential goods. For agriculture, this income level sustains demand for higher-quality food products and diversified diets, though growth remains incremental rather than expansive.

Demand Trends

In 2025, domestic agricultural demand remained stable, supported by rising real wages and improved consumer confidence. Demand was strongest for staple foods, fresh produce, poultry, pork, and processed essentials, while discretionary and premium food categories expanded more gradually. Export-oriented agriculture remained the main growth driver, with continued strength in fruit (grapes, cherries, berries), wine, salmon, forestry products, and processed foods.

Trade conditions were broadly supportive. Chile was largely insulated from US tariff measures, as copper and timber were exempt, and effective tariff exposure remained low. Export diversification through CPTPP markets provided additional resilience. However, export growth in 2025 was more moderate than previously expected, reflecting weaker mining output and logistical adjustments rather than agricultural constraints.

Outlook

In 2026, GDP growth is expected to ease slightly to around 2.2%, reflecting normalization after the investment rebound, but the composition of growth remains supportive for agriculture. Investment is projected to continue expanding, albeit at a slower pace, and domestic demand should remain stable as inflation stays near target and credit conditions gradually improve.

For agriculture, the outlook points to steady rather than accelerating demand. Domestic consumption is expected to grow modestly, while export performance should gradually improve as global demand stabilizes and investment-related disruptions fade. Chile’s strong institutional framework, open trade regime, and regulatory improvements continue to favor export-oriented agribusiness, particularly in high-value and counter-seasonal products.

Chile in 2025-26 represents a stable, low-risk agricultural market with limited domestic volume growth but strong structural appeal for export-oriented and value-added agricultural products. It is well suited for strategies focused on quality, traceability, and access to global markets rather than on the rapid expansion of domestic consumption.

Europe

In 2025, the European economy navigated a period of significant trade turbulence and structural adjustment, with real GDP growth estimated at 1.4% in the European Union (EU) as the region absorbed the impact of aggressive US trade policy. The volatility of the US tariff shocks was particularly acute given that the EU typically exports approximately 8.2% of its total goods and services to the US while importing 6%, a relationship that historically supports a substantial trade surplus. Fortunately, some semblance of stability has been achieved with the issuance of the Joint Statement on a US-EU framework on an agreement on reciprocal, fair and balanced trade on 21 August 2025, which established a headline tariff rate of 15%. Compared to other major global players, the EU enjoys lower trade-weighted average tariff rates on exports to the US, providing a relative advantage for the EU economy. The European Commission (EC) forecasts real GDP to grow by 1.4% in the EU in 2025 and 2026, edging up to 1.5% in 2027. This period of relative stability is largely driven by a stabilization in trade relations with the US combined with a strategic pivot toward trade diversification, as the EU seeks to reduce its reliance on the transatlantic corridor.

A cornerstone of this diversification strategy was the landmark conclusion of the EU-India Free Trade Agreement (FTA) in late 2025 and the subsequent progress of the EU-Mercosur agreement in early 2026. The India FTA is expected to double EU goods exports to the world’s most populous country by 2032, notably by slashing prohibitive tariffs on premium agri-food products like wine, cheese, and olive oil. Similarly, the deal with the Mercosur bloc provides privileged access to nearly 300 million South American consumers, creating a vital outlet for high-value European dairy and processed foods while securing stable supply chains for raw agricultural inputs. Together, these agreements represent a decisive shift toward strategic autonomy, allowing the EU to de-risk its economic outlook by fostering deeper ties with the Global South and emerging Asian markets.

Population Size and Growth

The EU’s population was estimated at 450.4 million on January 1 2025, 1,070,702 more than the previous year. This represents a total increase of 2.4%, consisting of a -2.8% natural change and 5.2% increase in migration. The negative natural change (more deaths than births) has been a consistent trend since 2012. During the period from 2012 till present, the EU has experienced consistent positive population growth, with the exception of 2020 during the COVID-19 pandemic (-2.1% total change). Thus, the observed population growth can be largely attributed to the increased migratory movements, especially post-COVID-19, when migration growth increased significantly.

While Western and Northern Europe continue to see marginal growth driven by net migration, Eastern and Southern Europe are facing sharp natural declines and aging workforces. This is particularly acute in Eastern European countries like Poland, Hungary, and Romania, as well as Italy in the South. For the agri-food sector, this demographic shift is simultaneously tightening the agricultural labor market and shifting consumer demand toward functional foods designed for aging populations, such as high-protein dairy and specialized clinical nutrition.

