W26 2025: Wheat Weekly Update

In W26 in the wheat landscape, some of the most relevant trends included:

- EU winter wheat development remains stable with favorable yield prospects in Spain, Romania, Bulgaria, Greece, and the Baltic states. However, localized weather issues, pest pressure, and early heatwaves raise concerns in parts of France, Germany, Italy, and Poland.

- Severe drought and heat in Eastern Ukraine, Türkiye, Cyprus, and the Western Maghreb have caused irreversible crop losses, significantly lowering expected yields.

- Afghanistan seeks to expand direct wheat imports from Russia amid supply disruptions from Iran, aiming to close a production gap despite a 10% increase in domestic output.

- Wheat planting in Argentina is 70% complete. Excess rainfall has delayed sowing and reduced the projected planted area. While improved soil moisture supports yield potential, climate risks and seed shortages continue to create uncertainty.

- Russia's total wheat area is declining as farmers shift to more profitable crops. Spring sowing is down by up to 5.7% YoY. Yields may remain stable, but moisture deficits and frost risks continue to pose challenges. Exports dropped sharply in Jun-25 but are projected to recover in Jul-25.

- In the US, spring wheat crop conditions deteriorated, and winter wheat harvesting remained behind the seasonal average. Wheat prices fell 7.41% WoW due to easing geopolitical tensions and mixed weather impacts.

1. Weekly News

European Union

EU Winter Wheat Outlook Remains Stable, with Regional Weather Risks

Winter crop development across the European Union (EU) remains stable with favorable yield prospects, particularly in Spain, Portugal, Romania, Bulgaria, Greece, and the Baltic states, according to the European Commission's (EC) Joint Research Centre (JRC) Monitoring Agricultural Resources (MARS) bulletin. Favorable spring rainfall supported biomass accumulation, though increased pest pressure and a brief heatwave in early Jun-25 posed risks.

Localized concerns persist in western Belgium, central France, eastern Germany, western Poland, and Hungary, where adverse weather may limit yields. Northern Italy faces potential yield losses due to excessive rainfall. Moreover, pest outbreaks are threatening crops in parts of Germany. In contrast, soft wheat yields in Italy could reach 5.14 metric tons (mt) per hectare (ha).

Severe drought and heat in Eastern Ukraine, Türkiye, Cyprus, and the Western Maghreb have led to irreversible crop losses, with MARS forecasting significant winter wheat yield declines in these regions.

Afghanistan

Afghanistan Seeks More Direct Wheat Imports from Russia Due to Regional Supply Risks

Amid potential supply disruptions from Iran due to the Israel-Iran conflict, Afghanistan is in talks with Russia to increase direct wheat imports, according to the Minister of Agriculture, Irrigation, and Livestock of Afghanistan. Although striving for agricultural self-sufficiency, Afghanistan remains reliant on key food imports, particularly from Iran and Russia.

Afghanistan currently imports wheat and flour from Russia and Kazakhstan, but is now seeking to prioritize wheat over flour shipments. In 2024, Afghanistan was Russia's top flour buyer. Despite increasing domestic wheat output by 10% to 4.83 million metric tons (mmt), the figure is still short of the annual demand of 6.8 mmt. Recent diplomatic engagements, including Afghanistan's participation in Russia's economic forum, signal deepening trade relations, with wheat supply stability emerging as a priority for Kabul amid regional geopolitical risks.

Argentina

Mixed Outlook for Argentina's 2025 Wheat Campaign as Weather Disruptions Offset Improved Soil Moisture

As of W26, wheat planting in Argentina's core region is 70% complete, but uneven progress and weather disruptions are altering initial expectations. The Rosario Stock Exchange (BCR) reports that excessive rainfall in northeastern Buenos Aires has delayed sowing and logistics, reducing the projected area by 50,000 ha, from 1.66 to 1.61 million ha. In contrast, western areas such as Corral de Bustos show strong progress, reaching 90% completion with optimal moisture and stable yield prospects of 40 to 42 quintal per ha.

Persistent rains have delayed planting of long-cycle varieties beyond their optimal window, increasing climate risks and leading to concerns over seed availability for shorter cycles. Nonetheless, water reserves across 70% of the region are significantly improved compared to 2024, with autumn rainfall 30% higher on average. However, additional challenges remain, including difficulties managing late-season and rising pest risks due to excess moisture. The 2025 wheat campaign faces a mixed outlook, buoyed by better soil moisture, but constrained by logistical setbacks and crop management uncertainties.

