W10 2025: Avocado Weekly Update

In W10 in the avocado landscape, some of the most relevant trends included:

- Heavy rainfall in Colombia has reduced avocado yields, driving up prices, while Florida's industry is struggling with Laurel wilt disease, which has cut production by 50%. These disruptions highlight the vulnerability of avocado supply chains to climate-related challenges.

- The temporary suspension of the US tariff on Mexican avocados has created instability in global trade, forcing Mexico to explore alternative markets in Europe and the Middle East. Meanwhile, concerns over a potential permanent tariff implementation continue to pressure the industry.

- Paraguay’s avocado industry is growing rapidly, supported by favorable conditions and rising global demand. Meanwhile, Peru is capitalizing on avocado industrialization, with avocado oil exports rising steadily and reaching new international markets.

1. Weekly News

Colombia

Hass Avocado Prices Surged by 12% WoW in Central Colombia

Fresh avocado prices in Ibague’s wholesale market rose by 12% week-on-week (WoW) to USD 1.95 per kilogram (kg) in W10, driven by a sharp supply decline from the Tolima Department, a key producing region in Colombia. Persistent heavy rainfall has severely impacted crop yields, reducing harvest volumes and tightening market availability. The ongoing supply shortage is pushing prices higher, straining consumer budgets and highlighting the market’s vulnerability to weather-related disruptions. If adverse conditions persist, prices are likely to rise further.

Mexico

Mexican Avocado Industry Faces Uncertainty Due to Tariff Concerns

Mexico’s avocado industry faces uncertainty as the temporary suspension of a 25% tariff on exports to the United States (US) raises concerns about a potential permanent implementation. The tariff initially disrupted shipments during W10, forcing producers to halt harvesting and renegotiate prices with US buyers due to shrinking profit margins. While exporters explore alternative markets in Europe and the Middle East, logistical challenges persist. Despite favorable production prospects, the risk of continued tariffs could drive price volatility, affecting both exporters and consumers. The industry remains uncertain with the US government set to review the decision in Apr-25.

Paraguay

Paraguay’s Avocado Industry Expands with Strong Growth Potential

Paraguay’s avocado production has grown at an annual rate of 25% over the past three years, reaching around 7.5 thousand metric tons (mt), driven by favorable climatic conditions, fertile soils, and rising global demand. Concentrated in Itapúa, Alto Paraná, and Cordillera, the industry generates approximately USD 13 million annually, with profit margins reaching up to 40% for established producers. Paraguay’s production cycles align with strategic commercial windows, creating opportunities to supply global markets, particularly in Europe and North America. However, challenges such as grower education, financing, and logistics must be addressed to establish a competitive avocado export industry.

Peru

Peru's Avocado Oil Exports See Steady Growth

Peru, the world's second-largest avocado producer and third-largest exporter, saw its avocado oil exports rise by 8.8% in 2024, reaching 1.6 thousand tons. These exports reached seven markets last year, with Spain (35.3%) and Italy (25.2%) as the top destinations. The industrialization of Peruvian avocados has expanded significantly, now reaching 50 markets, while avocado oil exports have grown at an average annual rate of 48.7% over the past six years. This upward trend is expected to continue, bolstering international demand and providing stable market opportunities for producers.

United States

Florida Avocado Industry Fights Laurel Wilt with USD5 Million Research Grant

Florida’s avocado industry is struggling with the devastating Laurel wilt disease, a fungal infection spread by the invasive redbay ambrosia beetle. The disease blocks water flow within trees, causing wilting, leaf drop, and eventual tree death, leading to the loss of over 350 thousand trees and a 50% decline in production. In response, a USD 5 million grant from the United States Department of Agriculture (USDA) will support research on disease control, pest management, and the development of cold-tolerant avocado varieties. Scientists are working to protect existing groves in South Florida while exploring expansion into Central Florida. As the disease spreads beyond the state, these efforts aim to prevent further ecological and economic damage, ensuring the long-term sustainability of avocado production in Florida and other affected regions.

