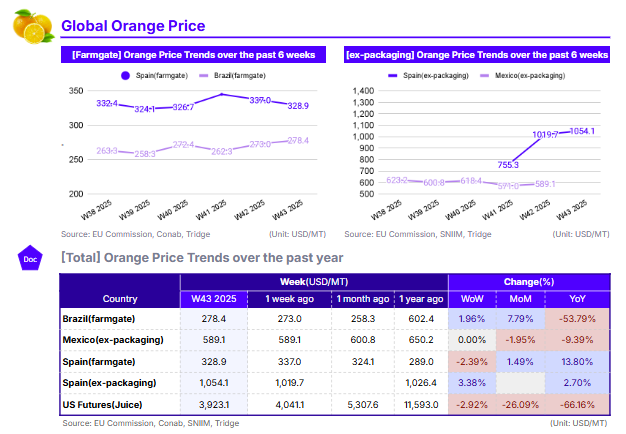

W43 2025: Orange

In W43 2025, global orange prices were mixed. Brazil's farmgate price rose 1.96% WoW to USD 278.4/mt based on increased exports to the US, while Spain's farmgate price fell 2.39% WoW to USD 328.9/mt due to rising seasonal supply and high volumes of South African oranges still on the European market. US Futures also continued to slide (-2.92% WoW), largely due to increased imports of orange juice from Brazil. Long-term trends show a major market correction, with US Futures (-66.16%) and Brazilian prices (-53.79%) collapsing YoY due to improved supply in the Americas. Spain remains the exception, with farmgate prices up 13.80% YoY, supported by forecasts of a 16-year low harvest. Given its significant harvest recovery and competitive pricing compared to Mexico, Brazil presents a prime sourcing opportunity for buyers in the Americas. Suppliers worth considering in Brazil include NCD Brazil, GBG, and Soeli Desouza Ferris.

1. Weekly Price Overview

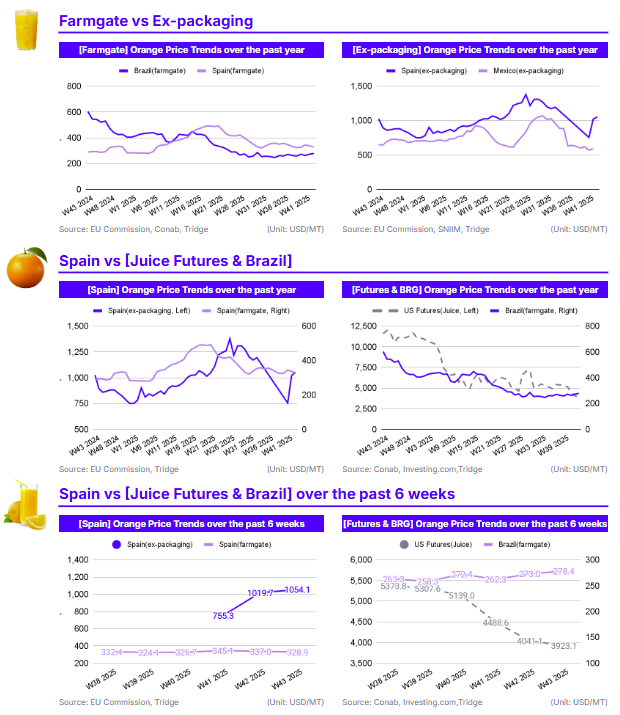

Prices in Brazil Move Upward While Prices in Spain and the US Face Downward Pressure

In Brazil, the farmgate price for oranges was USD 278.4/metric ton (mt) in W43, rising 1.96% week-on-week (WoW). Mexico’s ex-packaging price was flat (0.00% WoW) at USD 589.1/mt. In Spain, the farmgate price fell 2.39% WoW to USD 328.9/mt while US Orange Juice Futures continued to fall, dropping 2.92% WoW to USD 3,923.1/mt.

