In W12 in the sugar landscape, some of the most relevant trends included:

- The EC is considering further reducing Ukrainian sugar imports due to market price pressures, following a surge in Ukrainian exports after the 2022 duty suspension.

- EU sugar prices have declined in W12, resulting in losses for beet processors, with some companies closing plants. This may lead to reduced beet prices and planting area in 2025/26, contributing to a market deficit.

- India is set to begin the 2025/26 season with sufficient sugar stocks, despite lower-than-expected production and reduced exports, which may push prices higher.

- Indonesia has issued permits for sugar imports to address potential price fluctuations during the fasting month and Eid while balancing imports with domestic sugarcane harvests.

- Brazil's sugar prices rose in early 2025 due to climate uncertainties and a forecasted deficit in the 2024/25 harvest, potentially keeping prices high in the short term.

- Pakistan’s sugar prices surged due to water shortages affecting production, with the potential for tighter domestic supply and price increases if the situation persists.

1. Weekly News

European Union

EU Plans Further Cuts to Ukrainian Sugar Imports Amid Market Pressure

The European Commission (EC) plans to reduce Ukrainian sugar imports following complaints from European Union (EU) producers about market price declines. After the 2022 duty suspension, Ukraine’s sugar exports to the EU surged from 20,000 metric tons (mt) pre-war to over 500,000 mt in 2023/24. In Jul-24, a quota of 262,600 mt was reinstated, but further reductions are under consideration. EU farmers argue that Ukrainian sugar still pressures prices, despite limited February exports. With stricter quotas, Ukrainian producers are shifting exports to markets such as Türkiye and Libya, though the EU remains their preferred destination due to pricing and logistical advantages.

EU Sugar Price Decline in Jan-25 Pressured Beet Processors

In Jan-25, EU sugar prices continued to decline, reaching USD 602.65 (EUR 557/mt) ex-works (EXW), in line with the low prices agreed for the 2024/25 season. However, spot prices have recently rebounded above this level. The low prices have pressured EU beet processors, with companies like Sudzucker and Agrana reporting losses in Q4-2024, leading Agrana to close two plants in Austria and the Czech Republic. This financial strain is expected to reduce beet prices and planting area in 2025/26, with GlobalData forecasting a 7 to 8% reduction. As a result, the EU-United Kingdom (UK) market is projected to enter a deficit, which should support sugar prices in the coming season. Favorable weather conditions should allow timely planting, unlike the previous year.

China

China’s 2024 Sugar Imports Rose 9.41% YoY

China’s sugar imports totaled 4.35 million metric tons (mmt) in 2024, a 9.41% year-on-year (YoY) increase, despite a 21.29% YoY decline in Dec-24 imports to 391,500 mt. The total import value for the year reached USD 2.39 billion. Brazil remains the primary supplier, accounting for USD 2.06 billion, up 7.34% YoY. However, Dec-24 imports from Brazil fell 35.94% YoY. The decline in late-year imports may signal shifting trade patterns or fluctuating domestic demand, though overall annual growth suggests steady reliance on imports.

India

India to Enter 2025/26 Sugar Season with Stable Stocks Despite Lower Output and Exports

India is expected to enter the 2025/26 sugar season in Oct-25 with comfortable opening stocks despite lower-than-expected production and the approval of 1 mmt in exports. While industry estimates for the current season’s output have been revised downward, the Indian Sugar & Bio-Energy Manufacturers Association (ISMA) reassures that domestic supply will remain sufficient. Opening stocks are projected between 3.78 and 5.4 mmt, ensuring stability for early-season demand. However, traders anticipate price increases due to reduced output and high summer demand. Since sugar is a regulated commodity, the government continues to monitor prices and may intervene if necessary.

Indonesia

Indonesia Issues Import Permit for 200,000 MT of Raw Sugar to Stabilize Prices

Indonesia has issued an import permit for 200,000 mt of raw crystal sugar (Gula Kristal Mentah or GKM) from India and Brazil to strengthen food reserves and address potential sugar price fluctuations ahead of the 2025 fasting month and Eid. The Ministry of Trade confirmed that the import process is ongoing, with domestic sugar absorption from local farmers also being prioritized. The National Food Agency (Bapanas) assured that the price of sugar from domestic farmers will be maintained at USD 0.87 per kilogram (IDR 14,500/kg) to prevent price drops. The government aims to balance imports with local sugarcane harvests expected in Apr-25 and May-25.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W12 2024 to W12 2025)

