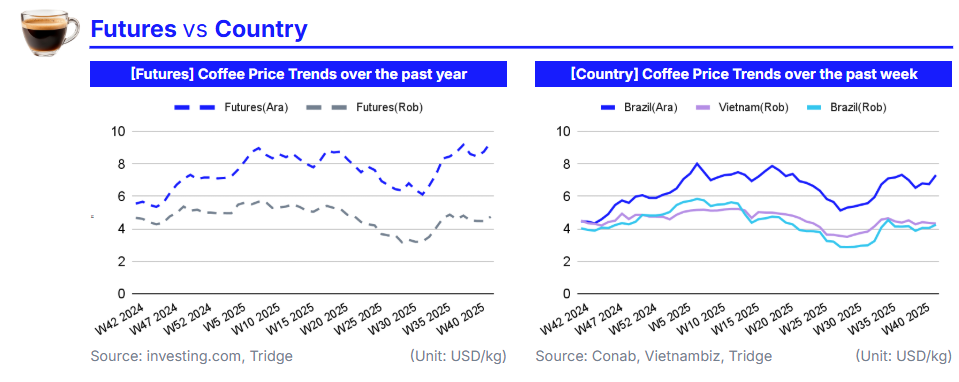

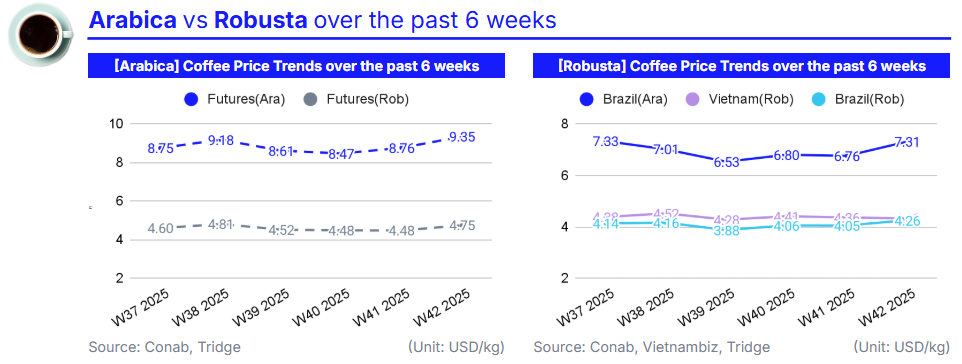

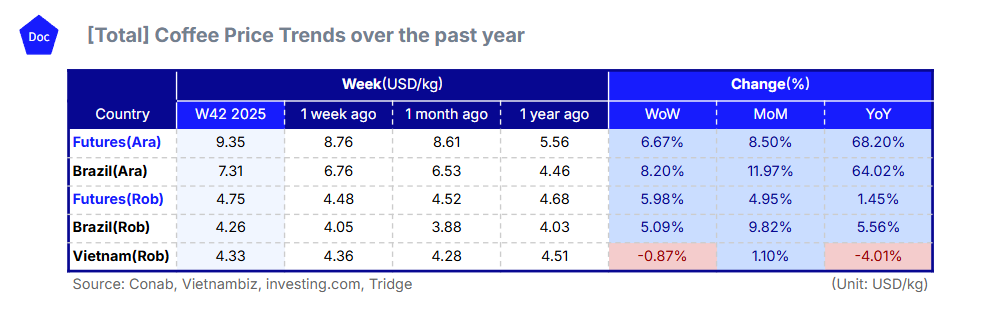

In W42 2025, global coffee prices rose sharply amid low inventories and adverse weather. Arabica (US Coffee C Futures) gained 6.67% WoW to USD 9.35/kg, while Robusta (London Coffee Futures) increased 5.98% WoW to USD 4.75/kg. In Brazil, Arabica surged 11.97% MoM to USD 7.31/kg and Robusta rose 9.82% MoM to USD 4.26/kg, supported by dry conditions in Minas Gerais and the 50% US tariff, which has restricted exports. Vietnam’s Robusta edged down slightly as heavy rains disrupted harvests. Domestic consumption in Brazil is softening, but specialty and premium coffees remain strong. Prices are expected to stay firm short-term, and buyers are advised to secure forward contracts with Brazilian exporters to hedge against continued volatility.

