In W17 in the grape landscape, some of the most relevant trends included:

- Global vineyard area continues to decline, especially in major wine-producing regions such as Spain, France, and Italy, while countries like Russia and India are seeing slight growth. Climate change and shifting market demands are contributing to this trend.

- Argentina's grape production has increased by 7.5% YoY, with vineyards focusing on varieties suited for the growing demand for low- and no-alcohol wines, despite challenges like rising input costs and pests.

- Egypt is preparing for a strong export season with high-quality grapes and new varieties targeting the Far East market, though competition from China’s early harvest may put pressure on pricing, especially in Asian markets.

- In Spain, favorable weather conditions have improved vineyard health following years of drought, but there is a rising risk of fungal diseases. To address market imbalances, Spanish agricultural authorities have introduced green harvest aid to help manage oversupply and stabilize the market, particularly benefiting small family-run vineyards.

1. Weekly News

Global

Global Vineyard Area Continues to Decline

The International Organisation of Vine and Wine (OIV) reported a 0.6% year-on-year (YoY) decline in the global vineyard area in 2024. The total area now stands at 7.1 million hectares (ha). This marks the fourth consecutive year of decrease. In the European Union (EU), which holds nearly half of the world's vineyards, the area decreased by 0.8% YoY. Spain saw a 1.5% drop to 930 thousand ha, France experienced a 0.7% decrease to 783 thousand ha, and Italy had a 0.8% increase to 728 thousand ha. Beyond the EU, Moldova's vineyard area remained stable at 115 thousand ha, while Russia’s expanded by 2.2% to 108 thousand ha. In Asia, China's vineyard area remained steady at 753 thousand ha, India’s grew by 1.8% to 185 thousand ha, and Türkiye’s continued its long-term decline with a reduction of 1%. North America saw a reduction in vineyard area, particularly in the United States (US), marking the eleventh consecutive year of decline. South America saw declines in Argentina and Chile, with Brazil reporting growth. South Africa, the continent's major grape producer, saw a 1.5% reduction to 120 thousand ha. Australia maintained stable levels at 159 thousand ha. This has highlighted the need for international cooperation to address the impacts of climate change and changing market conditions in the grape industry.

Argentina

Argentina's Grape Production Rises 7.5% YoY in 2025

According to the National Institute of Viticulture (INV), Argentina’s 2025 grape production has risen by 7.5% YoY. Wineries received over 16.4 million quintals of grapes by the end of Mar-25, continuing the positive trend from 2024. Unlike previous years, which were plagued by severe hail damage, the 2025 season saw minimal weather-related losses, although localized pest and fungi issues affected some vineyards in Lavalle. While eased export restrictions and a stronger dollar have enhanced the competitiveness of grape growers, rising input costs present a new challenge. Additionally, Lavalle's significant cultivation of varieties like Tempranillo, Torrontés, and Bonarda positions it well to benefit from the growing global demand for low- and no-alcohol wines, a market expected to expand steadily through 2027, driven by health-conscious consumer preferences and regulatory shifts in key markets such as the United Kingdome (UK). However, producing these wines may pose challenges, particularly in Lavalle’s warm climate, which naturally results in grapes with high sugar content and, consequently, higher alcohol levels. Reducing alcohol content without compromising flavor and quality requires investment in specialized technology and expertise, making the adaptation process complex. Nevertheless, Lavalle's diverse grape portfolio offers promising opportunities to meet shifting global tastes.

Egypt

Egyptian Grape Exports Poised for Strong 2025 Start Despite Market Competition

Egypt is preparing for its grape export season, expecting higher volumes and good fruit quality due to favorable weather during flowering. The harvest of early varieties, including Prime, Flame, and Starlight, will begin in early May, reaching full capacity by May 20, 2025. This season also marks the first export of new varieties like Ivory, Timson, Allison, Firestar, and Autumn Pearl, which are primarily aimed at the growing Far East market. Initial exports will target Europe, where prices are expected to remain high and stable through mid-June before declining as European harvests begin. Later shipments will shift toward the Far East, where prices are more stable but lower. However, Egypt faces strong competition from China, which is experiencing an early and high grape harvest, potentially putting downward pressure on prices in Asian markets.

Spain

Favorable Conditions Boost Grape Prospects in Spain Despite Market Challenges.

In Spain, autumn and winter rains have revitalized vineyards, and spring rainfall is promoting strong vine budding, particularly in Castilla-La Mancha, the country’s leading grape-growing region. This recovery follows years of drought, with varieties like Airén showing healthy development. While growers benefit from the increased rainfall, it also increases the risk of fungal diseases like powdery and downy mildew, urging vigilance with preventive treatments. On the market side, grape prices remain relatively high, driven by strong demand for white wines and a gradual recovery in reds. However, recent uncertainties surrounding global tariffs have caused a temporary slowdown. Wineries and cooperatives in the region are nearly out of stock heading into the next season. They remain optimistic despite concerns over declining global wine consumption, even as local consumption in Spain shows slight improvement.

South Africa

South African Grapes Lead German Market Despite Quality Concerns and Rising Prices

In Germany, South African grapes, particularly the red Crimson Seedless variety, dominated the market, followed by Chilean shipments, with Peruvian and Indian supplies serving as additional sources. A broad range of grape varieties led to significant price variations. While demand remained favorable and prices trended upward, quality inconsistencies were noted, especially with Chilean grapes in Frankfurt. Higher initial asking prices increased costs for buyers, particularly for South African grapes. Additionally, returns from food retailers, driven by declining organoleptic properties, further complicated the sale of regular goods.

