Global cheddar markets entered 2026 under sustained downward price pressure, driven by ample milk supplies and elevated cheese inventories across major exporting regions. In W1 2026, EU cheddar prices fell amid persistent oversupply, while US prices showed only temporary holiday-related support and remained bearish YoY. Oceania prices were comparatively stable but continued to face downside risks as processors redirected milk from weak powder markets into cheese. Looking ahead, USDA projections point to rising global milk and cheese production, led by the US and Oceania, while the EU faces tighter milk supplies but still prioritizes cheese output due to favorable margins. As a result of this, exporters are recommended to shift away from spot-market exposure toward structured, medium-term supply contracts, and expand exports into high-growth and price-sensitive markets. They should also accelerate value addition through branded, specialty, and customized cheese formats to protect margins and reduce vulnerability to price volatility.

1. Weekly Price Overview

Ample Milk Output Drives Cheddar Price Weakness Across Major Exporting Regions

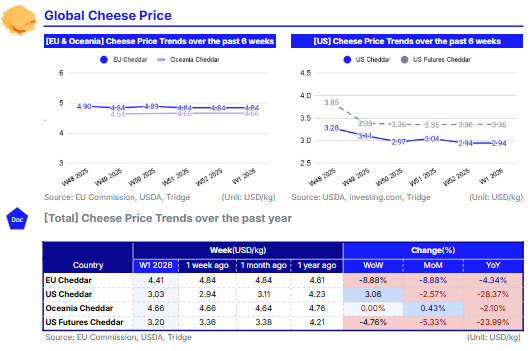

In W1 2026, European Union (EU) cheddar cheese prices averaged USD 4.41 per kilogram (kg), marking an 8.88% decline both week-on-week (WoW) and month-on-month (MoM), alongside a 4.34% year-on-year (YoY) drop. This sustained downward pressure reflects structural supply issues, as robust milk production across the region has continued to outpace demand, leading to elevated cheese inventories and forcing sellers to reduce offers to clear stocks.

In the United States (US), cheddar spot prices rose 3.06% WoW to USD 3.03/kg, supported by holiday-related buying, but remained 2.57% lower MoM and 28.37% lower YoY, underscoring the broader bearish trend. This weakness is reinforced by the futures market, where prices averaged USD 3.20/kg, falling 4.76% WoW, 5.33% MoM, and 23.99% YoY, signalling expectations of continued oversupply. Both domestic output and ample global availability are weighing on prices. However, US cheese remains highly competitive relative to other exporters, which has helped drive export volumes, partially cushioning the domestic market.

In Oceania, cheddar prices averaged USD 4.66/kg, remaining stable WoW, edging 0.43% higher MoM, but still 2.10% lower YoY. The weekly stability reflects steady domestic demand, yet underlying supply remains firm. Weaker international demand for milk powders is prompting processors to redirect more milk into cheese production, keeping output elevated even as seasonal milk collections begin to decline. As a result, Oceania’s cheese market is currently supported by local consumption but continues to face downside pressure from globally ample dairy supplies.

2. Price Analysis

Global Cheese Markets Face Rising Supply as Major Exporters Expand Output in 2026

In Dec-25, the Food and Agriculture Organization (FAO) global dairy price index averaged 130.31 points, a 4.37% MoM decline driven by broad-based weakness across major dairy commodities. Within this, the cheese price index fell by 1.84% MoM to 140.36 points, as ample supplies and slowing European export demand more than offset firmer prices in New Zealand. In Oceania, peak seasonal milk flows continue to be absorbed primarily by butter and milk powder production, which offer greater processing flexibility, limiting upward momentum in cheese prices.

Looking ahead to 2026, the United States Department of Agriculture (USDA) projects milk production across major exporting regions to rise by 0.4% YoY to 293.39 million metric tons (mmt), with growth in the US, Australia, and Argentina outweighing modest declines in the European Union (EU) and New Zealand. In the US, this expanding milk pool is expected to support a 3% YoY increase in cheese production to 621 thousand metric tons (mt), reinforced by ongoing investments in manufacturing capacity. At the same time, US cheese exports are forecast to exceed 620 thousand mt, underpinned by ample supplies and strong price competitiveness on global markets.

In contrast, the EU faces a more constrained milk outlook, with production projected to decline by 0.5% YoY to 144.8 mmt in 2026. Despite this, cheese output is expected to edge higher to 10.8 mmt, as processors continue to prioritize cheese over butter, whole milk powder (WMP), and skim milk powder (SMP) due to superior processing margins. However, EU cheese exports are forecast to fall by 1% YoY to 1.4 mmt, as strong domestic demand and relatively elevated prices encourage a larger share of production to remain within the internal market.

Meanwhile, Oceania is set to expand its role in global cheese supply. New Zealand’s cheese production is forecast to rise by 4% YoY, supported by investments in processing capacity and sustained export demand, while weaker returns for milk powders further incentivize milk allocation to cheese. As a result, New Zealand cheese exports are projected to grow by 2% to 425 thousand mt, which would mark a record high if realized. Australia’s cheese output is also expected to increase, driven by favorable margins relative to other dairy products and steady growth in domestic consumption linked to population growth, reinforcing the region’s expanding contribution to global cheese trade.

3. Strategic Recommendations

Turn Cheese Oversupply into Opportunity Through Market Diversification and Value-Addition Strategies

With EU cheddar prices under pressure from excess inventories and slowing export demand, exporters should reduce exposure to spot-market price volatility by locking buyers into medium-term contracts tied to usage rather than price alone. For example, instead of selling bulk cheddar into Middle East spot markets at discounted prices, EU processors can have medium-term supply contracts with pizza chains, burger brands, and food manufacturers in the Middle East, North Africa, and Southeast Asia, offering stable monthly volumes at formula-based pricing. At the same time, surplus milk should be redirected into aged, specialty, and grated cheese formats, which store longer and command higher margins.

Given the significant YoY price decline and bearish futures curve, US cheesemakers should maximize exports while protecting margins through futures and forward hedging. In parallel, exporters should prioritize high-growth destinations such as Mexico, South Korea, Indonesia, and the Philippines, where US cheddar is already price-competitive and demand for Western-style foods is rising. US suppliers can also bundle cheddar with mozzarella or processed cheese for quick-service restaurant chains, creating multi-product supply contracts that deepen buyer dependence and stabilize volumes.

With New Zealand and Australia increasing cheese output while milk powder demand weakens, Oceania processors should avoid flooding the bulk cheese market and instead push branded and customized cheese products into Asia. For example, New Zealand exporters can target Japan, South Korea, and China with portion-controlled cheddar slices, shredded cheese for pizza chains, and snack-sized packs marketed for convenience and foodservice use. This approach allows exporters to sell cheese at a premium to bulk commodity blocks, reducing vulnerability to global oversupply. Australian producers can leverage domestic consumption growth by expanding private-label supply agreements with major supermarket chains, locking in volumes even if export prices weaken.