In W18 in the avocado landscape, some of the most relevant trends included:

- Global avocado demand is driving production expansion, infrastructure investment, and new market access efforts, with Guatemala targeting the US, Peru recovering and diversifying exports, and the Netherlands reinforcing its position as a key European hub.

- Climate impacts and shifting farmer preferences are tightening supply and driving up prices, as seen in Mexico due to forest fires and in Vietnam due to poor yields and crop substitution.

- Sustainability and regulatory compliance are increasingly prioritized, with Peru upgrading irrigation and post-harvest practices, Guatemala addressing pest control and environmental standards, and Mexico enforcing anti-deforestation measures.

- Export growth is supported by improved logistics and supply chain investments, such as Guatemala’s new packing facility, Peru’s focus on export quality, and the Netherlands’ efficient re-export operations.

1. Weekly News

Guatemala

Guatemala Targets US Market with Avocado Industry Expansion

Guatemala's avocado industry is preparing for expansion, targeting the United States (US) market after receiving export approval six months ago. Although exports have not yet begun, Guatemala plans to capitalize on its proximity to the US and its experience in European exports. Currently, 7 thousand hectares (ha) are dedicated to avocado cultivation, with projections to expand to 30.35 thousand ha within the next decade. The agricultural ministry estimates an initial export volume of 1.7 thousand metric tons (mt) to the US, potentially reaching 15 thousand mt by 2030, though a new 10% US tariff on imports may impact these projections. A new packing facility by Mission Produce, one of the world’s largest avocado distributors with an extensive global supply chain and retail network, is expected to open in August 2025. However, final US approval for export protocols is still pending, as shipments must be certified as pest-free by inspectors. Despite these challenges, Guatemala may benefit from disruptions in Mexico’s avocado industry, but Guatemala’s growth will depend on addressing security, environmental concerns, and sustainable farming practices.

Mexico

Avocado Prices to Rise in Nayarit Due to Forest Fires

Forest fires in Nayarit, Mexico, have ravaged over 1 thousand ha of avocado crops, causing a significant price increase this year. The fires have severely impacted production, reducing supply, while producers with unaffected crops may benefit from higher prices. The state, which has faced recurring fires in recent years, saw this blaze spread uncontrollably, destroying thousands of mature trees. As a result, local and national avocado prices are expected to rise, affecting families and businesses that rely on the fruit. However, producers with ready-to-harvest crops will see market advantages due to the decreased supply. Government and environmental agencies are implementing targeted support for affected farmers while introducing stricter measures to reduce deforestation, a key driver of these recurring fires.

Netherlands

The Netherlands Emerges as Europe's Avocado Hub, Driving Import Growth and Regional Exports

The Netherlands is a key player in the global avocado trade, serving as Europe's main entry point for avocados from overseas. Over the past five years, avocado imports to the country have increased by 25%, reaching over 500 million kilograms (kg), with the value rising by 50% to USD 1.92 billion (EUR 1.7 billion). Peru remains the dominant supplier, although imports from Colombia, South Africa, Kenya, and Morocco are also growing rapidly, with 75% of South Africa's avocado exports heading to the Netherlands. In addition to importing, the Netherlands serves as a key supplier of avocados across Europe, with 84% of Germany's avocado imports coming from the country. Dutch avocado exports are primarily directed to Germany, France, and Spain. The avocado market in the Netherlands is particularly popular among young consumers, while pensioners make up a smaller portion of household purchases.

Peru

Peru's Hass Avocado Industry Expected to Experience Strong Recovery in 2025

Peru's Hass avocado industry is expected to experience a strong recovery in 2025 after a difficult 2024 season marked by extreme weather and logistical challenges. Exports are expected to rise by 37% year-on-year (YoY), following three years of stagnation. Despite reduced fruit yields due to high temperatures and insufficient cold hours, the industry has focused on improving irrigation technology and enhancing post-harvest practices. Additionally, strengthening collaboration between the public and private sectors has helped stabilize exports. While Europe, the US, and Chile remain the top markets for Peruvian Hass avocados, emerging Asian markets like China and Japan are becoming increasingly important for future growth. As global demand for Hass avocados continues to rise, Peru is also prioritizing the improvement of export quality, particularly in terms of dry matter content. With 77 thousand ha under cultivation, Peru's avocado industry is maturing, making 2025 a crucial year for growth in both volume and value.