The week's movements reflect opposing supply pressures. The 2.39% WoW dip in Spain’s farmgate price is likely a result of increasing seasonal supply. The country is moving past its tough start for early varieties, and harvest volumes are beginning to ramp up. This, combined with significant volumes of Southern Hemisphere oranges (like those from South Africa) still present in the European market, is placing temporary bearish pressure on prices. In contrast, the US Futures price drop (-2.92% WoW) is driven by abundant supply in North America. This is a reaction to both a domestic US production forecast that is up year-on-year (YoY) and a reported surge in orange juice imports from Brazil, which is weighing heavily on the futures market. Increased exports to the US is also likely the cause of the uptick in Brazilian orange prices.

2. Price Analysis

Supply Fundamentals Is The Primary Driver of Medium and Long Term Price Trends

US Orange Juice Futures prices fell 26.09% month-on-month (MoM), highlighting a massive 66.16% YoY collapse. Brazil’s farmgate price showed a recent 7.79% MoM recovery but remained down 53.79% YoY. Mexico’s ex-packaging price also remained bearish long-term, down 1.95% MoM and 9.39% YoY. Spain was the only market showing long-term strength, with its farmgate price increasing 1.49% MoM and 13.80% YoY.

The dramatic YoY declines in US Futures (-66.16%) and Brazil (-53.79%) reflect a major market correction from the price crisis peaks of 2024. This bearish trend is supported by improved supply fundamentals in the Americas. US domestic production is forecast to be higher YoY, and this is compounded by a significant increase in orange juice imports from Brazil, which has shifted volumes to the US to compensate for weaker demand in Europe. The production recovery in Brazil is compounding the downward price pressure on orange prices in both North and South America.

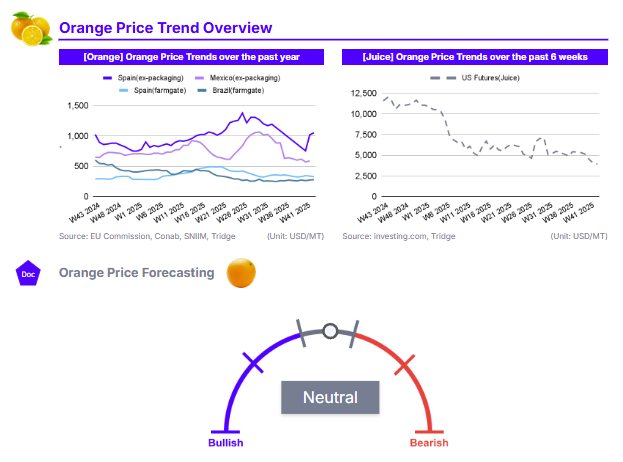

In sharp contrast, Spain’s 13.80% YoY farmgate price increase highlights its persistent, localized supply crisis. Despite recent seasonal pressure, the market is still pricing in the dire 2025/26 forecast, which predicts Spain's citrus production will hit a 16-year low. The outlook remains bearish for juice futures as slowing global demand meets recovering supply in the Americas. The situation is the same for Brazilian and Mexican orange prices. However, Spanish fresh orange prices are expected to remain firm and will likely rise as the limited 2025/26 harvest fails to meet regional demand.

3. Strategic Recommendations

Target Brazil for Americas Sourcing to Capitalize on Low Prices and Volume Recovery

Global buyers, particularly importers and juice processors based in North and South America, should prioritize sourcing from Brazil to leverage its current market-leading prices and recovered harvest volumes. In W43, Brazil's farmgate price of USD 278.4/mt is the most competitive among major producing countries, trading at a steep discount to its regional competitor, Mexico (USD 589.1/mt), and remaining well below Spanish farmgate prices (USD 328.9/mt). This affordability is underscored by a 53.79% YoY price collapse, signaling a significant market correction from 2024 highs.

This low pricing is supported by a substantial recovery in Brazil's 2025/26 harvest volume compared to the previous season's multi-decade low. This improved supply, combined with weaker demand from Europe, has prompted Brazilian exporters to increase shipments to the US. For buyers in the Americas, this creates a prime opportunity to secure large volumes at a significant cost advantage, reducing reliance on the higher-priced Mexican market. According to Tridge Eye data, suppliers worth considering in Brazil include NCD Brazil, GBG, and Soeli Desouza Ferris.