.jpg)

In W16 in the palm oil landscape, some of the most relevant trends included:

- Rising US-China trade tensions may increase global palm oil demand as China substitutes soybean imports with palm oil. However, broader demand uncertainties, such as US tariffs and falling crude oil prices, could limit price gains.

- Colombia's palm oil sector grew significantly in Q1-2025, with production and exports up due to favorable weather conditions. Domestic consumption remains strong, with a large portion used for edible oils and biodiesel.

- Indonesian palm oil producers face challenges due to a 32% US tariff on exports, pushing them to seek new markets in Africa, the Middle East, and Eastern Europe. Ongoing trade uncertainty has led to calls for reduced export duties.

- Malaysia maintains a 10% CPO export tax for May-25, impacting global pricing and regional export competitiveness, with adjustments in the reference price to reflect market conditions.

1. Weekly News

China

US-China Trade Tensions Drive China Toward Palm Oil

Rising United States (US)-China trade tensions may prompt China to substitute soybean imports with palm oil, potentially boosting global palm oil demand. However, Hong Leong Investment Bank (HLIB) Research cautions that this upside could be tempered by broader demand uncertainties tied to US tariffs and declining crude oil prices. While China has already reduced US soybean imports and increased palm oil purchases—up 5% to 5.3 million metric tons (mmt) in 2018—HLIB expects only minimal impact on US palm oil demand. In 2024, US palm oil demand totaled 1.8 mmt, largely sourced from Indonesia. With supply recovering, crude palm oil (CPO) price gains may remain limited, with 2025/2026 forecasts at USD 865.41 per metric ton (mt).

Colombia

Colombia's Palm Oil Output Rises 11.3% YoY in Q1-2025

Colombia's palm oil sector recorded strong growth in Q1-2025, with production rising 11.3% year-on-year (YoY) to 450,000 mt, according to the National Federation of Oil Palm Growers (Fedepalma). Driven by favorable weather conditions, particularly steady rainfall that supported fruit bunch development, production output rose to 203,000 mt in Mar-25, an increase of 24.1% YoY.The Eastern and Central regions led production with 264,000 mt and 178,000 mt, respectively, while the Northern region showed a 20.9% recovery in Mar-25.

Palm oil trade also improved, with total Q1-2025 sales up 4.4% YoY to 489,000 mt. Export volumes rose 16,000 mt to 155,000 mt, now representing 30–32% of total sales. Domestic consumption reached 334,000 mt (+1.3%), with 50% used for edible oils and fats and 45% for biodiesel production.

Indonesia

Indonesia Accelerates Palm Oil Market Diversification Amid US Tariff Uncertainty

Indonesian palm oil producers are diversifying export markets amid rising trade tensions with the US, which recently imposed a 32% tariff on palm oil. Although a temporary 90-day suspension was announced, industry leaders, including the Indonesian Palm Oil Producers Association (GAPKI), emphasize the need to mitigate future risks by targeting new markets in Africa, particularly Egypt, as well as the Middle East, Central Asia, and Eastern Europe. The US has become a growing market, with imports from Indonesia rising from 1.5 mmt in 2020 to 2.5 mmt in 2023, but ongoing uncertainty is prompting a strategic shift to diversify and stabilize exports.

Indonesian Palm Oil Producers Call for Duty Cuts to Stay Competitive Due to US Tariff Pressure

Indonesian palm oil producers are urging the government to reduce export duties on US-bound shipments to remain competitive following the imposition of a 32% tariff by the US. Although the tariff was temporarily suspended for 90 days, a baseline 10% levy remains in place. GAPKI highlights the cost burden producers face, including domestic market obligations, export levies, and duties—totaling around USD 221/mt, compared to USD 140/mt for Malaysian exporters. With the US accounting for 14.8% of Indonesia's refined palm oil exports, concerns are rising over potential market losses to Malaysia and emerging Latin American producers. Indonesia exported 2.2 mmt of palm oil to the US in 2024, down from 2.5 mmt in 2023.

Malaysia

Malaysia Keeps May CPO Export Tax at 10%

Malaysia will maintain its CPO export tax at 10% for May-25, while lowering the reference price to USD 1,008.47/mt (MYR 4,449.35/mt), down from USD 1035.71/mt (MYR 4,547.79/mt) in Apr-25, according to the Malaysian Palm Oil Board (MPOB). Under Malaysia's tax structure, the maximum 10% rate applies when prices exceed USD 922.34/mt (MYR 4,050/mt). As the world’s second-largest palm oil exporter, Malaysia's tax decisions play a key role in shaping regional export competitiveness.

