In W6 in the orange landscape, some of the most relevant trends included:

- Global orange production is declining due to adverse weather in major producing countries, and while Brazil's output is increasing, it is insufficient to offset global losses.

- Processing demand is rising, as reduced fresh orange supply pushes more fruit into juice production, particularly in Brazil and Spain, influencing price trends.

- Export competition is intensifying, with Egypt maintaining a strong presence in EU markets despite lower production, pressuring prices in Greece and Spain.

- High transportation and production costs continue to challenge growers, limiting profitability and price recovery in key markets like Spain and Italy.

- Changing consumer demand is shifting sales channels, with fresh orange consumption declining in some markets, pushing sales toward specialty stores and local markets.

1. Weekly News

Global

Global Orange Production Declines in the 2024/25 Season

Global orange production for the 2024/25 season is expected to decline by over 600 thousand metric tons (mt) to 45.22 million metric tons (mmt), despite Brazil’s orange production being projected to increase to 13 million metric tons (mmt). However, sharp declines in other countries will offset these gains. Egypt’s production is expected to drop by 12% to 3.7 mmt. Turkey’s production will decrease to 1.6 mmt. The United States (US) will see its lowest harvest in 88 years at 2.2 mmt. Meanwhile, China’s production remains stable at 7.6 mmt. The European Union (EU) production will drop by 70 thousand mt to 5.7 mmt due to drought in Italy, whereas South Africa is expected to see a modest 1% increase to 1.7 mmt. With reduced global supply, orange consumption and exports are expected to fall, while processing volumes are likely to rise, driven by Brazil’s improved harvest.

Greece

Greek Orange Exports Slow as Egyptian Supply Increases

Greek orange exports reached 163 thousand mt by January 31, 2025, up from 146 thousand mt in the same period in 2024, but growth is slowing due to an influx of cheaper Egyptian oranges in EU markets. Despite Egypt’s projected 12% year-on-year (YoY) decline in orange production to 3.7 mmt due to adverse weather, it remains the EU’s top supplier, with exports expected to reach 1.95 mmt, down from 2.3 mmt last season. Market dynamics continue to be influenced by increased processing for juice, rising transportation costs linked to the Red Sea crisis, and ongoing EU trade agreements with Mediterranean countries, including Egypt.

Brazil’s Orange Juice Exports Decline Due to Limited Supply

Brazil’s orange juice exports in the 2024/25 season have been affected by reduced orange supply and limited juice stocks. Exports declined by 23% YoY from Jul-24 to Dec-24, totaling 448.5 thousand mt Frozen Concentrated Orange Juice (FCOJ) 66 Brix. This is the lowest level since 1997. Despite lower volumes, export revenue surged by 37% to USD 1.96 billion, driven by high global prices. The EU remained the top market, accounting for 55% of revenue, followed by the US at 35%. São Paulo's offseason further constrained juice availability, while elevated prices dampened international demand. A slight increase in supply was noted in late Jan-25 due to a fourth blossoming, though fruit quality remained below expectations.

Italy

Sicilian Orange Season Faces Challenges as Prices Rise

Italy’s Sicilian orange season faced early challenges due to drought and water shortages, resulting in smaller-sized Navelina oranges in Nov-24. Available from mid-December 2024, the Washington Navel variety showed better quality, though its season is expected to end earlier than usual—by late February instead of Easter. Blood orange varieties, including Moro and Tarocco, have been in full supply since late Dec-24, with Tarocco being more popular and priced USD 0.42 per kilogram (kg) higher. Sicilian orange prices have risen by up to USD 0.31/kg compared to last year, driven by higher transportation costs. Meanwhile, blood orange consumption has declined. Sales have shifted from mainstream retail to specialty stores and weekly markets. However, these markets are also decreasing, highlighting ongoing challenges for Sicilian producers.

Nepal

Nepal’s Palpa District Sees Strong Orange Harvest and Rising Farmer Incomes

Nepal’s Palpa district saw a strong orange harvest in 2024. Production rose to over 9 thousand mt from 8.8 thousand mt in 2023. Farmer earnings increased to USD 3.97 million, up from USD 3.46 million. Favorable weather, improved farming techniques, and growing market demand drove this increase, with six of the district’s ten local levels actively engaged in citrus cultivation. Rainadevi Chhahara led production with 3.6 thousand mt, followed by Ribdikot and Bagnaskali. Strong local demand and expanding market access have kept prices favorable, while better irrigation, organic fertilizers, and modern storage solutions have helped reduce post-harvest losses. However, challenges such as price fluctuations and disease management persist. Experts recommend investing in cold storage, transport infrastructure, and value-added products like orange juice and essential oils to enhance the industry's resilience and growth.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W6 2024 to W6 2025)

