W25 2024: Beef Weekly Update

.jpg)

1. Weekly News

European Union

EU Beef Imports Expected to Grow in 2024 Amid Production Decline

The Agriculture and Horticulture Development Board (AHDB) reports that European Union (EU) beef imports are expected to grow by 2% year-on-year (YoY) in 2024, primarily driven by Brazil. This import increase is contingent on beef exports not being diverted to other key markets such as the United States (US) and China. The import outlook is attributed to a forecasted decrease in EU beef production, which registered a 3.9% YoY drop in 2023 and is projected to decline further by 2.3% YoY in 2024. The AHDB attributes the decrease in 2023 beef production to structural adjustments within the EU beef and dairy sectors. Italy experienced the steepest decline among the leading beef-producing countries, with production plummeting by 17% YoY due to a shortage of imported live animals.

The reduction in beef production has led to price increases, with the European Commission (EC) anticipating that quotations will continue rising in the coming months. Despite the attractive EU prices, beef imports have not fully compensated for the production shortfall. Moreover, the AHDB forecasts that EU beef exports will decline by 1% YoY due to lower cattle inventories. Concurrently, beef consumption in the EU is expected to fall by 2.8% YoY in 2024, following a 4.7% YoY decrease in 2023. This decline in consumption is attributed to high beef prices amid challenging economic conditions, prompting consumers to opt for cost-effective alternatives such as poultry and pork.

Australia

China Reopens Market to Australian Beef After 2020 Restrictions

The recent lifting of trade barriers imposed by China in 2020 on beef exports from five major Australian producers signifies a notable improvement in trade relations between the two countries. This development paves the way for a greater presence of Australian meat in the Chinese market, presenting new opportunities for Australian farmers and exporters. It also marks a crucial step toward normalizing bilateral relations after years of tension. It is worth noting that the trade restriction, seen as part of a broader trade conflict, emerged amid diplomatic tensions when Canberra called for an independent investigation into the origin of COVID-19.

Australian beef exporters have intensified their marketing efforts, using promotional platforms like the SIAL Shanghai 2024 expo held in May-24, where approximately 40 Australian exporters were showcased. Australian products are also anticipated to be featured at the China International Import Expo (CIIE) in Nov-24.

Despite the optimism, Australian beef exporters are expected to face several challenges as they strive to capitalize on this opportunity fully. The Chinese market is highly competitive, with major exporters such as Brazil and the US battling for market share. Additionally, Australian exporters must comply with stringent Chinese regulations and quality standards to prevent future setbacks. Fortunately, Australia's reputation as a supplier of high-quality beef, combined with Chinese consumers' growing preference for premium products, presents a significant opportunity.

China

China Implements New Regulations to Stabilize Beef Cattle Industry

China published new regulations to stabilize beef cattle production on June 21, 2024, as the industry grapples with price drops and significant losses. As the world's largest meat consumer, China has seen an increase in beef production over the last decade, driven by a growing middle class, which has spurred the expansion of farms. According to Reuters, China's cow slaughter reached 50.2 million heads in 2023, a 19% increase compared to 2014.

However, recent years have seen a decline in beef consumption due to the economic slowdown, leading to market oversupply and lower prices. In response, the Chinese government has advised farms to adjust breeding practices, cull old and low-performing livestock, optimize herd structure, and improve efficiency. China's Ministry of Agriculture also indicated that major producing areas should seek support from financial institutions. To prevent diseases, the ministry indicated that it would support large-scale farms in enhancing biosecurity measures and establishing disease-free communities.

2. Weekly Pricing

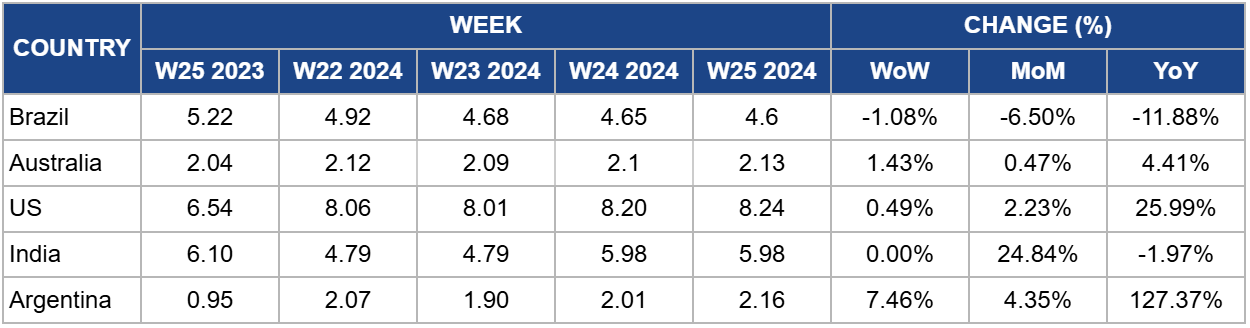

Weekly Beef Pricing Important Exporters (USD/kg)