Vietnam

Vietnam’s Avocado Prices Surge Due to Supply Shortage

Avocado prices in Vietnam have surged to their highest level in five years, reaching USD 1.54/kg (VND 40,000/kg). This represents a doubling from the previous year, driven by a significant supply shortage. The Central Highlands province of Lâm Đồng, a key avocado-growing region, has seen a 50% YoY drop in supply, driven by poor yields and unfavorable weather conditions. Faced with years of low profits, many farmers have turned to more lucrative crops like durian and coffee, leading to a decline in avocado cultivation. As a result, retailers in Ho Chi Minh City have raised avocado prices, making them more expensive than other fruits such as mangoes and oranges. To assure customers of quality, some supermarkets are promoting avocados with a green sticker to highlight their chemical-free status. Lâm Đồng typically produces around 80 thousand tons of avocados annually, but the area dedicated to avocado farming has been shrinking as farmers shift to more profitable alternatives.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

Yearly Change in Avocado Pricing Important Exporters (W18 2024 to W18 2025)

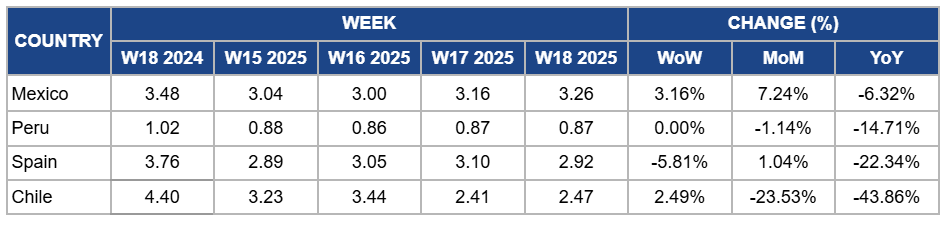

Mexico

In W18, Mexico's avocado prices increased by 3.16% week-on-week (WoW) to USD 3.26/kg, with a 7.24% month-on-month (MoM) rise driven by reduced supply following forest fires in Nayarit that destroyed avocado orchards, tightening availability and pushing prices upward. However, there is a 6.32% YoY drop due to the appreciation of the Mexican peso, which has made exports more expensive and less competitive in international markets, leading to decreased demand and contributing to the YoY price decline.

Peru

Peruvian avocado prices remained steady WoW at USD 0.87/kg in W18 as exporters maintained stable pricing strategies amid a recovering supply chain and consistent demand. However, prices declined by 1.14% MoM and 14.71% YoY, primarily due to intensified competition in European markets from countries such as Spain, Israel, and Morocco. This external pressure offset the expected upward price impact from reduced domestic production, which was affected by extreme heat and insufficient cold hours during the 2024 season, leading to lower yields and smaller fruit sizes, especially in the key northern coastal regions. In response, Peruvian exporters diversified their market focus by increasing shipments to Asia, including China, Japan, and South Korea. Despite current challenges, the industry expects a strong rebound in 2025, with export volumes projected to rise by 37%, supported by improved irrigation systems, better post-harvest handling, and the maturation of young plantations.

Spain

Spain's avocado prices dropped by 5.81% WoW to USD 2.92/kg in W18, with a 22.34% YoY decrease. The price decrease is due to higher-than-usual supply from improved weather conditions and favorable harvests, which increased production. However, MoM prices increased by 1.04% due to stronger demand in European markets, which have absorbed the available supply despite the increase in volume.

Chile

Chile’s avocado prices rose by 2.49% WoW to USD 2.47/kg in W18, likely due to a temporary tightening of supply following the end of the peak harvest season in May-25, which reduced availability in local and export markets. However, on a broader scale, prices fell by 23.53% MoM and 43.86% YoY. This decline was primarily driven by a 33% increase in production for the 2024/25 season, resulting from favorable climatic conditions and abundant rainfall. The resulting oversupply has exerted sustained downward pressure on prices. Additionally, intensified competition in key export markets such as Europe and the US, particularly from major producers like Peru and Mexico, has further contributed to the longer-term price decline.

3. Actionable Recommendations

Rebuild Supply Through Targeted Avocado Replanting

Avocado growers in Lâm Đồng should selectively replant high-yield, weather-resilient avocado varieties in abandoned or mixed-crop plots to recover the declining supply. Farmers can interplant avocados with durian or coffee to maximize land use while diversifying income. By focusing on premium, chemical-free varieties that meet supermarket standards, such as those already tagged with green stickers, producers can tap into rising consumer demand and restore long-term profitability.

Diversify Sourcing to Strengthen Supply Resilience

Dutch avocado importers should expand sourcing from emerging suppliers like Kenya and Morocco to reduce dependence on Peru and maintain consistent year-round availability. By building stronger supply chains with these alternative origins and investing in ripening and quality control infrastructure for newer sources, importers can better manage seasonal gaps and shipping disruptions. For example, trial contracts with Moroccan growers during Peru’s off-season or volume ramp-ups from Kenya during peak demand can help stabilize supply and protect margins.

Sources: Tridge, ABC News, Freshfruitportal, Freshplaza, Gobierno de Mexico, GroentenFruit Huis, Meganoticias, Vnexpress