In W42, global butter markets showed mixed trends, with European prices recording slight week-on-week (WoW) gains but remaining significantly lower year-on-year (YoY), while United States (US) prices continued to decline. Ample milk production, high butterfat yields, and lower feed and energy costs have kept European Union (EU) inventories elevated, though prices are expected to strengthen slightly during the winter and festive season when milk output typically declines. In contrast, US butter prices fell to a four-year low, following abundant cream supplies and a rise in milk output in major dairy states during the first eight months of 2025. To adapt, EU processors are recommended to align production with seasonal demand, expand exports to high-priced regions such as Asia and the Middle East, and diversify into value-added or blended butter variants. Meanwhile, US producers should rationalize production, redirect excess cream to alternative dairy uses, and leverage competitive pricing to expand export partnerships in Asia and Latin America.

1. Weekly Price Overview

Butter Prices Recover Marginally in Europe, While US Market Weakens on Ample Cream Supply

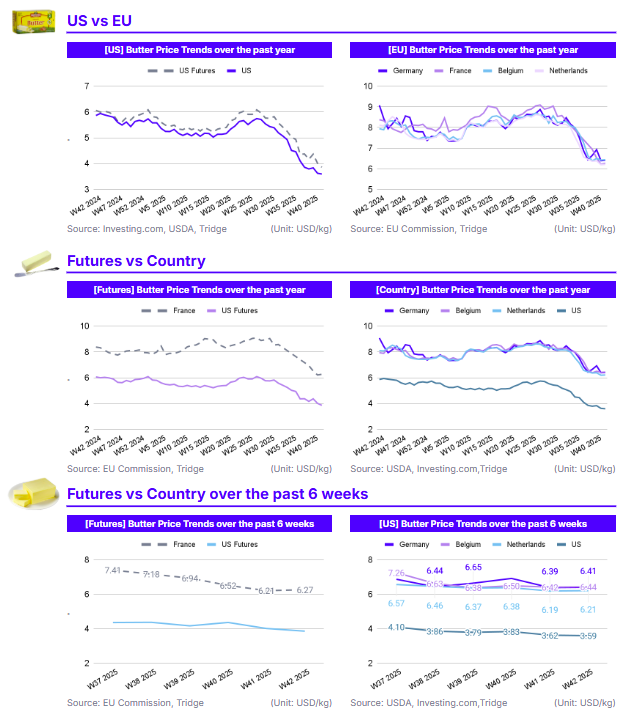

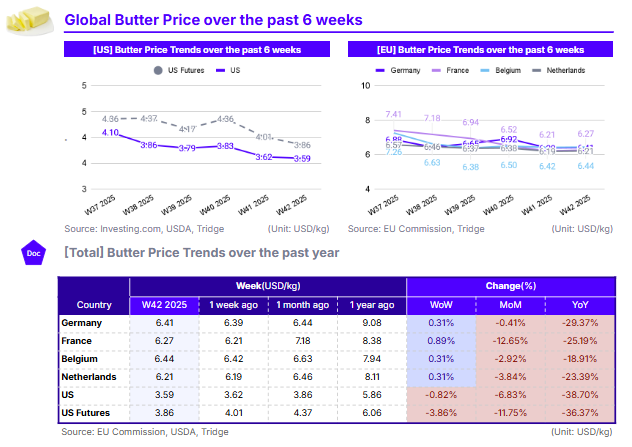

In W42, European butter prices registered slight WoW gains but remained significantly lower YoY. In Germany, prices increased 0.31% WoW to USD 6.41 per kilogram (kg) but were still 29.37% lower YoY. France recorded a similar trend, with prices rising 0.89% WoW to USD 6.27/kg yet down 25.19% YoY, while Belgium’s prices averaged USD 6.44/kg, up 0.31% WoW but 18.91% lower YoY. In the Netherlands, butter prices climbed 0.31% WoW to USD 6.21/kg but declined 23.39% YoY. The modest weekly gains likely reflect the start of restocking by processors and retailers ahead of the winter and festive season. In contrast, the significant YoY declines suggest ample EU stocks, supported by strong milk production and lower feed and energy costs throughout 2025.

Meanwhile, US butter futures averaged USD 3.86/kg, marking a 3.86% WoW decline and a significant 36.37% YoY drop. Similarly, US butter grade AA averaged USD 3.59/kg, a 0.82% WoW drop and a 38.70% YoY fall. The decline was driven by abundant cream supplies, with fat levels in milk seasonally higher and contractual cream intakes largely meeting processors’ needs.

2. Price Analysis

Global Butter Prices Ease as Strong Milk Output Expands Supply in the US and EU

In the US, butter prices have fallen to their lowest level in four years, driven by abundant milk production and a surplus of cream. This marks a reversal from the record highs of 2023, when prices exceeded USD 3.50 per pound (lb). Higher milk output and increased butterfat content have expanded cream availability, easing supply pressures. According to the United States. Department of Agriculture (USDA), milk production in the major dairy states rose 1.8% during the first eight months of 2025, supported by improved yields per cow.

In the EU, butter prices have also remained subdued due to strong milk output and high component levels that have increased cream availability. Although market activity remains steady, inventories are building as supply continues to outpace demand. However, prices are expected to firm during the winter and festive season, when milk production typically dips across Europe. Despite the short-term optimism, prices will likely remain lower compared to the previous years.

3. Strategic Recommendations

Strategic Responses to Global Butter Oversupply and Seasonal Price Shifts

In Europe, where prices have shown slight WoW gains but remain significantly lower YoY, processors and traders should leverage the upcoming winter and festive season to optimize inventory turnover. This can be achieved by aligning production schedules with seasonal demand peaks and securing short-term contracts with retailers to prevent oversupply. Exporters could also capitalize on lower domestic prices by expanding sales to regions where butter prices remain elevated, such as Asia and the Middle East, improving margin recovery. Additionally, producers should explore value-added and blended butter variants, such as flavored or plant-fat-mixed spreads, to capture growing consumer interest in premium and functional products, helping offset price pressures in the traditional butter segment.

In the US, where butter prices have reached a four-year low due to high milk and cream availability, processors should focus on production rationalization and export expansion. Reducing production runs to match domestic demand and redirecting excess cream to alternative uses such as cheese, ice cream, or industrial fat production could help stabilize prices. Given the competitiveness of US butter in global markets, exporters should strengthen trade partnerships with import-reliant countries, particularly in Asia and Latin America, through forward contracts and promotional campaigns emphasizing product quality and consistency.