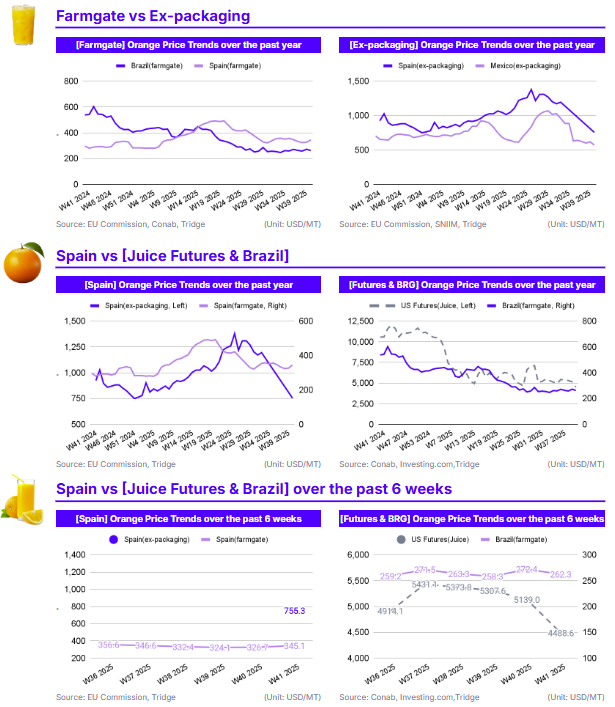

W41 2025: Orange

In W41 2025, global orange prices showed mixed patterns, with Spain’s farmgate price rising 5.63% week-on-week (WoW) to USD 345.1/mt due to immediate harvest disruptions and forecasts for a 16-year low crop. Conversely, prices in Brazil (USD 262.3/mt, -3.70% WoW) and Mexico (USD 571.0/mt, -7.66% WoW) fell, alongside US Futures (-12.66% WoW). This bearish trend is more pronounced long-term, with Brazilian and US Futures prices down over 51% year-on-year (YoY), correcting from 2024 peaks. Spain is the clear exception, up 16.55% YoY due to its localized supply crisis with a 16-year low harvest expected in 2025/26. Despite long-term structural supply risks from Brazil's citrus greening (HLB) and Spain's low harvest, Brazil's current low price presents a key sourcing opportunity. Buyers are advised to secure Brazilian contracts now before these structural supply deficits are fully priced into the market.

1. Weekly Price Overview

Spain Farmgate Prices Rise on Severe Supply Shocks While Brazil, Mexico, and US Decline

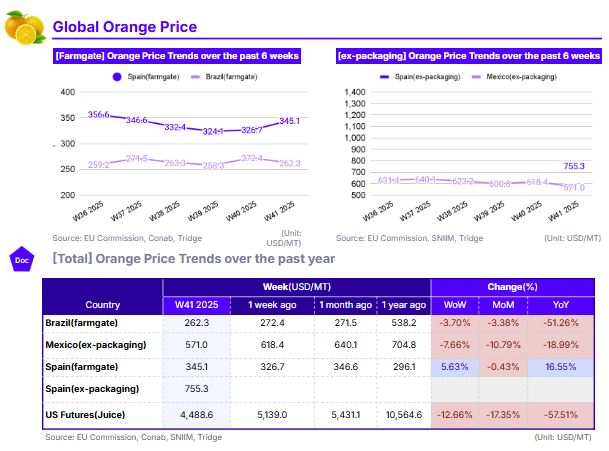

In Brazil, the farmgate price for oranges was USD 262.3/metric ton (mt) in W41, a decrease of 3.70% WoW. In Mexico, the ex-packaging price fell to USD 571.0/mt, marking a sharp 7.66% drop WoW. US Orange Juice Futures saw the steepest weekly fall, dropping 12.66% WoW to USD 4,488.6/mt. In contrast, Spain’s farmgate price rose 5.63% WoW to USD 345.1/mt. Spain's price jump is a direct response to acute, new-season supply fears. Reports of recent heavy rainfall in southeastern Spain are disrupting the start of the 2025/26 harvest, which is already forecast to be a 16-year low, down 11.6% from last year’s harvest. This creates supply fears for the 2025/26 harvest and upward price pressure. Conversely, the significant WoW declines in Brazil (-3.70%), Mexico (-7.66%), and US Futures (-12.66%) is likely due to increasing seasonal supply as the main harvest in these countries are ramping up, adding temporary bearish pressure to the market.