GDP per Capita

According to the International Monetary Fund (IMF), GDP per capita in the EU in 2025 was USD 46.8 thousand, up from USD 43.26 thousand in 2024, and with a projected growth to USD 49.88 thousand in 2026. However, there is a clear divide between Western and Eastern Europe. While Western Europe maintained a GDP per capita of USD 54.74 thousand in 2025, the GDP per capita in Eastern Europe was less than half that at USD 19.02 thousand. This has led to a dual-speed market where high-income segments in Western Europe continue to prioritize premium certifications like organic and provenance-based goods, while middle- and lower-income households, particularly in Eastern Europe, remain focused on necessity-driven consumption and private-label staples due to lower absolute purchasing power.

Figure 3. GDP per Capita in Europe from 1980 to 2030

Demand Trends

Agri-food demand across Europe in 2025 and going into 2026 is increasingly characterized by a more value conscious consumer as Europeans navigate the aftermath of significant food inflation experienced during the COVID-19 era. While headline inflation has begun to stabilize, only rising by 2.8% YoY in 2025, specific categories witnessed dramatic price surges in 2025. Chocolate prices rose the most, up 17.8%, while frozen fruit followed at 13%, and beef and veal increased by 10%. Dairy and animal protein products also continue to experience above inflation increases. For example, egg prices rose by 8.4%, followed by butter at 8.3% and lamb and goat at 7.2%, while fresh whole milk increased by 5.7%. Within the EU, Romania recorded the highest food inflation at 6.7%. Food inflation remained high across parts of Eastern and Southeastern Europe in 2025. Romania, Bulgaria, the Baltic states and the Balkans mostly saw rates between 4% and 7%, well above the EU average.

In response, the European market has seen a shift toward private-label brands, which now account for nearly 40% of grocery sales value according to McKinsey & Company’s The State of Grocery Retail Europe 2025. This inflationary pressure is a primary driver behind the strategic importance of the EU-Mercosur FTA. By lowering trade barriers, the deal is expected to provide a crucial deflationary buffer once entered into force, particularly for the meat sector. Increased access to competitively priced beef and poultry from South America offers a structural mechanism to offset high domestic production costs and stabilize protein prices for European households.

Beyond price sensitivity, demand is being reshaped by a sophisticated Precision Wellness trend. Consumers are increasingly moving away from ultra-processed foods (UPFs) in favor of clean label and functional products that support gut health, heart health, and healthy aging. This is manifesting in a growing appetite for protein-fortified staples and plant-based options that prioritize natural, recognizable ingredients over highly engineered substitutes. Furthermore, high-quality ready-to-eat meals are growing in popularity, especially among Gen Z and Millennial consumers. McKinsey found that 42% of Gen Z shoppers and 37% of Millennials purchase ready-to-eat meals at least once a week. Finally, the postponement of the EU Deforestation Regulation (EUDR) to late 2026/mid 2027 has shifted immediate corporate demand toward digital traceability infrastructure, which allows firms use the 12-month grace period to ensure their newly diversified supply chains from Mercosur and India are fully compliant with the upcoming transparency mandates.

Outlook

In 2026, the EU will continue to be defined by its duality as a market. It remains a high-volume destination for raw agricultural commodities while simultaneously serving as a premium, high-barrier arena for specialized food products. The EU remains an essential market for bulk agricultural products to feed its domestic processing industries. Tighter environmental regulations and rising production costs are creating a structural deficit in domestically produced raw materials. Consequently, the region is a prime destination for exporters of animal proteins, dairy ingredients, and feed grains, particularly those from the Mercosur bloc, which could provide competitively priced solutions to the European market and provide deflationary relief to European consumers.

Simultaneously, the EU continues to be a lucrative global market for companies targeting branded value-added product segments. Success in this segment requires navigating a complex intersection of sustainability and health mandates, from the Clean Label movement to the stringent traceability requirements of the EUDR. With the conclusion of the India and Mercosur trade deals, the market is opening further to suppliers who can bridge the gap between competitive pricing and high-standard compliance. For agri-food companies, the 2026 European market offers stability through its demand for raw industrial inputs and lucrative growth for those who can deliver traceable, sustainable, and health-focused innovations to an increasingly bifurcated and discerning consumer base.