Egypt

Egypt Expands Wheat Imports from Europe to Bolster Reserves and Reduce Supply Risks

Egypt, one of the world's largest wheat importers, is set to receive shipments from France and other European countries in the coming weeks as part of efforts to strengthen strategic reserves and diversify suppliers amid rising geopolitical risks and Black Sea trade volatility. The state grain buyer, Egypt's Future Authority for Sustainable Development, is finalizing a schedule of delayed imports through year-end and confirmed that loading at France's La Pallice port will start on July 5, with additional vessels to follow.

The agency is shifting toward direct procurement from European suppliers, aiming to streamline logistics and reduce reliance on intermediaries. Talks are underway with several EU countries for large-volume deliveries. Egypt's current wheat reserves reportedly cover more than six months of national consumption, supporting its broader food security strategy.

Russia

Russia's Wheat Acreage Hits Decade Low Due to Profitability Concerns and Crop Shift, Despite Stable Harvest Outlook

Russia's spring wheat acreage is projected to decline by up to 5.7% year-on-year (YoY), potentially reaching the lowest level in over a decade, amid unfavorable weather and a shift toward more profitable crops such as oilseeds and legumes. As of June 11, 2025, sowing covered 11.1 million ha, 10.5% less YoY, with the steepest declines seen in Siberia and the Urals. Winter wheat area also fell by 6.8% to 15.1 million ha, with total wheat sowing forecast at 27 to 28 million ha, down from 28.5 million ha.

This shift reflects declining profitability, with current wheat prices at USD 152.04 to 177.38/mt (RUB 12,000 to 14,000/mt) are near breakeven, while production costs have surged 20% annually. In contrast, oilseeds and pulses yield significantly higher margins, drawing farmers' interest. Despite the acreage drop, yield optimism keeps harvest projections stable. Analysts forecast a wheat crop of 82.8 mmt, slightly above last year’s 82.6 mmt, driven by improved yields. However, moisture deficits, spring frosts, and drought-related emergencies in southern regions pose downside risks.

Russian Wheat Exports Drop Sharply in Jun-25, but Rebound Expected in Jul-25 on New Harvest

Russian wheat exports for Jun-25 are estimated at 1.2 to 1.25 mmt, marking a sharp decline from 1.9 mmt in May-25 and 2.4 mmt in Apr-25, according to forecasts from Russian agricultural consultancy Sovecon and the Russian Agricultural Transport Company (Rusagrotrans). These volumes are unusually low for Russia, which is a leading global wheat exporter. However, Rusagrotrans anticipates a strong rebound in Jul-25, projecting exports to rise to 3.6 to 4 mmt, supported by the new harvest and seasonal export patterns.

Türkiye

Wheat Harvest Begins in Türkiye's Hayrabolu District with Promising Early Yields

The wheat harvest has officially begun in Hayrabolu, a key agricultural district in Tekirdağ, Türkiye. Following the planting of approximately 354,000 acres, early harvesting has commenced, with yields ranging between 250 and 520 kilograms (kg) per decare. The Chairman of the Hayrabolu Önder Farmer Consultancy Association noted that harvesting is progressing steadily and is expected to accelerate in the coming days. He emphasized the economic and strategic importance of wheat for local farmers and expressed optimism for a productive and prosperous season.

United States

USDA Reports Decline in US Spring Wheat Crop Conditions and Below-Average Winter Wheat Harvest Progress in W25

In W25, the condition of United States (US) spring wheat crops declined, with those rated good to excellent dropping from 57% to 54%, compared to 71% a year ago, according to the United States Department of Agriculture's (USDA) National Agricultural Statistical Service (NASS). Winter wheat harvesting remains below average, with only 19% completed by Jun-22, against 38% last year and a five-year average of 28%.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W26 2024 to W26 2025)

.png)