2. Price Analysis

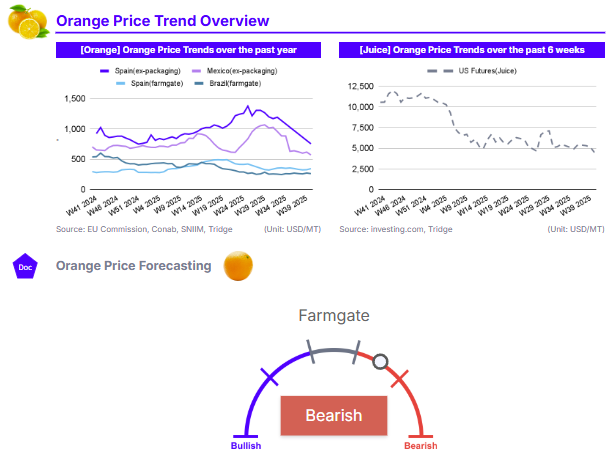

Global Prices Correct Sharply from 2024 Highs Amid Weak Demand

In Brazil, the orange farmgate price dropped 3.38% over the past month, contributing to a significant 51.26% collapse YoY from W41 2024. Mexico’s ex-packaging price followed this bearish trend, falling 10.79% month-on-month (MoM) and 18.99% YoY. US Orange Juice Futures recorded the most dramatic long-term correction, plunging 17.35% MoM and 57.51% YoY. Spain stands as the clear exception, with its farmgate price holding steady MoM (-0.43%) and posting a strong 16.55% gain YoY.

The massive YoY price decreases in Brazil (-51.26%) and US Futures (-57.51%) and to a lesser extent Mexico (-18.99%) is largely the result of supply recoveries in North and South America. Brazil is expecting a harvest of 306.7 million boxes of 40.8 kg which is a significant recovery over the 233 million boxes of the previous year. Similarly in the US, the California navel orange forecast is 80 million cartons, up 6% from the previous year. The US orange futures are especially impacted by Brazil’s harvest recovery considering that Brazil accounts for nearly 70% of the global supply for the juice industry. Conversely, Spain’s 16.55% YoY price increase highlights its severe supply crisis for the 2025/26 season. Forecasts of a 16-year low in production due to excessive rainfall in spring combined with high temperatures during critical periods of fruit development have insulated Spanish farmgate prices from the global bearish trend.

The outlook for global prices remains bearish in the short term, driven by increased supply especially from major producers in North and South America such as Brazil, Mexico and the US. However, Spain's prices are expected to continue rising as its historically small harvest fails to meet regional demand.

3. Strategic Recommendations

Secure Brazilian Orange Contracts While Low Prices Defy Longer Term Supply Risks

Global buyers, particularly juice processors, should capitalize on the current low farmgate prices in Brazil to secure volumes for the 2025/26 season. In W41, the Brazilian farmgate price of USD 262.3/mt is the most competitive in the global market, trading at a significant discount to both Mexico (USD 571.0/mt) and Spain (USD 345.1/mt). This price represents a 51.26% collapse YoY, offering a prime sourcing opportunity compared to the crisis-level pricing seen in 2024.

While current prices are low, buyers should be aware that this is occurring despite a deeply troubled supply chain. Brazil's 2025/26 harvest, while a significant recovery from last year's 30-year low, is not a large crop by historical standards and was recently revised downward due to the accelerating spread of citrus greening (HLB). Furthermore, key competitor Spain is forecasting its worst harvest in 16 years, which will increase European reliance on Brazilian imports. Buyers should view the current low prices as a window of opportunity before the full structural impact of Brazil's and Spain's poor harvests is priced into the global market. According to Tridge Eye data, suppliers worth considering in Brazil include NCD Brazil, GBG, and Soeli Desouza Ferris