1. Weekly Price Overview

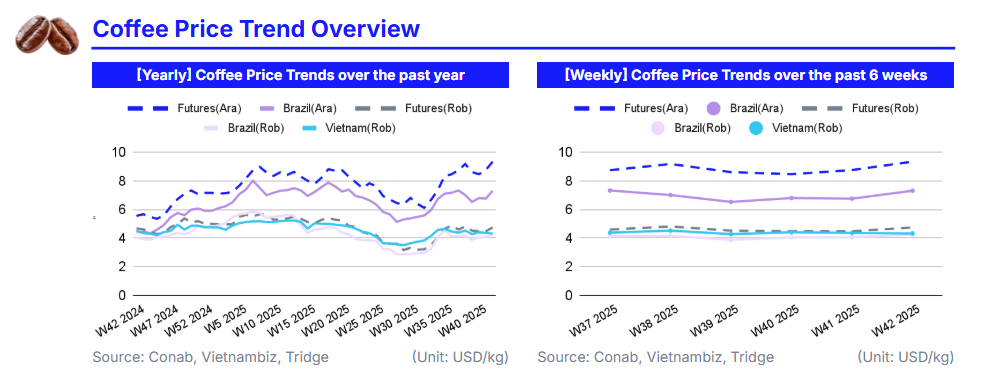

Brazil’s Dry Weather and Vietnam’s Floods Drive Diverging Coffee Price Trends

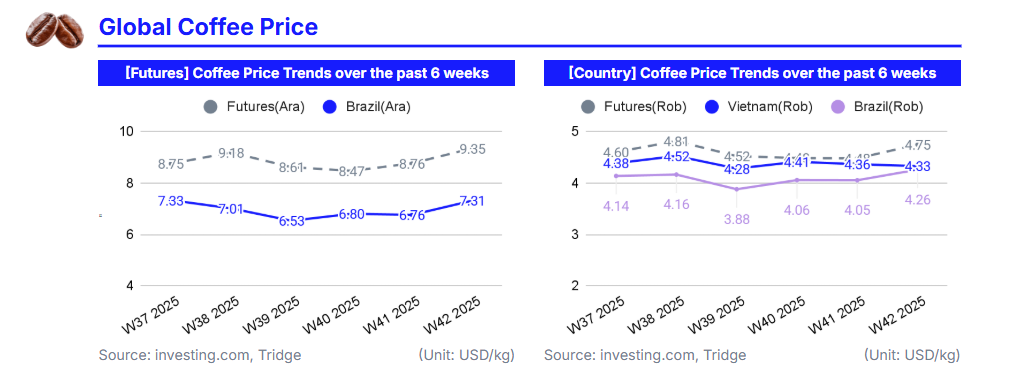

As of W42 2025, global coffee prices continued their upward trajectory amid tightening inventories and adverse weather in major producing countries. The international Arabica price, represented by US Coffee C Futures, surged 6.67% week-on-week (WoW) to USD 9.35/kg, while Robusta, represented by London Coffee Futures, rose 5.98% WoW to USD 4.75/kg. The rally was fueled by historically low certified stocks at the Intercontinental Exchange (ICE), with Arabica inventories falling to a 19-month low of 465,910 bags and Robusta to a three-month low of 6,141 bags, reinforcing global supply concerns.

In Brazil, Arabica climbed 8.20% WoW to USD 7.31/kg and Robusta rose 5.09% WoW to USD 4.26/kg, supported by irregular rainfall and strong winds in Minas Gerais that threaten flowering and fruit formation. Analysts warn that continued dry conditions in the coming weeks could cause irreversible production losses. Adding to market pressure, the 50% US tariff on Brazilian coffee has restricted import flows and heightened volatility in futures markets.

In Vietnam, Robusta prices declined by 0.87% WoW to USD 4.33/kg as heavy rains and flooding in the Central Highlands disrupted harvest progress. Despite the short-term impact, official projections remain optimistic, with the 2025/26 crop expected to reach 31 million bags and exports around 25 million. Global coffee prices remain supported by low stock levels, weather-related supply risks, and heightened trade tensions, suggesting sustained price strength through the coming weeks.

2. Price Analysis

Brazilian Coffee Surges on Tight Stocks and Adverse Minas Gerais Weather, Volatility Persists

