In W41, global milk powder markets reflected a bearish tone as prices declined across major exporting regions except South America. EU WMP and SMP prices fell due to weak regional demand and subdued export activity, while Oceania also recorded declines driven by strong production ahead of the spring flush. In contrast, South America saw price gains supported by steady demand and rising export activity, particularly from Argentina. With global milk output remaining high and inventories gradually building, market conditions continue to pressure EU and Oceania exporters, prompting the need for strategic responses such as targeting emerging markets, adopting flexible pricing strategies, and diversifying into higher-value dairy derivatives to maintain competitiveness.

Milk Powder Price Forecasting

1. Weekly Price Overview

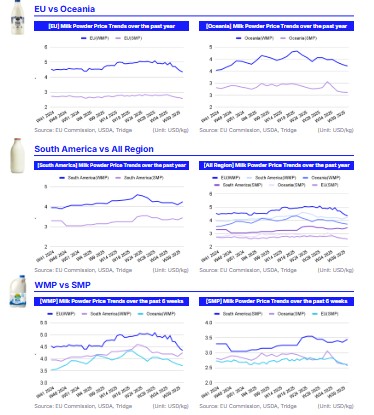

EU and Oceania Face Price Pressure While South America Sees Gains

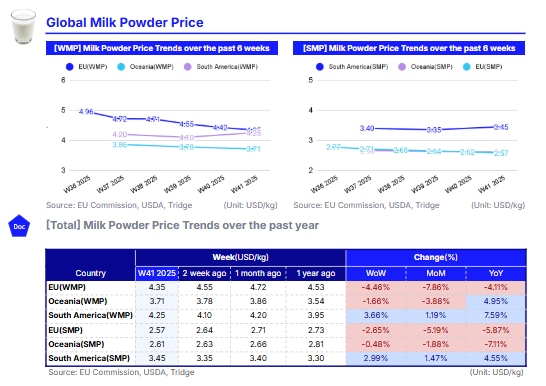

In W41, European Union (EU) whole milk powder (WMP) prices averaged USD 4.35 per kilogram (kg), a 4.46% week-on-week (WoW) decline. This drop was likely driven by weaker regional and international demand, as competitive global pricing continues to pressure EU sales. A similar trend is observed in the EU skimmed milk powder (SMP) market, where prices declined 2.65% WoW to USD 2.57/kg. The decrease is attributed to sluggish domestic demand and subdued export interest. In Oceania, WMP prices slipped 1.66% WoW to USD 3.71/kg, likely due to strong production ahead of the spring flush, leading to excess supply. Meanwhile, Oceania SMP prices edged down 0.48% WoW to USD 2.61/kg due to peaking milk output in the region.

On the contrary, South America recorded price gains, with WMP increasing 3.66% WoW to USD 4.25/kg, while SMP rising 2.99% WoW to USD 3.45/kg, supported by steady demand. Milk production in the region remains strong as the spring flush progresses. Nonetheless, demand for SMP and WMP is stable, with WMP output increasing and export activity picking up, particularly with Argentina leading recent shipment growth.

2. Price Analysis

High Production and Softer Demand Drive Bearish Sentiment in Dairy Market

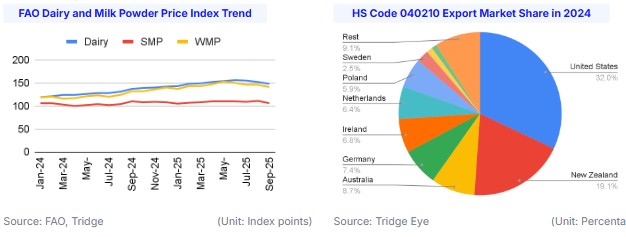

According to the Food and Agriculture Organization (FAO), the global dairy price index declined by 2.63% month-on-month (MoM) in Sep-25, reaching 148.26 points. Specifically, SMP prices dropped 4.28% MoM to 106.02 points, while WMP decreased by 3.09% to 141.22 points. The decline was largely driven by weaker demand from major importers and increased competition among exporters. This trend is consistent with the latest fortnightly held event, Global Dairy Trade (GDT) auction on October 7, where SMP prices fell by 0.5% to USD 2,599 per metric tons (mt), and WMP declined by 2.3% to USD 3,696/mt. Given this environment, the milk powder market outlook remains bearish, as global production stays high while demand remains sluggish.

In the EU, milk output continues to rise, increasing available volumes and keeping SMP production steady. WMP production is also steady, supported by ample milk supplies and a focus on fulfilling existing contracts, although spot trade remains limited. In Oceania, production is strengthening as the region moves into the peak milk season. Domestic SMP prices and near-term futures remain stable, indicating that domestic demand is adequately supplied, while export prices are slightly lower due to pressure from increased global milk production. WMP domestic prices were steady, although late-term futures contracted modestly, despite export demand staying firm. In South America, milk output continues to grow, supported by favorable weather conditions and a strong grain harvest, which may help moderate feed costs. However, stakeholder sentiment remains bearish, as rising operating costs are squeezing producer margins, and inflation is weakening consumer purchasing power.

3. Strategic Recommendations

Strategic Actions to Navigate Bearish Milk Powder Markets

Given the current bearish global milk powder market, stakeholders, particularly exporters in the EU and Oceania, should pivot towards demand-driven strategies to regain price momentum and mitigate inventory pressure. Exporters in the EU should intensify trade promotion efforts toward price-sensitive emerging markets, especially in North Africa and Southeast Asia. This will enable them to defend their market share against increasingly competitive Argentine shipments. Flexible pricing mechanisms and short-term promotional contracts could help stimulate movement in sluggish spot markets while preventing inventory buildup. At the same time, diversifying product portfolios toward higher-value dairy derivatives, such as fortified powders, infant formula bases, or specialized food service-grade powders, would help shield producers from commodity price pressure.

For Oceania suppliers facing oversupply, adjusting production scheduling and exploring forward contracts or hedging strategies could help manage pricing risks amid volatile futures markets. Strengthening logistics efficiency and shipment timing can help capture better price windows as WMP export demand remains relatively firm.

4. Price Indicators