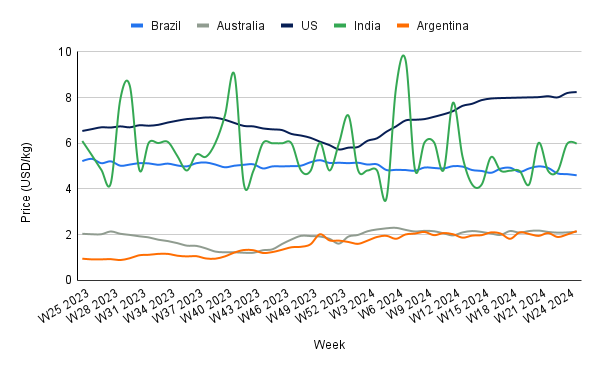

Yearly Change in Beef Pricing Important Exporters (W25 2023 to W25 2024)

Brazil

In W25, the wholesale price of boneless rear beef in Brazil averaged USD 4.60 per kilogram (kg). This marks a 1.08% week-on-week (WoW) drop, a 6.50% month-on-month (MoM) decrease, and a 11.88% YoY decline. The price in Brazilian real (BRL) remained steady at BRL 25.00/kg, indicating that the WoW drop in USD is due to the devaluation of the real against the US dollar. However, the YoY decline is primarily due to a high beef supply in the Brazilian market resulting from increased production. The Center for Advanced Studies on Applied Economics (CEPEA) reports that approximately 613.54 thousand metric tons (mt) of meat were available at national wholesale in May-24, an increase of 11.6% compared to Apr-24. CEPEA also indicates that domestic beef availability reached 2.972 million metric tons (mmt) from Jan-24 to May-24, the highest volume since 2018. This surge is attributed to lower cattle prices in 2024, reflecting a demand that has not kept up with the increase in supply.

Australia

Australia's national young cattle indicator averaged USD 2.13/kg in W25. This indicates a 1.43% WoW increase, and a 0.47% MoM rise. This price increase can be attributed to a drop in supply at various saleyards. The Meat and Livestock Australia (MLA) reports that yardings decreased by approximately 7.35 thousand heads, falling to 53.66 thousand heads over the week. This decline occurred despite the longer trading week in some states due to the King's Birthday long weekend. MLA highlights that the reduction was mainly driven by a 9.97 thousand heads drop in Queensland yardings, which fell to 15.47 thousand heads. Notably, yardings were smaller in every Queensland sale except Dalby.

United States

The average price of lean beef (92% to 94%) in the US reached USD 8.24/kg in W25, a 0.49% WoW increase, and a substantial 25.99% YoY rise. These price hikes are attributed to a reduced beef supply in the market, resulting from a decrease in US beef production due to prolonged droughts. The United States Department of Agriculture (USDA) reports that as of June 1, 2024, the total US cattle and calves on feed amounted to 11.6 million heads, slightly below last year’s inventory. The USDA indicates that these numbers suggest a stronger decline in placements later in the year, potentially pushing prices even higher.

India

In W25, the average price of beef (cow) in India was USD 5.98/kg, a 1.97% YoY decline. However, this price represents a significant 25.10% MoM increase, highlighting the volatility of the Indian beef market, which has been pronounced over the past year. This volatility is mainly driven by fluctuations resulting from both domestic and international regulations.

Argentina

In W25, the average price of beef (steer) in Argentina reached USD 2.16/kg, a 7.46% WoW increase, and a 4.35% MoM rise. These price hikes could be due to a rebound in demand during the holidays celebrated over the week. Despite this, beef consumption has remained low in recent months due to the challenging economic environment, causing many consumers to opt for more cost-effective options like poultry. The Chamber of Industry and Commerce of Meats and Derivatives of the Argentine Republic (CICCRA) reports that domestic beef consumption is at its lowest level in the last 30 years. This decline is attributed to the economic crisis, which has significantly eroded the purchasing power of Argentines. In the first half of 2024 alone, purchasing power dropped by approximately 13% YoY, negatively impacting access to various basic basket products.

3. Actionable Recommendations

Enhancing Trade Partnerships and Diversifying Import Sources

To address the anticipated increase in EU beef imports, the EU should strengthen trade agreements with key beef-exporting countries like Brazil. By negotiating favorable terms and reducing trade barriers, the EU can ensure a stable and diverse beef supply, mitigating the risks associated with relying on a single source. This approach will help stabilize prices and provide more options for EU consumers.

Supporting Domestic Beef Producers

To mitigate the impact of declining domestic beef production, the EU should support domestic beef producers through subsidies, low-interest loans, and grants. This financial support can help farmers invest in advanced farming technologies, improve productivity, and sustain their operations despite the challenging economic conditions.

Additionally, the EU should collaborate with financial institutions to provide tailored financial products and services to beef producers amid the challenging economic conditions. These could include low-interest loans, credit facilities, and insurance products designed to help farmers manage risks and invest in necessary infrastructure improvements.

Complying with Regulations and Quality Standards and Developing Brand Identity

Compliance with Chinese import regulations and quality standards is paramount for Australian exporters. To prevent future trade setbacks, exporters must regularly update and audit their supply chains to meet regulatory requirements. Investing in quality control measures and certifications that align with Chinese standards, along with training staff on compliance protocols and regulatory changes, will ensure that Australian beef maintains its reputation for safety and quality.

Australian beef producers should leverage their reputation for high-quality beef by developing a strong brand identity that highlights the premium quality, safety, and sustainability of their products. Utilizing geographical indicators and certification labels will help distinguish Australian beef in the market. Launching targeted marketing campaigns that resonate with Chinese consumers’ growing preference for premium products can further enhance market presence.

Sources: Agromeat, Agro Valor, AHDB, CEPEA, Reuters