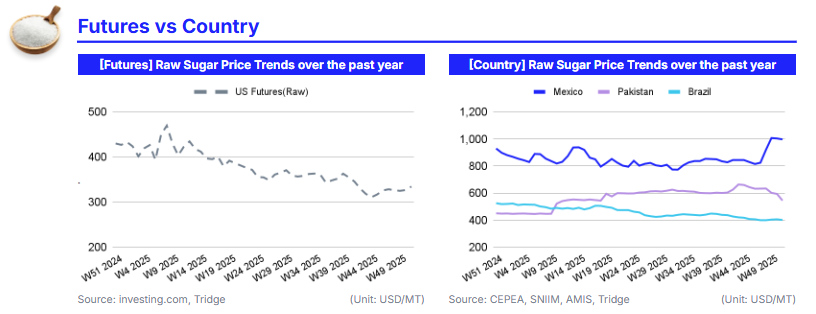

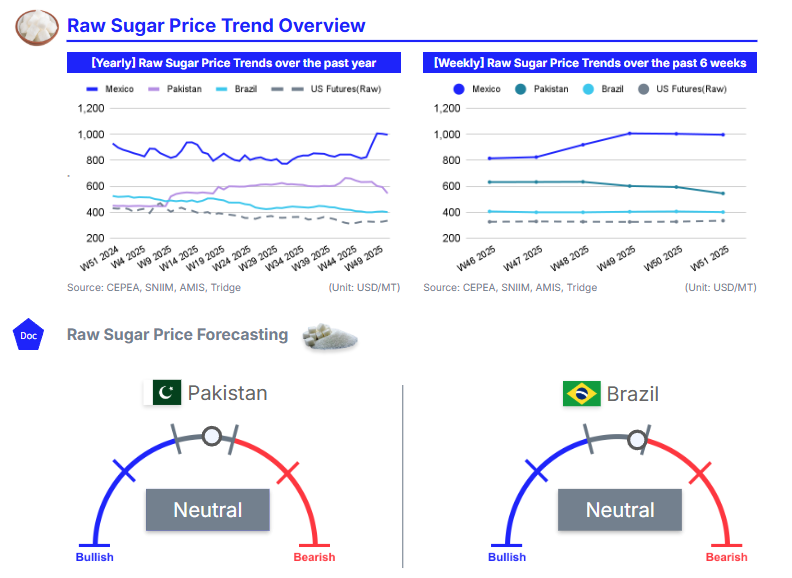

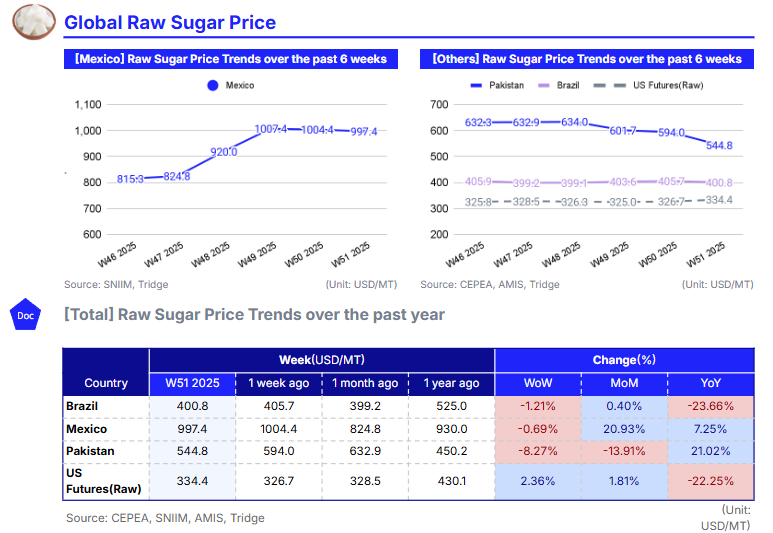

In W51 2025, global sugar markets remain firmly surplus-driven, with prices capped by strong availability from Brazil and uneven, policy-led dynamics elsewhere. Brazilian sugar prices decreased to USD 400.8/mt, reflecting a weak BRL, improving Center-South cane productivity, and a sharp recovery in ATR, which together have reinforced Brazil’s position as the most competitive origin despite cumulative yields still trailing last season. Mexico continues to trade at a significant premium, with prices elevated by regulatory distortions linked to illegal milling activity and enforcement uncertainty rather than genuine supply tightness. Meanwhile, Pakistan has seen prices soften sharply amid administrative intervention, ample prompt availability, and slow crushing progress, although medium-term uncertainty persists due to pending deregulation.