Asia

In 2025, the Asian economy demonstrated unexpected resilience, contributing approximately 60% of global growth despite a strained transatlantic trade environment with the US. According to the IMF, real GDP growth is estimated at 4.5% for 2025, with a projected moderation to 4.1% in 2026. The resilience against trade tensions with the US on the Asian continent in 2025 can be attributed to front-loading of exports ahead of new levies, stronger-than-expected investment in artificial intelligence, ongoing supply-chain reconfiguration within the region, and policy easing in some countries. Asia exhibits significant variation in growth between countries, however, China and India, the two largest players in the region maintain high growth rates. China’s economic growth is forecast to slow from 4.8% in 2025 to 4.2% this year. India grew even faster at a healthy pace of 6.6% in 2025, the most among major emerging economies, while it is expected to slow to 6.2% in 2026. Japan’s economy is expected to decelerate from 1.1% to 0.6% in 2026. South Korea’s growth will accelerate from 0.9% in 2025 to 1.8% this year. The Association of Southeast Asian Nations (ASEAN) economies will expand by 4.3% for a second straight year.

Trade policy has served as a strategic stabilizer for Asia in 2025. While the region absorbed shocks from elevated US tariffs, a pivotal roll-back of US duties on approximately 200 food items in late 2025 provided a tailwind for Asian agricultural exporters. Furthermore, the Regional Comprehensive Economic Partnership (RCEP) is now entering its fifth year of implementation, with intra-ASEAN trade growing by 7.03% in 2024. By 2026, the reduction of tariff and non-tariff barriers and the streamlining of supply chains are facilitating a more efficient regional food system, promoting intra-continental trade while de-risking from Western market volatility, especially US volatility.

For the agri-food sector, the macro environment is defined by low inflation averaging 1.6% in developing Asia in 2025, with an estimated uptick to 2.1% in 2026. According to the Asian Development Bank, the low inflation across the region in 2025 can largely be attributed to low food inflation in India. With the GDP growth rate across Asia outpacing headline inflation by a comfortable margin, it can tentatively be assumed that the disposable income of Asian consumers is steadily on the rise.

Population Size and Growth

The population in Asia and the Pacific continues to grow, but at a declining rate. In 2025, there were 4.85 billion people living in the region, representing about 60% of the total global population. In 2025, the overall population in Asia grew an estimated 0.58% YoY. This represents a significant decline from the +1% experienced only 15 years ago, suggesting continued slowing population growth across the region. Nonetheless, Asia remains the world’s demographic heavyweight, though it is increasingly characterized by a duality within the region.

On the one hand, countries such as China (-0.22%), Taiwan (-0.44%), Japan (-0.55%), South Korea (-0.13%) and Thailand (-0.08%) in South and Southeast Asia experienced negative growth in 2025, experiencing a combined population decline of more than 4 million people. On the other hand, large countries such as Vietnam (0.57%), Indonesia (0.76%) and the Philippines (0.8%) in Southeast Asia and India (0.87%), Bangladesh (1.21%) and Pakistan (1.6%) in South Asia experienced substantial growth, adding an estimated 22.65 million people to the total population growth figure. However, the highest population growth was experienced in the Middle East, with most countries in the region experiencing population growth north of 1%, with countries with populations between 40 and 50 million such as Iraq, Afghanistan and Yemen experiencing population growth north of 2%.

There are clear regional divides within Asia. Overall, more developed countries, primarily located in East Asia, are experiencing population declines, while developing countries in the region are primarily experiencing population growth. Countries with declining populations will struggle with aging populations. These trends have a clear impact for agri-food trade going into the future.

GDP per Capita

According to the IMF, Asia and the Pacific region had a GDP per capita of USD 9.08 thousand in 2025, estimated to grow to USD 9.59 thousand in 2026, a growth rate of 5.62%. However, Asia presents a vast spectrum of purchasing power, characterized by significant regional differences. For example, East Asia has a GDP per capita of six times that of South Asia. East Asia is the wealthiest region with a GDP per capita of USD 16.65 thousand in 2025, followed by Central Asia and the Caucasus at USD 12.15 thousand. At half that value, Southeast Asia comes in at USD 6.01 thousand with South Asia coming in last, halving the value of Southeast Asia at USD 2.67 thousand.

Over the past five years, Central Asia and the Caucasus has shown the most significant growth, increasing from USD 5.24 thousand in 2020, more than doubling its GDP per capita during this period. This is largely due to significant growth in Turkey, Kazakhstan, Turkmenistan and Georgia. The wealthiest countries are located in East Asia and Southeast Asia. In East Asia, Macao and Hong Kong, two Special Administrative Regions (SAR) of China, Japan, Taiwan and South Korea stand out while Brunei and Singapore stand out in Southeast Asia. Lastly, Oxford Economics estimates that the middle class population in emerging markets is set to double over the next decade, expanding from 354 million households in 2024 to 687 million households by 2034. China and India represent the largest markets, expected to add more than 100 million middle class households in the five years spanning 2024 to 2029.