Brazil

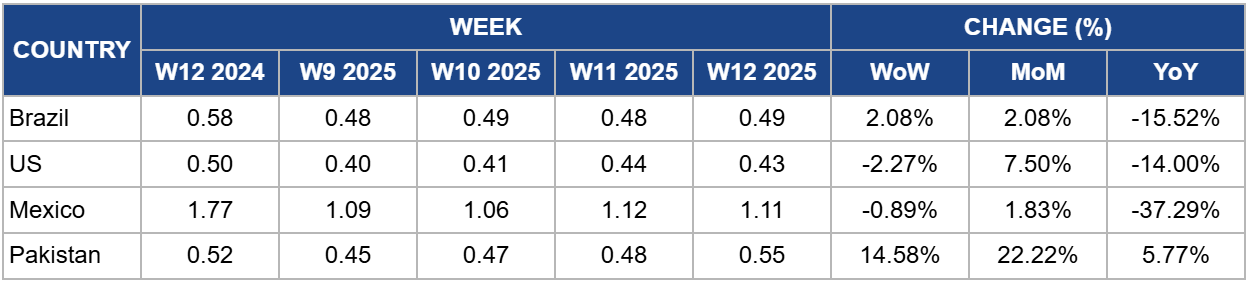

Brazil's sugar prices rose to USD 0.49/kg in W12, reflecting a 2.08% rise both week-on-week (WoW) and month-on-month (MoM). The recent price increase is supported by expectations of a 4.1 mmt deficit in the 2024/25 harvest, coupled with climate uncertainties such as rainfall in the last months of 2024 being well above the historical average, and rainfall at the beginning of 2025 being below the average. Despite forecasts of a surplus in 2025/26, reduced rainfall and ongoing field renovations may limit output, maintaining upward pressure on prices. However, if global sugar prices fall below USD 0.1850 per pound (lb), mills may shift more cane to ethanol production, potentially tightening the sugar supply and supporting prices in the short term. Future price movements will depend on rainfall in Mar-25 and Apr-25 and global market trends.

United States

In W12, the United States (US) sugar prices dropped to USD 0.43/kg, a 2.27% weekly decrease and a 14% YoY decline. The lifting of export restrictions on Central Romana Corporation, the Dominican Republic’s largest sugar producer, is expected to increase US sugar supply. This could stabilize or further reduce prices, depending on the volume of sugar reintroduced to the market.

Mexico

Mexico's sugar prices fell to USD 1.11/kg in W12, down 0.89% WoW and 37.29% YoY, reflecting weakened demand and trade disruptions. Years of drought have constrained production, while proposed US tariffs further threaten exports. Anticipation of the 25% tariff spurred early shipments to the US, but future flows have now stalled, limiting Mexico's market access. With reduced exports and falling demand, domestic sugar prices may remain under pressure in the short term. However, lower production levels in 2025 could tighten supply, potentially stabilizing or increasing prices if domestic consumption strengthens.

Pakistan

In W12, Pakistan's sugar prices rose to USD 0.55/kg, experiencing a sharp 14.58% WoW and 22.22% MoM increase, driven by concerns over water shortages affecting key agricultural regions. The Indus River System Authority (IRSA) warns that declining water levels in Mangla and Tarbela Dams could severely impact sugarcane production, particularly in Sindh. Reduced irrigation availability may lower future yields, further tightening domestic supply and sustaining price increases. If the crisis persists, Pakistan may face heightened inflationary pressure in the sugar market, prompting potential government intervention through price controls or increased imports.

3. Actionable Recommendations

Strengthen Import Diversification and Logistics in Response to EU Quota Reductions

As the EC considers reducing Ukrainian sugar imports, EU producers facing price pressures should explore alternative sources from non-EU countries. Expanding sugar imports from markets such as Brazil, India, and Türkiye could help offset the tightening of Ukrainian supplies. Governments and trade organizations can support this shift by negotiating trade agreements and ensuring logistical infrastructure is in place to facilitate smooth and efficient supply chains. Additionally, diversifying sourcing strategies will reduce the risk of over-reliance on any single exporter and mitigate future price volatility.

Capitalize on Short-Term Price Movements to Stabilize Domestic Markets

With sugar prices fluctuating globally—especially in Brazil, Mexico, and Pakistan—industry stakeholders, including traders and processors, should strategically time their purchases to benefit from short-term price rebounds. Importers can secure supplies during price dips while maintaining a close watch on climate forecasts and production reports to anticipate future price trends.

Invest in Strategic Storage and Export Planning Amid Production Challenges

Given the projected sugar deficits in key regions like the EU and Brazil and the reduced domestic output in India, sugar producers should invest in robust storage infrastructure to manage supply disruptions. This will allow for more strategic export timing, reducing the risk of oversupply and price crashes. Countries like Mexico and Pakistan facing domestic production challenges could benefit from public-private partnerships to enhance local storage capacities and strengthen export pipelines to emerging markets such as Southeast Asia, where growing demand offers potential for price stabilization.

Sources: Tridge, Canal Rural, Hellenic Shipping News, UkrAgroConsult, Agravery, News Foodmate, Republika