In W48, European butter prices plummeted, with major markets like Germany, France, Belgium and the Netherlands registering YoY declines exceeding 32% due to abundant cream and cautious buyer sentiment. Similarly, US butter prices fell by over 40% YoY, maintaining its status as the cheapest amid the strongest four-month milk production growth since 2012, which supports strong export momentum. Globally, dairy prices continued to soften in Nov-25, as shown by consecutive declines in the FAO dairy index and falling GDT butter prices. The downward trend was driven by strong export availability from the EU and New Zealand. To navigate this environment, EU processors are recommended to de-commoditize butter, secure forward contracts, and invest in higher-value fractionated products. US processors should leverage low prices to expand exports and secure long-term domestic contracts. Meanwhile, New Zealand should continue prioritizing higher-value milk fat and cheese categories to sustain export returns.

1. Weekly Price Overview

European and US Butter Prices Plummet as Abundant Cream and High Production Drive Down Markets

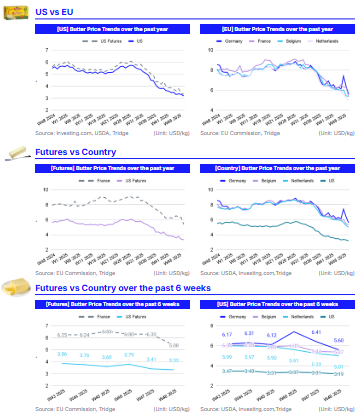

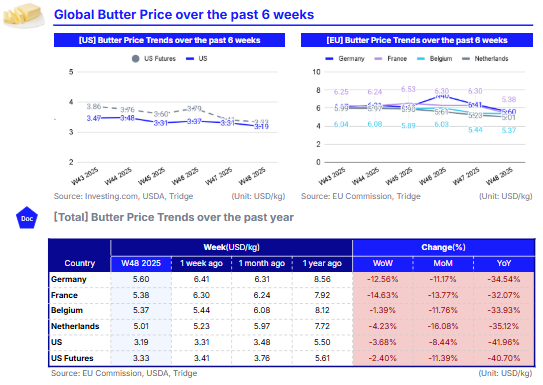

In W48, Germany’s butter prices averaged USD 5.60 per kilogram (kg), down 12.56% week-on-week (WoW), 11.17% month-on-month (MoM), and 34.54% year-on-year (YoY). France followed a similar pattern, with prices at USD 5.38/kg, falling 14.63% WoW, 13.77% MoM, and 32.07% YoY. Belgium saw a more modest weekly drop of 1.39% to USD 5.37/kg, though monthly and yearly declines reached 11.76% and 33.93%, respectively. Dutch butter prices fell 4.23% WoW, 16.08% MoM, and 35.12% YoY, reaching USD 5.01/kg. This widespread downward trend in the European Union (EU) is mainly attributed to abundant cream availability and strong milk flows, which kept supply pressure high. Buyers remained cautious, focusing on immediate needs rather than extending coverage. Forecasts suggest further moderation in momentum as softer milk prices and rising non-feed costs are expected to impact production heading into the next milk year.

Meanwhile, United States (US) butter prices also faced significant pressure, averaging USD 3.19/kg, down 3.68% WoW, 8.44% MoM, and 41.96% YoY. Similarly, US butter futures fell 2.40% WoW, 11.39% MoM, and 40.70% YoY to USD 3.33/kg. Continued high production remains a key factor weighing on the market. Although retail discounting may offer some short-term support, with holiday demand largely fulfilled and cream output remaining strong, US butter prices may experience further downward pressure in the near term.

2. Price Analysis

Global Dairy Prices Drop on High Production and Export Surpluses

Global dairy prices continued to decline in Nov-25, with the Food and Agriculture Organization (FAO) dairy price index falling to 137.47 points from 141.9 in Oct-25. This marked the fifth consecutive monthly decrease, driven by higher milk production and abundant export supplies, particularly in the EU and New Zealand. Butter prices were notably weaker, with the index falling to 173.33 points from 182.83 points in Oct-25, reflecting increased export competition and large inventories. This trend aligns with the December 2 held Global Dairy Trade (GDT) event, where butter prices averaged USD 5,169 per metric ton (mt), a 12.4% drop from the previous event.

New Zealand’s Oct-25 export data showed strong value growth despite mixed changes in volumes. The value of milk powder, butter, and cheese exports reached USD 2.10 billion, up 18% YoY, while fresh milk and cream exports rose 21% YoY. Export volumes showed declines in milk powder but increases in milk fats and cheese. The EU also recorded significant butter surpluses of 93.7 thousand mt in the first three quarters of 2025, supported by lower cream prices, falling from over USD 11643.75/mt (EUR 10,000/mt) the previous year to around USD 4657.50/mt (EUR 4,000/mt), fueling higher production at reduced cost.

Meanwhile, US milk production recorded the strongest four-month YoY growth since 2012, helping make US butter the cheapest globally and sustaining strong export momentum. Retail and food service demand in the US is stable to improving, cream availability remains high, and butter production is operating near capacity as inventories hold steady or decline.

3. Strategic Recommendations

Optimize Processing Efficiency and Pursue Export Market Share Amid Declining Prices and Increased Production

Given the persistent butter surpluses driven by abundant cream and high milk flows in the EU, processors should prioritize strategies to de-commoditize its large volumes and manage rising future costs. They should also shift from volatile spot sales to secured forward contracts for commodity butter to hedge against YoY price drops and lock in current margins. Additionally, they should leverage the current low cost of cream to accelerate investment in butter-fractionation technology to convert bulk butter into higher-value ingredients like anhydrous milk fat (AMF), which commands better margins in the international ingredient trade.

For the US, processors should start an aggressive export drive by prioritizing cost-sensitive markets in Asia and Latin America. Their low prices give them an immediate edge over EU and Oceania suppliers. Temporary trade financing or export subsidies may be needed to swiftly secure market share. Domestically, they should exploit the stable-to-improving retail demand by negotiating longer-term supply agreements with major domestic chains to secure consistent sales volume and reduce exposure to global price fluctuations.

New Zealand's dairy sector, which has maintained strong export value growth despite mixed volumes, should focus on sustaining value differentiation and strategically reallocating milk solids. New Zealand exporters should continue to prioritize increasing the volume and value of milk fats and cheese exports over milk powder, strategically allocating milk solids towards these higher-performing categories.