Figure 4. GDP per Capita in Asia from 1980 to 2030

Demand Trends

Agri-food demand across Asia is increasingly characterized by a sharp regional divergence in population dynamics and purchasing power. In the more developed economies of East Asia (China, Japan, South Korea) and parts of Southwest Asia, high GDP per capita is paired with declining and aging populations. This shift has catalyzed a Precision Wellness movement, where roughly 34% of Asian consumers are now actively seeking age-specific nutrition, according to Innova Market Insights. In these markets, demand is pivoting away from volume toward high-value, functional products that cater to the silver economy driven by an aging population, such as high-protein dairy, specialized senior nutrition, and products focusing on health and functional benefits.

In contrast, South Asia and parts of the Middle East present a vastly different demand profile. With populations growing much faster and a significantly lower GDP per capita, these regions remain best suited for high-volume, cost-competitive staple products. For these large, youthful populations, food security and affordability remain the primary drivers, sustaining robust demand for bulk grains, vegetable oils, and basic proteins. However, even in these price-sensitive markets, there is a growing interest in traditional foods, with over 70% of Asian consumers expressing a desire for modernized versions of traditional recipes that offer better nutritional profiles without sacrificing cultural authenticity.

Outlook

In 2026 and beyond, the Asian agri-food sector will remain the primary food market in the world, especially with its rapidly growing middle class population. The long-term opportunity is defined by a distinct geographic dual-track strategy. East Asia (China, Japan, South Korea) and parts of Southeast Asia will increasingly demand high-value, health oriented functional food solutions to serve an aging but wealthy population, making it an ideal market for precision wellness and functional food products. Conversely, South Asia, the Middle East, and large parts of Southeast Asia will remain one of the world's most critical volume markets, where the combination of rapid population growth and urbanisation will sustain large demand for staple commodities and affordable proteins. For agri-food stakeholders, the 2026 and beyond era in Asia is no longer just about capturing scale, it is about navigating a sophisticated, bifurcated market where success depends on the ability to provide either large-scale nutritional security for the growing South or high-standard, value-added innovation for the aging East.

Africa

According to the IMF, Africa exhibited real GDP growth of 4.2% in 2025, with a slight uptick to 4.3% expected in 2026. This equates to an economy worth just north of USD 3.3 trillion USD, a substantial market that cannot be ignored in the agri-food trade in 2026. However, there are significant differences in growth rates across the continent. According to the African Development Bank, East Africa was projected to grow the fastest in 2025 at 5.9%, driven by resilience in Ethiopia, Rwanda, and Tanzania. West Africa maintains solid 4.3% growth, driven by new oil and gas production coming onstream in Senegal and Niger. In the face of persistent headwinds, North Africa is expected to register 3.6% growth in 2025. In Central Africa, growth was projected to slow to 3.2% and Southern Africa was projected to grow at only 2.2%, with its largest economy, South Africa, expected to achieve only 0.8% growth.

Trade dynamics across Africa in 2025 were shaped by an accelerated strategic pivot away from traditional Western dependencies, largely driven by US tariff pressure. While high US tariffs on global industrial goods had a ripple effect on African trade financing, the continent benefited from specific exemptions for key agricultural exports. This movement prioritizes intra-continental trade and partnerships with the Global South, de-risking the region from transatlantic volatility. For example, South Africa’s agricultural exports reached a historic high of USD 15.1 billion in 2025, marking a 10% YoY increase. While new US tariffs weighed heavily on selected South African agricultural products, especially in the second half of 2025, South Africa offset those losses by deepening trade ties across the African continent as well as with Asia. Africa accounted for 54% of South Africa’s agricultural exports in Q4-2025, followed by Asia and the Middle East at 17%, and the EU at 16%. Meanwhile, the US accounted for only 4% of exports, with agricultural exports to the US declining 11% in Q3-2025 and accelerating to a 39% decrease in Q4-2025. The South African case study highlights how the African continent is accelerating intra-continental trade and de-risking away from Western markets by focusing on Asia.

Population Size and Growth

The population in Africa continues to grow, but at a declining rate. In 2025, there were 1.55 billion people living in the region, representing about 18.5% of the total global population. In 2025, the overall population in Africa grew an estimated 2.29% YoY. The population growth in Africa has been on steady decline since 2013 when the growth rate was at 2.65%. According to the African Development Bank, the African population is expected to grow to 2.4 billion people by 2050. However, there are significant regional variations across the continent.

