In W1 2026, global milk powder markets remained under pressure, with EU WMP and SMP prices showing modest weekly gains but significant YoY declines due to abundant milk supplies and cautious buying. Oceania prices were stable WoW but limited by strong global production and subdued international demand, while South American markets were supported by rising exports to Algeria. Looking ahead, New Zealand WMP exports are expected to remain steady, SMP shipments to rise, EU powder exports to decline as processors favor cheese, and US SMP output to grow amid strong domestic demand. In this environment, exporters are advised to shift from spot sales to medium-term, usage-linked contracts, diversify products, and target application-specific markets in Asia and Latin America to stabilize volumes and protect margins.

1. Weekly Price Overview

Holiday Buying Lifts Milk Powder Prices Briefly Amid Ample Global Supplies

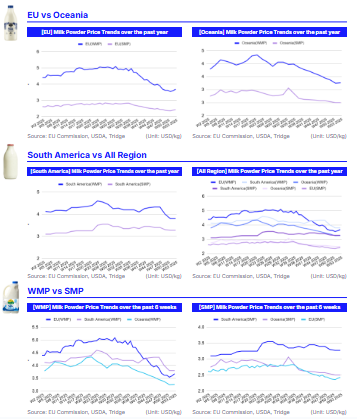

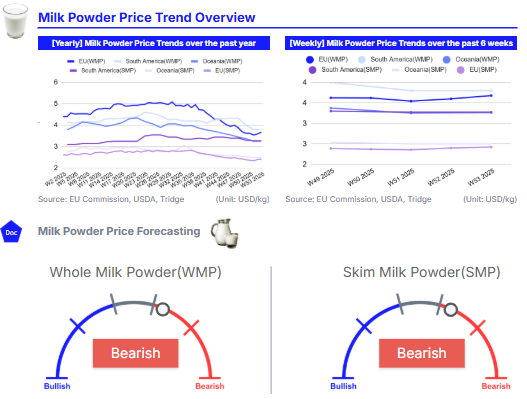

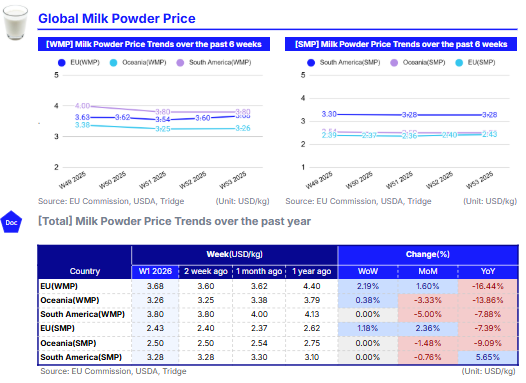

In W1 2026, whole milk powder (WMP) prices in the European Union (EU) averaged USD 3.68 per kilogram (kg), rising 2.19% week-on-week (WoW) and 1.60% month-on-month (MoM), but still standing 16.44% lower year-on-year (YoY). The short-term uptick was largely driven by holiday-related buying as buyers focused on near-term coverage. However, demand remained cautious, with buyers reluctant to extend positions amid abundant milk availability, prompting sellers to trim offers to stay competitive.

In Oceania, WMP prices averaged USD 3.26/kg, up by 0.38% WoW but down 3.33% MoM and 13.86% YoY. While export prices stabilized following recent declines, domestic prices weakened. International demand remained subdued as strong global milk output and elevated WMP production provided buyers with access to competitively priced supplies from alternative origins, limiting upward price momentum.

South American WMP prices averaged USD 3.80/kg, remaining stable WoW but falling 5.00% MoM and 7.88% YoY. Price stability in the short-term was supported by rising export activity, which helped offset increased seasonal production. Argentina and Uruguay recorded higher shipment volumes, with Algeria emerging as the primary destination, aiding market balance.

On the other hand, skim milk powder (SMP) prices in the EU averaged USD 2.43/kg, up 1.18% WoW and 2.36% MoM, but 7.39% lower YoY. The gains were linked to holiday-driven demand, though buyers remained focused on essential coverage and avoided forward commitments. Strong milk intakes continued to boost powder output, leading sellers to adjust offers to manage growing availability.

