W16 2025: Olive Oil Weekly Update

.jpg)

In W16 in the olive oil landscape, some of the major trends include:

- Brazil’s removal of a 9% import tariff on EU olive oil is expected to significantly boost European exports, especially from Portugal, Spain, and Italy, as Brazil's domestic demand continues to outpace local production, positioning it as a major global market.

- Spanish olive oil exporters are facing reduced competitiveness in the US due to tariffs, prompting a shift toward alternative markets and raising concerns over the long-term viability of Spain’s olive farming sector.

- Tunisia has consolidated its role as the fourth-largest olive oil exporter, with expanding packaged exports and stable prices, though climate challenges and price volatility pose risks to long-term sustainability.

- US olive oil consumption is projected to surpass Italy’s in 2024/25, driven by health and sustainability awareness, yet tariffs and limited domestic supply may restrict access.

- Italy’s olive oil prices remain high due to structural supply constraints, climate-induced yield reductions, and persistent demand.

1. Weekly News

Brazil

Brazil Lifts Olive Oil Tariffs as Consumption Soars, Boosting EU Export Prospects

The Brazilian government's decision to eliminate a 9% tariff on European Union (EU) olive oil imports has been welcomed by European producers. Aimed at easing household costs amid high food prices, the move reflects Brazil's growing olive oil consumption, averaging 96,800 metric tons (mt) annually over the past five years, a fourfold increase since the early 2000s. Despite rising domestic production, demand still far outpaces local supply. Portugal remains Brazil's top olive oil supplier, followed by Spain and Italy. Analysts expect all major exporters to benefit from increased access, with Brazil projected to become one of the world's largest olive oil markets. The tariff removal also coincides with the conclusion of the Mercosur–EU free trade agreement, though concerns persist among Mercosur producers over competition from lower-priced European oils.

Spain

Spanish Olive Oil Industry Shifts Focus Amid US Tariff Pressures and Export Decline

Spanish olive oil producers are seeking alternative markets in response to United States (US) tariffs that have raised production costs and reduced their competitiveness in one of their key export destinations. As the world’s leading olive oil exporter, Spain has been significantly affected, with small and medium-sized companies halting US shipments due to shrinking profits and market uncertainty. Industry representatives warned that the tariffs threaten the viability of olive farming and could lead to a loss of global market share.

Tunisia

Tunisia Expands Global Olive Oil Reach Despite Price Pressures and New Export Strategy

Tunisia has strengthened its position as the world’s fourth-largest olive oil exporter, capturing 10% of global exports, with growing international recognition for quality and sustainability. In 2024, olive oil exports reached USD 1.60 billion (TND 4.8 billion) across 64 markets, with notable growth in packaged products and strong demand from the EU, North America, and Africa. Despite a 46.3% increase in export volume, revenue declined by 25.8% in the first five months of the 2024/25 campaign due to a sharp price drop. A new national program aims to expand Tunisia’s global market presence through promotional initiatives and international partnerships.

United States

US Olive Oil Leaders Call for Tariff Exemption to Safeguard Public Health and Market Growth

At a recent Olive Oil World Congress event in Washington, DC, industry leaders emphasized the health and sustainability benefits of olive oil while advocating for its exemption from US tariffs. Organized by the North American Olive Oil Association (NAOOA), the event highlighted the rising consumption of extra virgin olive oil in the US—projected to reach 398,000 mt in 2024/25, surpassing Italy. Despite this growth, domestic production remains limited, averaging under 15,000 mt annually. Concerns were raised that current tariffs risk reducing access, particularly for lower-income households, thereby undermining public health gains linked to olive oil use. Organizers stressed the need for policy support to sustain industry growth.