Eastern Africa has the largest population by region on the African continent at 513 million people, growing at a rate of 2.55% in 2025, with Ethiopia being the most populous country at 135 million people or around 16% of the population share. Western Africa has the second largest population at 466 million people, growing at a rate of 2.25% in 2025, with Nigeria being the most populous country by far at 237 million people or around 50% of the population share. Northern Africa had a population of around 276 million people in 2025 growing at a rate of 1.53%, with Egypt being the largest country in the region at 118 million people or around 43% of the population share. Middle Africa had a population of around 219 million people in 2025 growing at a rate of 3.1%, the highest on the continent with the Democratic Republic of the Congo being the largest country in the region at 113 million people or around 52% of the population share. Lastly, Southern Africa is by far the smallest region at 74 million people, also growing at the slowest rate on the continent of 1.21%. South Africa is the largest country in the region with an estimated population of 65 million people, representing 88% of the population share in the region.

According to the African Development Bank, the urban share of the population has doubled over the past 50 years to 39%, which equates to more than 360 million city dwellers. By 2030, the urban share of the population is expected to increase to 58%, adding an additional 350 million city dwellers. This means that Africa is the fastest urbanizing continent in the world. This will have significant impacts for the agri-food trade in the form of changing consumption patterns and consumer needs.

GDP per Capita

Africa is the poorest continent on the planet when measured by GDP per capita. According to IMF data, in 2025, the entire African continent had a GDP per capita of USD 2.08 thousand growing at a rate of 4.2%. However, simply looking at the macro statistics masks significant regional variations. North Africa and Southern Africa maintain higher purchasing power, while East Africa is leading the continent in growth momentum. In North Africa, Morocco (USD 4.76 thousand), Algeria (USD 6.1 thousand), Tunisia (USD 4.75 thousand), Libya (USD 6.87 thousand), and Egypt (USD 3.19 thousand) have GDPs per capita significantly above the average, while South Africa (USD 6.67 thousand), Namibia (USD 4.82 thousand), and Botswana (USD 6.94 thousand) in Southern Africa have significantly above average GDPs per capita. This highlights significantly more purchasing power in the North and South extremes of the continent.

However, the fastest growth on the continent is taking place in the East. The fastest growing economies in the Eastern part of Africa in 2025 include South Sudan (24.3%), Ethiopia (7.2%), Uganda (6.4%), Rwanda (7.1%), Tanzania (6%), and Zambia (5.8%), all of which grew north of 5%. However, there are also several fast growing economies in the horn of Africa in the west, including Guinea (7.2%), Benin (7%), Niger (6.6%), and Côte d'Ivoire (6.4%). Although Africa remains the poorest continent, it has wealthier economies in the North and South and some fast growing economies in the East and West that warrant market attention and investigation.

Figure 5. GDP per Capita in Africa from 1980 to 2030

Demand Trends

The agri-food demand landscape in Africa in 2026 is defined by a transition toward convenience, nutritional fortification, and affordable proteins, driven primarily by the continent’s high urbanization rate. In terms of affordable protein, chicken has solidified its position as Africa’s primary animal protein, now accounting for 60% of total meat consumption in leading markets like South Africa. By 2026, domestic production is scaling rapidly to meet urban demand; for instance, South Africa’s chicken meat production is forecast to reach 1.68 mmt in 2026, a 2% increase supported by recovering grain harvests and lower feed costs. This trend is mirrored across West and East Africa, where poultry is favored for its price competitiveness over beef and its suitability for quick-service urban retail.

Rapid urbanization and the rise of a time-constrained middle class are fueling significant growth in the Ready-to-Eat (RTE) food market. In South Africa, the RTE market alone is projected to grow from USD 2.86 billion in 2024 to over USD 5.44 billion by 2032, maintaining a robust CAGR of 8.49%. By 2026, the demand for convenience-oriented meat products is expected to be the fastest-growing sub-segment, expanding at an annual rate of over 9% as urban professionals prioritize protein-rich, grab-and-go options. This shift is most pronounced in large, economically developed cities like Lagos, Nairobi, and Johannesburg, where busier lifestyles and limited time for traditional meal preparation have made shelf-stable, chilled, and frozen ready-meals and functional snacks essential.

Outlook

In 2026 and beyond, Africa represents a dual-priority agri-food market. The region is undergoing a structural shift where the demand for basic food security through bulk commodities is increasingly running parallel to a burgeoning urban appetite for sophisticated, value-added products. This urban pivot is driven by a city-dwelling population expected to reach 58% of the continent’s population by 2030, creating a consumer base with lifestyle preferences increasingly aligned with global developed markets. While the demand for value-added products grows, Africa’s dependence on grain imports, specifically wheat and rice, remains a structural necessity. The challenge for 2026 and beyond is bridging the gap between ever increasing input costs and domestic price sensitivity.