Spain Offers Green Harvest Aid to Support Grape Growers in Castile and León

Self-employed winegrowers in Castile and León can now apply for green harvest aid for the 2025 grape harvest. This measure is designed to stabilize the market by reducing excess grape production. This is part of the extended 2019/23 Wine Sector Support Program, which offers financial compensation covering up to 50% of the costs for early grape bunch removal and income loss from unsold grapes. To qualify, vineyards must be registered in Registro de Explotaciones Agrarias de Castilla y León (REACYL), planted before August 1, 2021, and cover at least 0.15 ha.

Applicants with past non-compliance or sanctions are excluded. Applications are submitted online via the Regional Government's website, requiring documents like Sistema de Información Geográfica de Parcelas Agrícolas (SIGPAC) maps and vineyard declarations, with the green harvest to be completed before July 15, 2025. Preference will be given to plots under protected designations of origin (PDO), young farmers, and active farmers if the budget limit is exceeded. This aid aims to support small, family-run vineyards, which are essential to rural economies. It helps them avoid the financial challenges of oversupply and falling grape prices.

2. Weekly Pricing

Weekly Grape Pricing Important Exporters (USD/kg)

Yearly Change in Grape Pricing Important Exporters (W17 2024 to W17 2025)

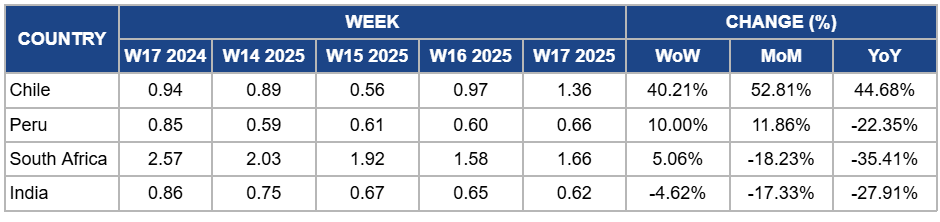

Chile

In W17, Chile's grape prices surged by 40.21% WoW to USD 1.36/kg, marking a 52.81% MoM increase and a 44.68% YoY rise. This significant price hike is partly due to a slight delay in the harvest in central and southern regions caused by cooler spring temperatures, alongside a strategic shift toward later-maturing grape varieties to avoid overlap with Peru’s earlier season. These factors, combined with strong demand from key export markets, particularly the US, contributed to a temporary supply gap and supported higher prices. Additionally, the implementation of the Systems Approach in Chile’s grape-growing regions has enhanced fruit quality and export efficiency, further driving price gains.

Peru

Grape prices in Peru rose by 10% WoW to USD 0.66/kg in W17, with an 11.86% MoM increase due to favorable weather conditions, such as mild temperatures during flowering and fruit set, adequate rainfall followed by dry periods to prevent rot, and minimal extreme weather events like frost or excessive heat. These conditions enhanced the quality and spurred strong demand in key export markets. However, YoY prices dropped by 22.35% due to a higher supply this season compared to last year, leading to a price adjustment. This oversupply, combined with demand from international buyers shifting towards more cost-effective alternatives, pressured prices downward.

South Africa

South Africa's grape prices increased by 5.06% WoW to USD 1.66/kg in W17 due to strong demand in key markets, particularly in Europe, where South African grapes continued to dominate the market, alongside favorable weather conditions that improved harvest quality. However, MoM and YoY prices decreased by 18.23% MoM and 35.41% YoY due to oversupply from earlier shipments, which led to a price correction, and quality inconsistencies were observed in certain batches, especially in markets like Frankfurt. This resulted in reduced buyer confidence and lower prices, despite the initial high asking prices.

India

In India, grape prices fell by 4.62% WoW to USD 0.62/kg in W17, with a 17.33% MoM drop and a 27.91% YoY decrease. The price decline is due to an oversupply of grapes from the current harvest, as production volumes increased significantly. This surge in output was driven by favorable weather conditions, improved farming practices, and an expansion in planted areas, especially in key producing regions like Maharashtra, following strong price trends in previous years. Additionally, lower demand from local and export markets, particularly amidst ongoing logistical challenges and fluctuating quality, contributed to the price drop. The weakening demand from key export destinations also pressured prices further.

3. Actionable Recommendations

Optimize Export Timing to Maximize Grape Profits

Egyptian grape exporters should prioritize early shipments to Europe, capitalizing on the high prices before local European harvests flood the market. To counteract competition from China in the Far East, exporters should focus on promoting the new grape varieties, Ivory, Timson, Allison, Firestar, and Autumn Pearl, emphasizing their unique qualities and premium pricing. Strategic marketing campaigns targeting the Far East market should be planned to align with shipment schedules, ensuring steady demand even with lower price expectations.

Improve Quality Control for Consistent Grape Sales

South African grape exporters should implement stricter quality control measures to maintain consistency across shipments, particularly for the red Crimson Seedless variety, to avoid price volatility and returns. Chilean exporters need to focus on improving grape quality, especially in markets like Frankfurt, where inconsistencies have affected buyer confidence. South African and Chilean exporters should also align pricing strategies more closely with the market demand to prevent high initial costs from deterring retailers. Expanding supply chain visibility and implementing better post-harvest handling techniques will ensure higher quality and reduce returns.

Sources: Tridge, Autonomosyemprendedor, Despertadorlavalle, Freshplaza, Larazon, Noticiaspiura30, Vinetur