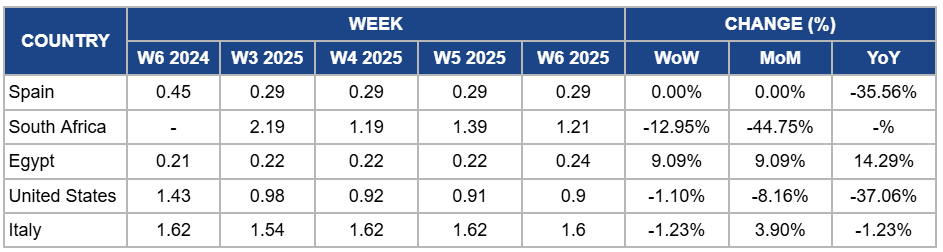

Spain

Orange prices in Spain held steady at USD 0.29/kg since W2 due to stable demand from juice processors, which continued sourcing supplies at consistent levels amidst steady domestic production. Additionally, the market remained balanced despite competition from lower-cost imports, as processing demand helped absorb available volumes. However, YoY prices dropped significantly by 35.56% due to persistent pressure from cheaper Egyptian imports, which have undercut local prices, and a decline in domestic fresh orange consumption. Moreover, Spanish farmers continue to struggle with high production costs, further limiting price recovery despite Spain's strong position in the EU citrus market.

South Africa

In South Africa, orange prices dropped by 12.95% week-on-week (WoW) to USD 1.21/kg in W6, marking a 44.75% MoM decrease due to increased processing volumes absorbing a larger share of production, reducing fresh market demand. Additionally, the expected slight production increase has contributed to higher supply availability, exerting downward pressure on prices. Global supply constraints have also limited export opportunities, further affecting price stability in the domestic market.

Egypt

Egypt's orange prices rose by 9.09% WoW and month-on-month (MoM) to USD 0.24/kg in W6, with a 14.29% YoY increase. The price increase is due to the projected decline in production for the 2024/25 season, leading to tighter supply in the market. Additionally, steady local demand and strong export interest have supported higher prices. The generally mild-to-hot weather has also influenced production dynamics, potentially affecting fruit quality and availability, further contributing to price growth.

United States

Orange prices in the US dropped slightly by 1.10% WoW to USD 0.90/kg in W6, with an 8.16% MoM decrease and a 37.06% YoY decline due to low demand and increased competition from imports, which offset concerns over Florida’s lower production forecast of 11.5 million boxes. Despite the decline in Florida’s orange production, market participants had already adjusted to expectations of reduced supply, preventing a price surge. Additionally, the availability of imported oranges from Mexico and South Africa helped stabilize supply levels, keeping prices under pressure.

Italy

In W6, Italy's orange prices dropped by 1.23% WoW and YoY to USD 1.60/kg due to weaker consumer demand for blood oranges and the shift in sales from mainstream retail to specialty stores and weekly markets, which have also been shrinking. Additionally, the early end of the Washington Navel season in late February has contributed to market uncertainty. However, MoM prices increased by 3.90% due to higher transportation costs and the continued premium pricing of Tarocco blood oranges, which remain in full supply but face declining consumption.

3. Actionable Recommendations

Expand Premium Market Presence

Sicilian orange producers should focus on promoting premium Tarocco blood oranges through specialty stores and direct-to-consumer channels by partnering with gourmet retailers, launching online sales platforms, and leveraging subscription-based fruit delivery services. Stronger branding and marketing—highlighting the fruit’s heritage and health benefits—can boost margins and offset declining retail sales.

Strengthen Premium Market Position

Brazilian juice exporters should focus on high-value markets by promoting premium orange juice products with differentiated quality and sustainability credentials. Strengthening branding, securing long-term contracts with key buyers in the European Union (EU) and the US, and leveraging limited supply to justify premium pricing can help maintain revenue growth despite lower export volumes.

Expand Value-Added Orange Exports

Greek orange exporters should differentiate their products by focusing on premium and value-added segments, such as organic or specialty varieties, to compete with lower-cost Egyptian oranges. Strengthening branding, targeting niche EU markets, and securing direct contracts with retailers can help sustain demand and profitability.

Sources: Tridge, Agropopular, Agrotypos, CEPEA, Freshplaza, Nepal Monitor, Sapros GmbH