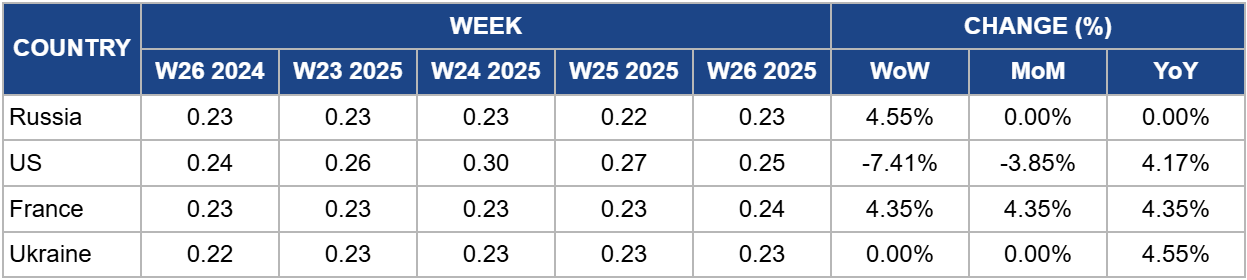

Russia

In W26, Russia's wheat prices rose by 4.55% week-on-week (WoW) to USD 0.23/kg, matching the same level as in 2024. The increase follows a USD 5/mt rise in FOB bid prices for 12.5% protein wheat for Jul-25 delivery, reaching USD 226–227/mt, reflecting improved demand and weather-related supply risks. Correspondingly, domestic bid prices in deep-sea ports climbed by USD 3.17/mt (RUB 250/mt) to USD 183.72/mt (RUB 14,500/mt), excluding value-added tax (VAT).

This price rebound follows a previous dip and is supported by rising benchmark prices in competing origins. Analysts cite wet weather in southern Russia as a contributing factor. While precipitation in the Rostov and Krasnodar regions may ease drought conditions slightly, quality concerns persist due to early harvest and rain-related risks such as sprouting and lower grain quality.

United States

In W26, US wheat prices fell by 7.41% WoW to USD 0.25/kg, experiencing a month-on-month (MoM) decline of 3.85% from USD 0.26/kg. The recent drop follows the easing of geopolitical tensions surrounding potential US involvement in the Israel-Iran conflict, which had previously fueled price gains through short-covering activity. As uncertainty eased, less speculative buying contributed to the downward movement.

Additionally, mixed crop conditions added volatility to the market. While excessive rainfall in the US Great Plains raised quality concerns, it also improved yield prospects in some areas, tempering bullish sentiment. This recent price softening may limit upward momentum in the near term unless weather risks intensify or export demand strengthens. Continued monitoring of harvest outcomes and global supply competition, particularly from the Black Sea region, will be critical in shaping future price direction.

France

France's wheat prices rose by 4.35% WoW to USD 0.24/kg in W26, reflecting steady gains across monthly and annual comparisons. The price increase aligns with the start of the 2025 harvest season, as the National Establishment for Agricultural and Sea Products (FranceAgriMer) reported initial winter wheat threshing at 1% of planted area, on par with the five-year average. Meanwhile, favorable crop development and early harvest activity for winter barley (22% harvested) suggest stable supply prospects.

While the current price strength is supported by early harvest momentum and firm demand, future pricing will depend on yield outcomes amid localized weather risks. If weather remains favorable and harvesting accelerates without disruption, supply expansion could moderate price growth in the coming weeks. However, any yield variability or quality concerns, particularly with durum wheat and later-stage crops, may sustain upward price pressure.

Ukraine

In W26, Ukraine's wheat prices remained steady at USD 0.23/kg, unchanged from the previous week and month but up 4.55% YoY from USD 0.22/kg. This stability follows earlier price declines in Jun-25 and is now supported by a stronger US dollar and recent importer tenders in which Ukrainian wheat was sold.

Despite stable prices, Ukraine's wheat market may face downward pressure due to lower harvest expectations and export constraints. Ukraine's Agro-Security Analytical Platform for Agriculture (ASAP Agri) forecasts a 3% production drop to 21.74 mmt and exports at 15 mmt, limited by renewed EU import quotas and competition from Russian wheat. Harvesting is expected to intensify in late June, which could cap short-term price gains, though delays in EU trade talks or Black Sea disruptions may provide support.

3. Actionable Recommendations

Enhance Pest and Weather Risk Management in the EU

European wheat producers should intensify integrated pest management and implement adaptive strategies to mitigate the risks posed by localized pest outbreaks, heatwaves, and excess rainfall. Investing in crop monitoring technologies and timely intervention will help stabilize yields across vulnerable regions such as France, Germany, Italy, and Poland.

Diversify and Secure Wheat Supply Chains for Import-Dependent Countries

Countries like Afghanistan and Egypt should prioritize diversifying wheat import sources and strengthen direct procurement agreements, particularly with stable suppliers such as Russia and EU member states. This approach will help mitigate supply disruptions arising from geopolitical conflicts and enhance food security through improved logistical efficiency.

Support the Argentine Wheat Sector to Manage Planting and Climate Risks

Stakeholders in Argentina should focus on improving sowing logistics and seed availability to address delays caused by excessive rainfall. Additionally, promoting resilient wheat varieties and investing in pest management will be crucial to optimize yield potential amid climatic uncertainties and ensure a stable 2025 campaign despite uneven planting progress.

Sources: Tridge, Oil World, Hellenic Shipping News, Ukr AgroConsult, Revista Chacra, Kamu3, Agro Investor, Agri