W3 2025: Wheat Weekly Update

.jpg)

In W3 in the wheat landscape, some of the most relevant trends included:

- Global wheat production for the 2024/25 season is projected to increase to 793.24 mmt, while exports are forecasted to decline to 212 mmt. Ending stocks are expected to rise to 258.82 mmt.

- Ukrainian wheat harvest remains steady at 22.9 mmt, but export forecasts have been reduced to 16 mmt due to logistical and drought-related challenges. Operational data show a delay in winter wheat sowing.

- Russia’s wheat export forecast has been lowered to 46 mmt, reflecting a reduction due to drought and government export restrictions. Wheat production for 2024/25 is now estimated at 83 mmt.

- Ukrainian wheat prices rose WoW and YoY, while French wheat prices declined WoW and MoM despite lower production forecasts.

1. Weekly News

Global

Global Wheat Production Projected to Increase, Exports Decline

The United States Department of Agriculture (USDA) Jan-25 report projects global wheat production for the 2024/25 season to slightly increase to 793.24 million metric tons (mmt). The export forecast has been reduced to 212 mmt and ending stocks are expected to rise to 258.82 mmt. Ukraine's wheat harvest remains steady at 22.9 mmt, but its export forecast has been reduced to 16 mmt. Wheat production and export estimates remain unchanged in the United States (US). Meanwhile, China is expected to see a minor increase in wheat production, alongside a decline in imports and ending stocks, reflecting adjustments in domestic policies and demand.

Egypt

Egypt’s Wheat Imports Reached 10-Year High at 14.2 MMT in 2024

Egypt's wheat imports soared to a 10-year high of 14.2 mmt in 2024, up from 10.8 mmt in 2023. This sharp increase was due to improved dollar availability and a drop in global wheat prices, which fell to an average of USD 240 per metric ton (mt) compared to USD 350/mt in 2023. The Egyptian government's share of wheat imports rose significantly by 30%, reaching 6.2 mmt.

India

Climate Change Threatens India's Agricultural Sustainability

India's agricultural sector is under significant threat from climate change, with projections indicating a decline in rice and wheat production. Wheat output could drop by 6 to 25% by 2100. These reductions pose risks to food security since India contributes approximately 14% of the global production, and the nation relies heavily on subsidized grains. Climate change also disrupts fisheries, with warmer sea temperatures driving fish away from coastal areas, adversely affecting fishing communities. Furthermore, the decreasing frequency and intensity of Mediterranean weather systems, crucial for winter precipitation in Northwest India, exacerbate concerns about water shortages, threatening agricultural sustainability and livelihoods.

Kazakhstan

USDA Maintains Kazakhstan's 2024/25 Wheat Export Forecast at 10 MMT

The USDA maintained its forecast for Kazakhstan's wheat exports at 10 mmt for the 2024/25 season. This figure remains unchanged from the Dec- forecast. The USDA also kept its projection for wheat imports steady at 500 thousand mt. Similarly, the wheat production estimate for the 2024/25 season remains unchanged at 18 mmt, consistent with the Dec-24 forecast.

Russia

USDA Lowers Russia’s Wheat Export Forecast for 2024/25 to 46 MMT

The USDA has reduced its forecast for Russia's wheat exports in the 2024/25 season by 1 mmt to 46 mmt, excluding Crimea and newly added regions. This follows a similar downward revision in Dec-24. Meanwhile, the export forecast for the European Union (EU), Russia's closest competitor, remains unchanged at 29 mmt. The estimate for Russian feed grain exports slightly increased from 6.2 mmt to 6.23 mmt. According to the USDA, Russia, the world's largest wheat exporter, has announced its grain export quota for the second half of 2024/25 will be the lowest in five years, likely affecting its overall export capacity.