In Oceania, SMP prices averaged USD 2.50/kg, unchanged WoW but down 1.48% MoM and 9.09% YoY. Export prices held steady after recent declines, while domestic prices softened. Global demand for Oceania-origin SMP remained limited due to ample supplies of lower-priced alternatives from other regions.

Meanwhile, South American SMP prices averaged USD 3.28/kg, unchanged WoW, down 0.76% MoM, but up 5.65% YoY. Price stability was supported by increased exports from Argentina, Uruguay, and Brazil, which coincided with elevated production levels in 2025, even as seasonal milk output eased from its October peak.

2. Price Analysis

Ample Supply and Margin-Driven Production Shifts Reshape Global Milk Powder Trade

In Dec-25, the Food and Agriculture Organization (FAO) global dairy price index averaged 130.31 points, marking a 4.37% MoM drop due to broad-based weakness across major dairy commodities. Within the index, the WMP price index fell by 6.51% MoM to 114.81 points, reflecting peak seasonal milk output in Oceania and subdued purchasing interest from key importing regions. The SMP price index also declined, averaging 95.43 points, down 2.09% MoM, as ample export availability and generally stable market fundamentals weighed on prices.

Looking ahead, the United States Department of Agriculture (USDA) projects that New Zealand’s WMP exports will reach 1.375 million metric tons (mmt) in 2026, broadly unchanged from 2025 estimates. Demand from China is expected to remain stable, as imported WMP continues to be preferred over domestic supplies for certain applications, while shipments to other destinations are forecast to be flat or slightly lower. In contrast, New Zealand’s SMP exports are projected to increase by 4% YoY to 435 thousand metric tons (mt), supported by competitive pricing on the global market.

In the EU, WMP exports are forecast to decline by 9% YoY to 155 thousand mt in 2026, largely due to reduced production as processors continue to prioritize cheese, which offers superior margins. Similarly, EU SMP production is expected to fall by 1% YoY as cheese remains the preferred output over lower-margin products. As a result, EU SMP exports are also projected to edge 1% YoY lower in 2026, following an estimated 6% YoY increase in 2025, with tighter supplies limiting export availability.

Meanwhile, US SMP production is anticipated to rise by more than 5% YoY, supported by higher milk availability and strong domestic demand for protein-rich products. Despite the increase in output, US SMP exports are forecast to decline marginally to 668 thousand mt, reflecting intense global competition. US nonfat dry milk prices are expected to remain above those of the EU and New Zealand, while cooling global demand for SMP is likely to constrain further export growth.

3. Strategic Recommendations

Reposition Milk Powders in an Oversupplied Market with Cautious Buying and Margin Pressure

In the EU, where WMP and SMP face structural oversupply but processors increasingly favor cheese, remaining powder volumes should be placed through usage-linked contracts rather than spot tenders. For example, EU suppliers can secure medium-term supply agreements with food manufacturers producing infant nutrition blends, bakery mixes, or recombined dairy products in North Africa and the Middle East, offering formula-based pricing tied to input costs instead of headline spot prices. This approach stabilizes offtake while reducing exposure to opportunistic buying during weak markets.

In Oceania, where WMP and SMP prices remain under pressure from global competition, exporters should prioritize product differentiation and destination-specific customization over volume expansion. Instead of competing purely on price with EU and South American suppliers, New Zealand processors can target Southeast Asia and China with functional or application-specific powders, such as instantized WMP for beverage use or SMP tailored for bakery and confectionery applications. For instance, offering smaller-bag formats or customized solubility specifications to mid-sized food manufacturers in Indonesia or Vietnam can command modest premiums while deepening customer dependence.

For South America, where exports are already helping absorb rising production, the focus should be on deepening trade relationships in price-sensitive but volume-stable markets. Argentina, Uruguay, and Brazil can build on momentum in Algeria by negotiating longer-term government-to-government or state-linked supply arrangements, reducing reliance on episodic tenders. In addition, South American exporters can expand into nearby Latin American markets by positioning SMP as a cost-effective protein source for recombination and food aid programs, leveraging geographic proximity and lower freight costs to outcompete extra-regional suppliers.