2. Weekly Pricing

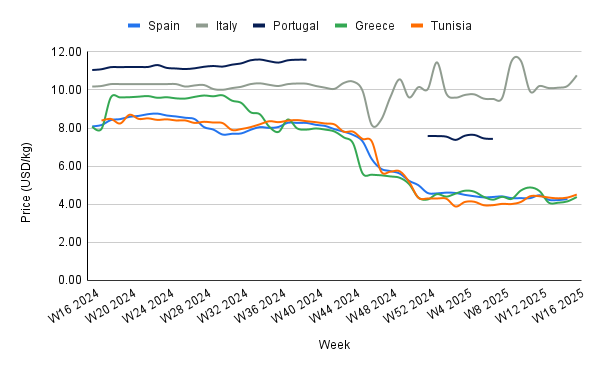

Weekly Olive Oil Pricing Important Exporters (USD/kg)

Yearly Change in Olive Oil Pricing Important Exporters (W16 2024 to W16 2025)

Italy

Italy's olive oil prices rose to USD 10.77 per kilogram (kg) in W16, reflecting a 5.48% increase week-on-week (WoW) and a 5.80% rise year-on-year (YoY), reinforcing the upward pricing trend driven by structural supply limitations. The sharp price differential compared to other major producers highlights ongoing challenges in the Italian sector, where climatic extremes, particularly drought and heat, have severely reduced yields, especially in key regions like Puglia and Sicily.

This supply contraction is exacerbated by the alternate-bearing cycle of olive trees, which naturally limits output in certain years, and by persistent international demand, which continues to absorb reduced volumes at high prices. If adverse weather patterns persist and production does not recover in the next crop year, prices may remain elevated or rise further. Additionally, sustained high prices could shift demand toward lower-cost producers or blends, potentially impacting Italy’s export volumes, though the premium reputation of Italian olive oil may cushion this effect in high-end markets.

Greece

Greece's olive oil prices rose to USD 4.38/kg in W16, up 5.54% WoW, yet down 45.79% YoY from a high of USD 8.08/kg. This sharp annual decline reflects a strong recovery in domestic production following previous drought-affected seasons. Improved yields have alleviated supply constraints, leading to market recalibration and downward price corrections, even as production costs remain elevated.

Despite recent volatility, steady export demand continues to support Greece’s role in the global olive oil trade. The US market plays a key role, accounting for 20 to 30% of Greek olive oil exports directly and indirectly via Italy and Spain. However, the imposition of broad US tariffs on Greek goods, including olive oil, introduces new uncertainty. These trade barriers may dampen future demand, particularly for branded and high-value segments, potentially pressuring prices downward or shifting export strategies toward non-US markets.

Tunisia

In W16, Tunisia's olive oil prices rose to USD 4.51/kg, marking both a WoW and month-on-month (MoM) rise of 3.68% from USD 4.35/kg. This moderate but steady price growth highlights the country's resilient export performance, particularly as European buyers diversify supply sources in response to production instability in traditional markets like Spain and Italy.

Tunisian prices have shown relative stability compared to more volatile markets, underpinned by the country’s growing role as a key global supplier—now ranked fourth worldwide. However, long-term environmental risks, notably water scarcity and persistent soil moisture deficits, threaten production consistency. Without significant investment in climate-resilient practices and modernized irrigation infrastructure, these challenges could tighten supply over time, placing upward pressure on prices and potentially affecting export reliability. Tunisia’s ability to maintain competitive pricing and meet increasing demand will depend on its success in balancing short-term export growth with long-term sustainability measures. The recently launched 2025 National Program to promote olive oil abroad could support price stability by boosting market visibility and fostering higher-value packaged exports, offering some buffer against environmental and market shocks.

3. Actionable Recommendations

Expand Market Share in Brazil Through Targeted Branding and Localized Partnerships

European olive oil exporters, particularly from Portugal, Spain, and Italy, should leverage Brazil’s tariff elimination by expanding exports and investing in localized branding strategies that emphasize authenticity, quality, and health benefits. Establishing partnerships with Brazilian distributors or retailers and adapting products to local consumer preferences (e.g., packaging sizes, and flavor profiles) can enhance market penetration. Promotional campaigns supported by industry groups such as the International Olive Council (IOC) should focus on positioning EU olive oils as premium yet accessible alternatives amid rising Brazilian demand.

Diversify Export Markets and Product Segments to Mitigate Tariff Exposure

Given heightened US tariff risks and price instability, especially for Spanish and Greek producers, exporters should diversify into non-traditional markets such as Brazil, the Gulf Cooperation Council (GCC), and East Asia. These markets offer growing demand and fewer trade barriers. Producers should also consider developing mid-range or blended product lines to capture health-conscious, price-sensitive consumers in emerging economies. Government-backed trade facilitation programs and promotional initiatives can support this diversification strategy.

Sources: Tridge, Oils & Fats International, Olive Oil Times, Bastille Post Global, African Manager