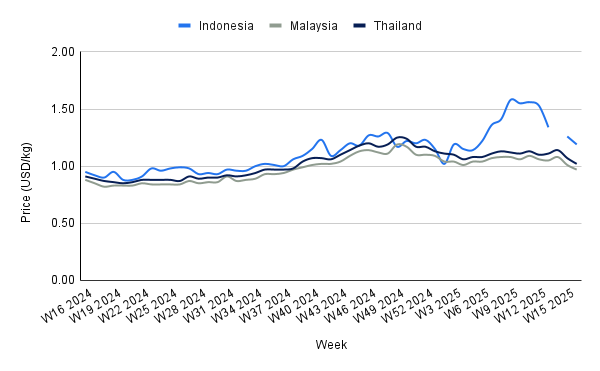

2. Weekly Pricing

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W16 2024 to W16 2025)

Indonesia

In W16, Indonesia's palm oil prices declined to USD 1.19 per kilogram (kg), a 5.56% week-on-week (WoW) drop, though still 25.26% higher YoY. The recent price pressure reflects expectations of increased supply, with the United States Department of Agriculture (USDA) projecting 2025/26 production to rise to 47 mmt, up 1.5 mmt from the previous season, driven by favorable weather and improved yields.

While domestic demand is also forecast to grow slightly, particularly from the national biodiesel mandate (B40), the resulting supply growth is expected to weigh on prices in the near term. Exports are projected to rise by 1 mmt to 24 mmt, primarily to China, India, and Pakistan, but global oversupply risks remain. Meanwhile, rising trade tensions with the US are prompting Indonesian producers to diversify markets beyond North America. Despite these efforts, the combination of higher production, marginally rising stocks, and export uncertainty could exert downward pressure on prices throughout 2025, unless demand strengthens meaningfully in non-traditional markets.

Malaysia

Malaysia’s palm oil prices fell to USD 0.97/kg in W16, down 3.96% WoW, despite remaining 10.23% higher YoY. The recent decline is primarily attributed to expectations of improved production in both Malaysia and Indonesia. Data from the MPOB show that Malaysia's CPO output rose by 16.76% in Mar-25 compared to Feb-25, while exports grew by just 1%. This imbalance has contributed to downward price pressure, including a 7.62% month-on-month (MoM) decrease from USD 1.05/kg. Although exports improved by 13.55% in the first half of Apr-25, reaching 450.7 thousand mt, the supply-side increase continues to outweigh demand growth.

If production continues to rise while export growth remains modest, further price corrections may follow. However, seasonal demand factors and shifts in global vegetable oil markets could provide some support and help stabilize prices in the medium term.

Thailand

In W16, Thailand's palm oil prices fell to USD 1.02/kg, marking a 4.67% weekly decline. This drop is linked to broader economic uncertainties, particularly regarding potential US tariffs on Thai exports, including a proposed 36% duty. Additionally, increased palm oil production, boosted by recovery from El Niño conditions, could further exert downward pressure on prices if demand does not grow correspondingly. If these factors persist, Thailand may face challenges in maintaining competitive pricing, potentially influencing both domestic and global market dynamics. Rising production without matching demand could lead to sustained price volatility in the short term.

3. Actionable Recommendations

Diversify Export Markets to Mitigate Tariff Risks

Given the rising trade tensions and the potential impact of tariffs, Indonesian palm oil producers should accelerate efforts to diversify their export markets beyond the US. Targeting regions such as Africa, the Middle East, and Eastern Europe, through trade agreements and tailored marketing strategies, will help stabilize revenues and reduce vulnerability to trade disputes and tariff escalations.

Implement Cost Reduction Measures to Enhance Competitiveness

To remain competitive amidst rising export duties and tariffs, Indonesian authorities should focus on reducing export costs, specifically targeting a reduction in the 10% export levy for US-bound shipments. This could involve revisiting export tax structures and providing direct financial support to producers, enabling them to maintain competitive pricing and prevent market share losses to Malaysia and emerging Latin American producers.

Invest in Value-Added Palm Oil Products for Market Resilience

Palm oil producers in Southeast Asia should consider investing in value-added products such as oleochemicals, biodiesel, and specialty fats to reduce dependency on crude palm oil exports. This would allow producers to capture higher margins, cater to niche markets, and mitigate the impacts of price fluctuations while aligning with increasing global demand for sustainable and eco-friendly products.

Sources: Tridge, Ukr AgroConsult, Grain Trade, Caracol, Alberta Farmer