For global food manufacturers sourcing Brazilian sugar, the core strategy is to anchor near-term coverage in Brazil through staggered spot or short-dated contracts, leveraging abundant export availability and limited upside risk. Exposure to Mexico should be minimized and treated tactically, given the vulnerability of current price levels to policy normalization, while Pakistan warrants a flexible, wait-and-see approach as near-term softness may give way to stabilization later in the season. Overall, with global balances comfortable and no material weather disruption evident, sugar prices are expected to remain range-bound with a bearish-to-neutral bias into early 2026, favoring disciplined, short-horizon procurement over long forward commitments.

1. Weekly Price Overview

Weak Brazilian Real, Rising Center-South Yields, and Policy Actions Drive Broad Sugar Price Declines

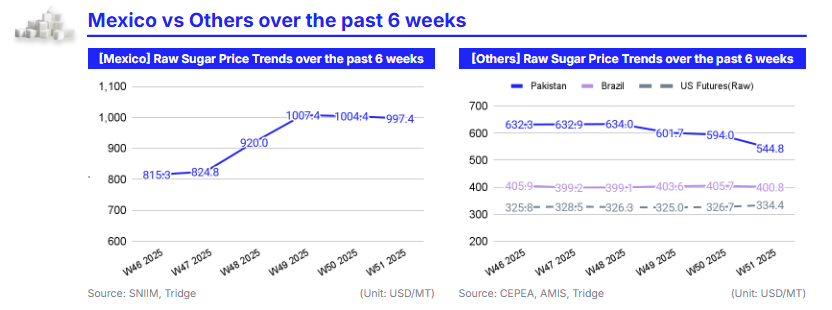

In W51 2025, global sugar markets remained under broad bearish pressure over the past two weeks, driven primarily by currency movements, rising supply, and ample inventories across key producing regions. Brazil’s sugar prices declined by 1.21% week-on-week (WoW) to USD 400.8 per metric ton (mt) and down 23.66% year-on-year (YoY), reflecting the depreciation of the Brazilian real (BRL) to a four-month low, which incentivised exports and increased availability on the global market. This pressure was reinforced by improved short-term agronomic conditions in the Center-South, where Nov-25 cane productivity rose 0.7% YoY to 63.3 mt per hectare (ha) and total recoverable sugar (ATR) improved by 8.6% to 134.3 kg/mt, enhancing production efficiency despite cumulative 2025/26 yields still tracking 4.9% below last season due to earlier climatic and operational disruptions. Mexico’s sugar prices eased 0.69% WoW to USD 997.4/mt amid slowing domestic demand under persistent inflationary pressure and rising concerns over illegal milling activity, which producers warn is distorting market prices and exacerbating oversupply risks despite government support for domestic consumption under Plan Mexico.

Pakistan recorded one of the sharpest declines, with sugar prices falling 8.27% WoW to USD 544.8/mt and down 13.91% month-on-month (MoM), following strict government enforcement against hoarding and speculation. Improved availability from ongoing crushing, large domestic stocks, and the presence of imported sugar have sharply lowered wholesale prices, with forward deals indicating expectations of further downside. By contrast, United States (US) raw sugar futures rose 2.36% WoW to USD 334.4/mt, rebounding modestly from recent multi-year lows despite a fundamentally bearish backdrop. Abundant global supply, weak domestic demand, and elevated stocks-to-use ratios continue to weigh on the US market, while higher tariffs on Brazilian sugar and reduced import volumes have limited direct exposure to global price declines. Strong production prospects in Brazil and globally continue to anchor sugar markets in a surplus-driven, bearish environment, with only short-term regional factors offering temporary price support.

2. Price Analysis

Sugar Prices Ease on Brazil Supply Strength, While Policy Distortions Sustain Divergence Across Key Markets

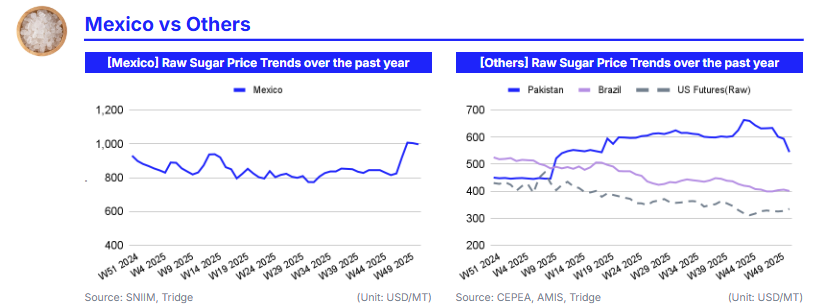

Recent sugar price movements reflect a widening gap between supply-driven adjustments in Brazil and policy-driven dynamics in Mexico and Pakistan. In Brazil, prices declined 0.69% WoW but remained marginally higher MoM at USD 399.2/mt, as improved cane yields and a sharp recovery in cane quality offset concerns about cumulative harvest losses. November productivity rose to 63.3 mt per hectare (ha), and ATR increased by 8.6% to 134.3 kg/mt, thereby improving near-term sugar availability and reinforcing the perception of a comfortable prompt supply. Although cumulative productivity and ATR remain slightly below last season, the current improvement in recoverable sugar content has weighed on spot prices, limiting upside momentum despite earlier seasonal tightness.

