W48 2025: Beef

In W48, global beef markets showed generally strong trends, supported by festive-season demand and tight supply in key regions. EU beef prices rose on limited domestic production, while Brazil saw moderate gains driven by stronger domestic consumption, despite competition from cheaper proteins like chicken. Argentina experienced price increases due to festive demand and bull shortages, while US live cattle futures were supported by tight supplies and wintry weather. The FAO reported a slight rise in the global beef index despite overall declines in the meat price index, reflecting steady international demand. Brazil rapidly resumed beef exports to the US following the removal of a 50% tariff, with shipments expected to grow significantly. Meanwhile, Australia achieved record exports driven by strong global demand and premium positioning, especially in the US, Japan, and South Korea. Across these markets, producers and exporters are recommended to focus on improving supply chain efficiency, capturing high-margin opportunities, emphasizing quality, and diversifying trade to sustain growth and maintain market competitiveness.

1. Weekly Price Overview

Global Beef Market Strengthens Due to Tight Supplies and Festive Demand

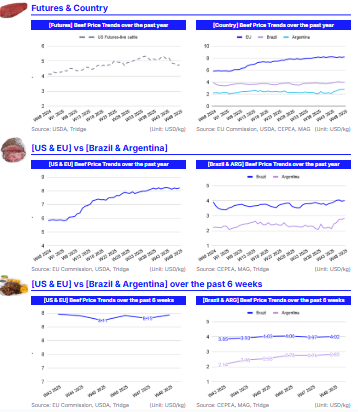

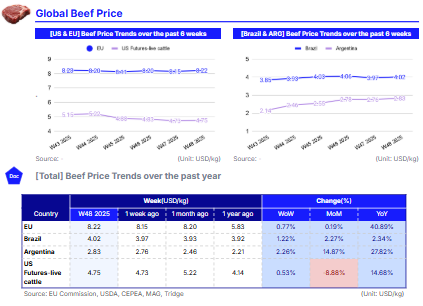

In W48, the European Union (EU) beef prices averaged USD 8.22 per kilogram (kg), a 0.77% week-on-week (WoW) rise, a 0.19% month-on-month (MoM) increase, and a significant 40.89% year-on-year (YoY) surge. This sustained upward momentum is primarily driven by declining production and tightening domestic supply. With the festive season approaching, demand is expected to remain firm, helping keep prices elevated.

In Brazil, beef prices averaged USD 4.02/kg, rising 1.22% WoW, 2.27% MoM, and 2.34% YoY. The uptick is largely attributed to stronger domestic consumption heading into the festive period, when demand seasonally increases. However, beef continues to face competition from more affordable proteins such as chicken, which may limit upward price movement.

In Argentina, beef prices averaged USD 2.83/kg, recording a 2.26% WoW, 14.87% MoM, and 27.82% YoY increase. The sharp rise is linked to festive-driven demand and a shortage of bulls, which has pushed up processing costs and driven price gains in both domestic and export markets.

Meanwhile, United States (US) live cattle futures stood at USD 4.75/kg, up 0.53% WoW and 14.68% YoY, though down 8.88% MoM. The market remains supported by tight cattle supplies and wintry weather across parts of the central and northern Plains, which has contributed to supply constraints.

2. Price Analysis

Global Beef Markets Show Resilience as US Tariffs Change and Demand Remains Strong

According to the Food and Agriculture Organization (FAO), the global meat price index declined to 124.58 points in Nov-25 from 125.55 points in Oct-25. The drop was driven by decreases in poultry and pork, which more than offset increases in lamb and beef. The beef index rose slightly from 147.5 points in Oct-25 to 147.8 points in Nov-25, supported by steady international demand despite a slight limitation from the removal of US tariffs on imported Brazilian beef, which eased upward pressure on Australian prices. Nevertheless, US buyers continued seeking high-quality imports, helping maintain firmness in the global beef market.

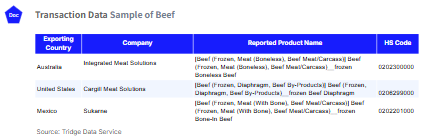

Brazil emerged as a major focus, rapidly restoring beef shipments to the US after the removal of the additional 50% tariff. Exporters quickly resumed production, and shipments are expected to rise from 12.6 thousand mt in Nov-25 to around 35 thousand metric tons (mt) in Dec-25, potentially reaching 50 thousand mt in Jan-26. Although tariff-related disruptions led Brazil to redirect volumes to Asia, Europe, Chile, and Russia, at lower margins, the reopening of the US market is set to boost revenues and strengthen supply flows. The US continues to offer significantly higher prices, making it a key market as Brazilian exporters plan to expand their presence.

Australia also recorded a landmark year, shipping 1.398 million metric tons (mmt) in the first 11 months of 2025, up 15% YoY. This growth is driven by strong global demand and solid domestic production. The US remained Australia’s largest export market, absorbing over 412 thousand mt over the period despite the temporary imposition of a 10% tariff. Japan, South Korea, and other Asian and Middle Eastern markets contributed to the record performance, while grain-fed beef exports also reached new highs.

3. Strategic Recommendations

Optimize Beef Production and Exports in Response to Rising Prices and Demand

In the EU, due to tightening domestic supply and strong festive-season demand, producers and processors should focus on improving supply chain efficiency to ensure consistent product availability, particularly during peak demand periods. Retailers and processors can also introduce value-added products, such as ready-to-cook festive packages or premium cuts, to maximize margins while meeting consumer preferences.

For Brazil, the removal of US tariffs presents a key opportunity to expand exports and capture higher-margin sales. Exporters should prioritize US orders, ensuring rapid production and delivery. However, they should maintain diversified trade with Asia, Europe, and the Middle East to reduce dependency on a single market. Given competition from cheaper proteins like chicken, Brazilian companies should also consider product differentiation, such as emphasizing quality, safety certifications, or branded beef cuts, to maintain their competitive edge.

In Argentina and Australia, the focus should be on addressing supply constraints and capturing premium markets. In Argentina, companies should streamline processing and improve cattle availability to meet both domestic and export demand, especially during the festive season when prices spike. For Australia, maintaining high-quality standards and emphasizing grain-fed or premium beef will preserve price premiums and strengthen market positioning. Australian exporters should continue to target high-demand markets such as the US, Japan, and South Korea, while exploring growth in emerging regions.