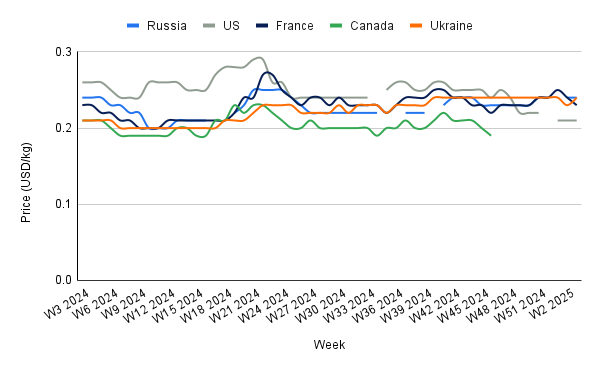

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W3 2024 to W3 2025)

Russia

In W3, Russian wheat prices remained steady week-on-week (WoW) at USD 0.24 per kilogram (kg). However, concerns over a potential decrease in wheat supply from Russia persist due to unfavorable weather conditions impacting early wheat growth, including droughts that have lowered production forecasts. The USDA now estimates Russian wheat production for the 2024/25 marketing year (MY) at 83 mmt, reflecting a downward revision. Moreover, the Russian government's export restrictions to stabilize domestic food prices and ensure sufficient local supply have further constrained the volume of wheat available for export, contributing to a tightening global wheat market.

United States

In W3, US wheat prices stood at USD 0.21/kg, marking a 19.23% year-on-year (YoY) decline. The price drop is due to expectations of record global wheat supplies and the strong US dollar, which has pressured prices downward. The USDA projects an 11% YoY increase in the US wheat crop for 2025, reaching approximately 2 billion bushels. This anticipated surplus has further weighed on prices. Moreover, the strong US dollar has made US wheat exports less competitive, potentially dampening demand from key importers such as the Philippines, Mexico, and Japan.

France

In W3, French wheat prices declined by 4.17% WoW and month-on-month (MoM), reaching USD 0.23/kg. This price drop occurred despite lower production forecasts for the 2024/25 MY. The French Ministry of Agriculture revised its soft wheat production estimate downward to 25.78 mmt, representing a 540 thousand mt drop from earlier projections. This adjustment reflects a 17% decrease in planted acreage and a 15% decline in yields compared to the 2023/24 season.

Ukraine

In W3, Ukrainian wheat prices rose by 4.35% WoW and 14.29% YoY to USD 0.24/kg. Despite the wheat harvest forecast remaining unchanged at 22.9 mmt, the export forecast was revised downward to 16 mmt. Moreover, operational data indicate that as of early Dec-24, 4.38 million hectares (ha) of winter wheat had been sown, nearly 2% below the planned area and 9% YoY less. This lag in winter crop sowing is due to ongoing drought challenges.

3. Actionable Recommendations

Develop Climate-Resilient Wheat Varieties in Vulnerable Regions

As climate change threatens wheat production in regions like India and Ukraine, breeding and promoting drought-resistant wheat varieties can help farmers maintain productivity. Collaborate with agricultural research institutes to develop and distribute heat-tolerant and drought-resistant wheat varieties, such as HLWG-73 in India and Madduma in Ukraine. This enhances resilience to extreme weather events, improving long-term food security and yield stability, even during fluctuating weather patterns.

Diversify Export Markets Beyond Traditional Buyers

With the projected surplus in wheat production globally, countries like the US, and Russia should focus on expanding exports to new or underdeveloped markets where demand is growing. Engage in trade negotiations with emerging economies in Southeast Asia, Africa, and Latin America to introduce value-added wheat products such as flour blends and packaged goods. This opens up new revenue streams and mitigates dependency on traditional buyers, ensuring a more stable export base.

Enhance Storage and Post-Harvest Handling in Exporting Countries

Given the projected decline in global wheat exports, particularly from key suppliers like Russia and Ukraine, improving post-harvest handling and storage infrastructure can significantly reduce losses and ensure higher quality for export. This includes implementing modern grain storage techniques such as temperature-controlled silos and air-tight bins to preserve wheat quality over extended periods. Therefore, it will prevent quality deterioration and reduce wastage during transit and storage, ensuring a more consistent supply for international buyers.

Sources: Tridge, Agro Investor, UkrAgroConsult