In contrast, Mexico’s sugar prices surged 20.93% MoM to USD 824.8/mt, despite short-term WoW softness, reflecting structural distortions rather than underlying supply strength. Allegations of illegal sugar mills and unregulated sugar inflows have intensified market uncertainty, tightening effective supply for formal channels and amplifying price volatility. Producer pressure for stricter enforcement and support for import-substitution policies has sustained elevated prices, even as these gains remain vulnerable to policy normalization or improved regulatory oversight.

Pakistan’s sugar prices declined 13.91% MoM to USD 450.2/mt, though they remain sharply higher YoY, as weak spot demand and operational delays during the crushing season weighed on prices. Slow crushing progress and uncertainty surrounding sugar sector deregulation have disrupted market activity, temporarily depressing prices despite no clear evidence of surplus production. The prospect of deregulation by mid-2026 introduces medium-term uncertainty, as delayed policy clarity risks discouraging cane planting and could tighten supply later in the year.

Global sugar prices are likely to maintain a bearish-to-neutral bias in the near term. Brazil’s improving cane quality and stable output prospects should continue to cap international prices, particularly if weather conditions remain favorable. Mexico’s prices are expected to remain elevated but volatile, highly sensitive to enforcement actions and trade policy shifts. Pakistan faces a more balanced outlook, with near-term softness likely to give way to stabilization or mild recovery if crushing delays translate into tighter availability later in the season. Overall, absent a material weather shock in major producing regions, current supply conditions suggest limited upside for global sugar prices into early 2026.

3. Strategic Recommendations

Maintain Defensive Coverage and Monetize Regional Price Dislocations in a Bearish Sugar Market

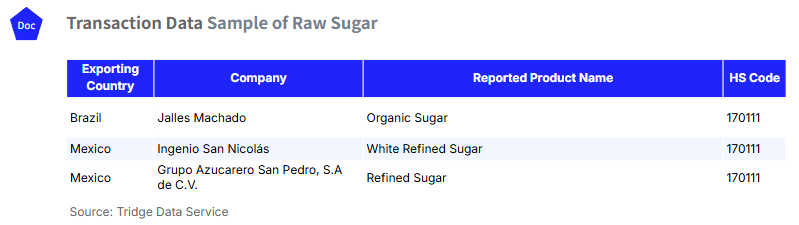

Given the prevailing surplus-driven conditions and the bearish-to-neutral price outlook into early 2026, sugar procurement strategies should remain opportunistic and short-dated. Brazil continues to offer the most competitive and reliable supply, as improving cane productivity and higher recoverable sugar content cap upside risk despite earlier seasonal losses. According to Tridge Eye’s transaction data explorer, Brazilian export availability includes organic sugar from domestic suppliers, supporting steady spot liquidity and limiting upside risk. This favors staggered spot or nearby-term purchases from Brazil to secure low absolute prices while maintaining flexibility should global prices soften further.

In contrast, Mexico’s sugar market remains structurally distorted by regulatory uncertainty rather than constrained by production fundamentals. Elevated prices are being sustained by enforcement actions against illegal milling activity and concerns over unregulated sugar flows, which have tightened effective supply in formal channels. Tridge Eye transactional data indicates ongoing trade in white refined sugar from Ingenio San Nicolás and refined sugar from Grupo Azucarero San Pedro, S.A de C.V., highlighting that supply remains available but is being priced at a policy-inflated premium. Exposure to Mexico should therefore be managed defensively, with sales prioritized into current price strength and inventory commitments kept limited to mitigate downside risk if enforcement improves or trade dynamics normalize.

Pakistan’s near-term price weakness reflects administrative intervention, ample prompt availability, and slow crushing progress rather than a structural surplus. While current conditions favor delayed buying, prolonged operational delays and uncertainty surrounding sector deregulation could tighten availability later in the season. As a result, maintaining optionality through flexible contracting remains prudent. Overall, the recommended approach is to anchor near-term coverage in Brazil, selectively monetize policy-driven price dislocations in Mexico, and remain tactically flexible in Pakistan, balancing cost control with protection against episodic volatility in an otherwise range-bound global sugar market.