US Tariffs on Mexico Disrupt Global Avocado Market

The US administration’s 25% tariff on Mexican avocado exports is reshaping global trade, prompting Mexico to redirect its 1.3 million-ton annual production toward Europe. This shift, particularly during Europe’s peak avocado season (May–September), could flood the market with 500 thousand to 600 thousand tons, driving prices down to an estimated USD 0.55 to 0.82/kg (EUR 0.50 to 0.75/kg). Kenyan exporters, shipping 70 to 100 thousand tons annually, face increased competition and potential financial strain. Meanwhile, US consumers are likely to see higher prices as the market turns to Chile and Peru for supply. In the long run, the disrupted supply chain could reduce profitability for producers worldwide, ultimately pushing global avocado prices higher.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

Yearly Change in Avocado Pricing Important Exporters (W10 2024 to W10 2025)

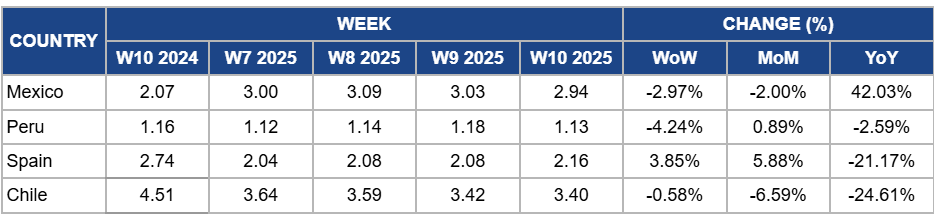

Mexico

Mexico's avocado prices dropped by 2.97% WoW to USD 2.94/kg in W10, with a 2% month-on-month (MoM) decrease due to cautious market behavior amid uncertainty over the recently imposed 25% US tariff on Mexican imports. While a temporary exemption for United States–Mexico–Canada Agreement (USMCA)-compliant products is in place until April 2, 2025, buyers have adopted a wait-and-see approach, leading to price adjustments. However, there is a 42.03% year-on-year (YoY) surge due to tighter supply compared to the previous season, as initial disruptions from the tariff forced producers to delay harvesting and adjust export strategies, limiting availability in key markets.

Peru

Avocado prices in Peru dropped by 4.24% WoW to USD 1.13/kg in W10. The price also recorded a 2.59% YoY decrease. This decline is due to steady export growth in processed avocado products like oil, which has shifted some supply away from the fresh market, easing price pressure. However, avocado prices increased by 0.89% MoM due to tightening availability as the season progresses, alongside stable international demand from key markets like Spain and Italy.

Spain

Spain's avocado prices increased by 3.85% WoW to USD 2.16/kg in W10, with a 5.88% MoM increase due to strong demand across European markets, particularly in France and Germany, where consumption remains high. The ongoing Lamb Hass harvest in the Valencian Community has contributed to stable domestic availability, while improved post-harvest handling and export logistics have supported price resilience. However, avocado prices dropped by 21.17% YoY due to expanded production from maturing orchards, increased output from key suppliers such as Peru and Colombia, and favorable weather conditions that have enhanced yields, leading to a more abundant market supply.

Chile

Chile's avocado prices dropped slightly by 0.58% WoW to USD 3.40/kg in W10, representing a 6.59% MoM decrease and a 24.61% YoY drop due to higher end-of-season supply, increased competition from Peru and Mexico in export markets, and subdued European demand. Additionally, the declining purchasing power in key import destinations has pressured prices, while the local market remains stable but insufficient to offset the broader downward trend.

3. Actionable Recommendations

Diversify Export Markets to Offset Competition

Kenyan avocado exporters should strengthen trade ties with Middle Eastern and Asian markets to mitigate the impact of increased Mexican supply in Europe. Expanding shipments to countries like the United Arab Emirates (UAE), China, and India can help maintain stable prices and demand. Investing in branding and certifications, such as Global Good Agricultural Practices (GAP) and organic labels, can also enhance competitiveness in premium market segments.

Strengthen Supply Chains to Stabilize Prices

Avocado traders in Ibague should establish supply agreements with growers in neighboring regions to mitigate shortages caused by weather disruptions in Tolima. Expanding sourcing to areas with more stable production can help maintain market availability and prevent excessive price spikes. Additionally, investing in cold storage facilities can extend the shelf life of available stock, reducing supply pressure during periods of low harvest.

Sources: Tridge, Agraria, Agronews Castilla Y Leon, EastFruit, Floridatrend, Freshplaza, Fruitnet, Revista Mercados