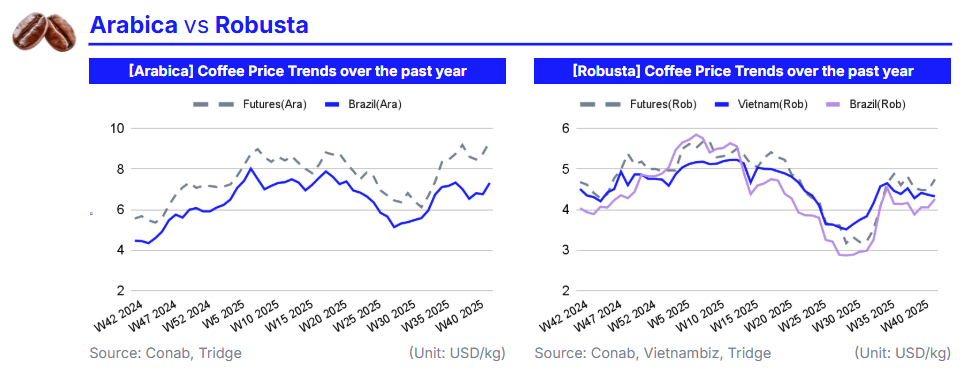

In W42 2025, Brazil’s coffee prices continued their strong upward momentum, driven by tightening inventories and adverse weather conditions in key producing regions. Arabica prices in Brazil surged 11.97% month-on-month (MoM) to USD 7.31/kg, while Robusta rose 9.82% MoM to USD 4.26/kg. The increase stems primarily from low certified stocks at the Intercontinental Exchange (ICE), with Arabica inventories falling to a 19-month low of 465,910 bags, amplifying concerns over supply scarcity. In Minas Gerais, the country’s largest Arabica-producing region, irregular rainfall and strong winds have disrupted flowering and early fruit formation, raising the risk of irreversible yield losses if dry conditions persist. This weather stress, coupled with a 50% US tariff on Brazilian coffee, has restricted export flows and increased volatility across futures markets. Meanwhile, Vietnam’s Robusta harvest pressures the global market slightly, but the effect on Brazilian Robusta has been limited due to ongoing domestic and export demand.

Despite strong export prices, domestic consumption in Brazil is weakening. Recent surveys show that the share of consumers drinking more than six cups of coffee daily fell from 30% in 2023 to 26% in 2025, while 39% now prioritize the cheapest options, reflecting price fatigue. Coffee shop visits have also declined, with many consumers returning to home preparation as a cost-saving measure. This demand softness could dampen domestic price transmission in the coming months, especially for lower-grade blends. Nonetheless, the premium segment—particularly award-winning and specialty coffees from Minas Gerais—continues to command prices up to three times higher than standard lots, sustained by online sales and quality competitions.

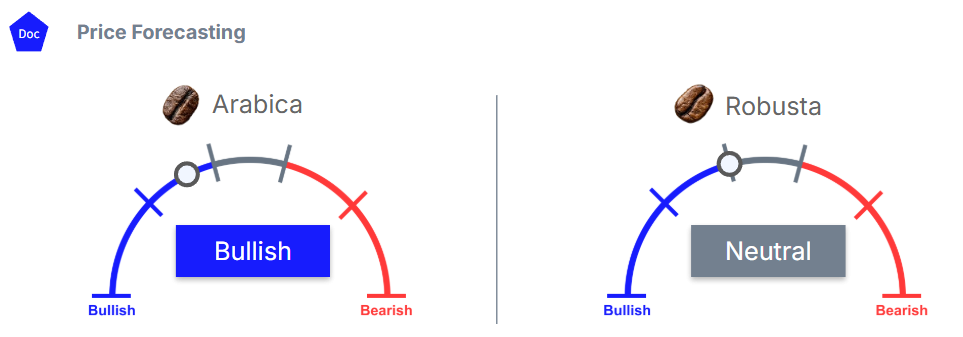

Looking ahead, Brazilian coffee prices are expected to remain firm in the short term as low exchange inventories and weather-related risks support elevated Arabica values. If dry conditions persist in Minas Gerais and trade tensions with the US remain unresolved, Arabica could climb further toward the USD 9.50/kg mark, while Robusta may consolidate around USD 4.30–4.50/kg. Conversely, the onset of regular rains and progress in tariff negotiations could ease upward pressure by late Q4-2025, bringing Arabica back toward USD 6.80–7.50/kg. Overall, Brazil’s coffee market is likely to stay volatile, with asymmetric risk skewed to the upside until clearer signals emerge on weather patterns and trade policy.

3. Strategic Recommendations

Capitalize on Brazil’s Coffee Supply Tightness Amid Weather Risks and US Tariff Uncertainty

Global coffee buyers should consider prioritizing Brazil as the main procurement source for Arabica and Robusta contracts in the short term (Q4-2025 – Q1-2026), as market conditions indicate strong upside potential amid tight inventories and adverse weather. Brazilian Arabica surged 11.97% MoM to USD 7.31/kg, and Robusta rose 9.82% MoM to USD 4.26/kg, driven by a 19-month low in ICE-certified stocks and irregular rainfall in Minas Gerais, which threatens flowering and fruit formation. The combination of supply constraints, ongoing US tariff uncertainty, and volatility in futures markets is likely to sustain price strength through the coming weeks, while domestic consumption shows signs of weakening, particularly for lower-grade blends.

This situation presents a strategic window for global importers, roasters, and industrial users to secure forward contracts or fixed-price agreements with leading Brazilian exporters such as Melitta, Nestlé Brasil, and smaller specialty producers. By securing supply now, buyers can hedge against further upside driven by weather-related yield risks and potential trade disruptions, while also gaining access to high-quality Arabica and Robusta for premium or standard products. For Robusta, Vietnam remains a secondary source, but the Brazilian market offers more predictable quality and export logistics. Buyers should consider structuring multi-month forward purchases or staggered delivery contracts to mitigate short-term volatility, optimize cost, and ensure continuous supply for the upcoming 2025/26 cycle.