In W18 in the maize landscape, some of the most relevant trends included:

- The EU's corn imports increased by 12% YoY in the 2024/25 season, with a notable rise in shipments from the US, now accounting for 21% of the EU's corn imports. This increase helped offset declines from Ukraine and Brazil, the EU's top suppliers.

- Meanwhile, Argentina's corn harvest is progressing slowly, with only 30% harvested by mid-April. However, favorable weather conditions will accelerate progress, potentially boosting yield prospects and supporting prices.

- On the other hand, Ukraine's corn exports have fallen by 18.5% YoY in the 2024/25 season. Despite this, Ukrainian corn prices surged by 60% YoY in Apr-25, driven by reduced global supply and a weakened hryvnia, making Ukrainian maize more competitive in the global market.

1. Weekly News

Europe

EU Corn Imports Up 12% YoY in 2024/25 as US Shipments Surged

As of April 20, 2025, the European Union (EU) imported 16.76 million metric tons (mmt) of corn in the 2024/25 season (July to June), marking a 12% year-on-year (YoY) increase. This growth was due to a surge in corn imports from the United States (US), which supplied 3.52 mmt, nearly 30 times more than the 114 thousand metric tons (mt) shipped during the same period last year, raising its share of EU imports from 0.8% to 21.0%. Meanwhile, imports from Ukraine, the EU’s top supplier, declined from 10.09 mmt in the 2023/24 season to 9.54 mmt in the 2024/25 season, reducing its share from 67.6% to 56.9%. Brazil, the third-largest supplier, saw exports to the EU fall from 2.81 mmt to 1.62 mmt, lowering its market share from 18.8% to 9.7%. In contrast, imports from Canada rose from 660 thousand mt to 1.11 mmt, increasing its share from 4.4% to 6.6%. Overall, the sharp rise in US shipments effectively offset the declines from Ukraine and Brazil, supporting the EU’s growing corn demand.

Argentina

Argentina's Coarse Grain Harvest Progressing Steadily with Favorable Weather Conditions

Argentina’s coarse grain harvest is progressing slowly but steadily, aided by stable weather conditions. Dry weather will continue across the core region through W19, facilitating fieldwork. As of W18, only 30% of the corn has been harvested, but the forecasted low humidity levels will help accelerate the process. Temperatures are expected to rise midweek, with highs reaching 24 to 28°C by the weekend in areas like Pergamino, slightly above seasonal averages.

Paraguay

Paraguay Corn Use Hits Record on Ethanol Boom, Exports Set to Drop

Paraguay will reduce corn exports by 12% YoY to 2.9 mmt in the 2025/26 marketing year (MY) as rising domestic demand, driven primarily by the expanding ethanol industry and animal feed sector, tightens exportable supplies. Domestic consumers will push corn consumption to a record 2.4 mmt, with the ethanol sector alone using 1.5 mmt. Two large-scale ethanol plants operate at full capacity, while engineers expect a third plant, now under refurbishment, to resume operations by mid-2025. Once operational, the facility will consume between 420 thousand and 450 thousand mt of corn annually starting in 2026. However, ethanol producers may curb future corn demand by incorporating sorghum as a partial substitute, attracted by its drought resilience and lower production costs despite lower yields and prices than corn. Farmers will maintain corn production at 5.2 mmt for the 2025/26 season.

Ukraine

Ukraine Corn Exports Down 18.5% YoY to 18.34 MMT in 2024/25

As of April 28, Ukraine exported 18.343 mmt of MY 2024/25 corn, reflecting a decline of over 4.1 mmt or 18.5% compared to last year. In Apr-25 alone, corn exports totaled 1.366 mmt.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W18 2024 to W18 2025)

United States

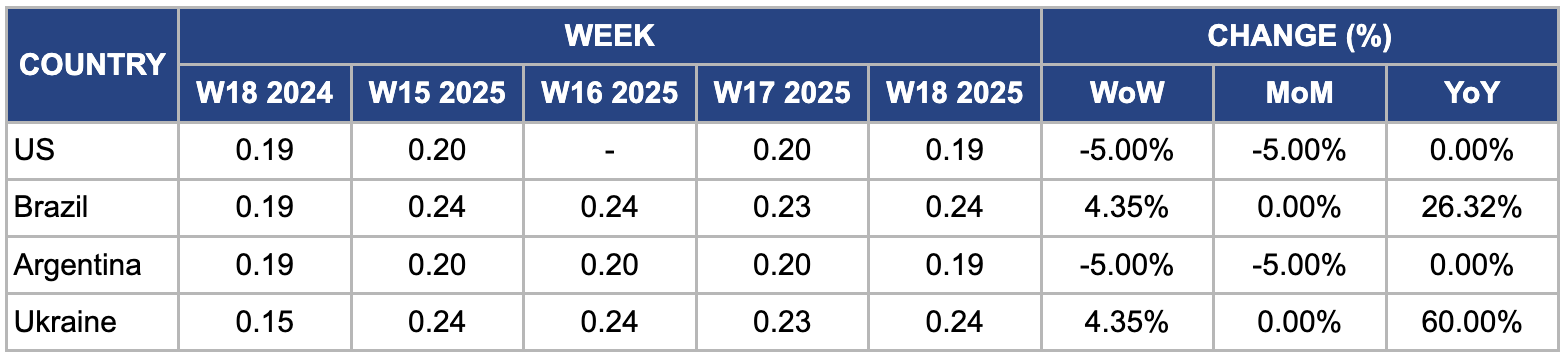

In W18, US corn prices reached USD 0.19 per kilogram (kg), representing a 5% week-on-week (WoW) and month-on-month (MoM) decline. This decline was mainly due to favorable weather conditions across key corn-producing areas, such as the Midwest, which improved crop conditions and boosted planting progress, alleviating supply concerns. As a result, the outlook for the upcoming corn harvest became more positive, leading to a price drop. Moreover, the strengthening US dollar made US corn less competitive on the global market, reducing demand from international buyers. Furthermore, improved harvest expectations in major exporting countries like Brazil and Argentina, where weather conditions supported better production prospects, contributed to the overall downward pressure on US corn prices.

Brazil

In W18, Brazil's wholesale maize prices increased 4.35% WoW to USD 0.24/kg. The price rise is primarily due to firm domestic demand from the livestock and ethanol industries, alongside slow farmer selling as producers hold onto stocks in anticipation of better prices. Moreover, concerns over the 2024/25 second (safrinha) corn crop, particularly in key producing states like Mato Grosso and Paraná, have supported prices. Recent dryness in some regions has raised fears of potential yield reductions, prompting market participants to price in future supply risks. Despite ongoing harvest activities in early areas, overall supply availability remains tight, which has added to the upward price momentum.

Argentina

In W18, Argentine maize prices declined by 5% WoW and MoM, reaching USD 0.19/kg. This decline was primarily due to recent improvements in weather conditions across key growing regions such as Buenos Aires, Entre Ríos, and Santa Fe. These areas received significant rainfall, which helped alleviate some of the supply concerns that had previously put upward pressure on prices. The improved weather contributed to better crop yields and reduced fears of prolonged drought conditions, offering a more optimistic outlook for the upcoming maize harvest. Furthermore, increased competition from other major maize-producing countries like Brazil and the US further pressured the market, as their larger harvests offered more competitive pricing.

Ukraine

In W18, Ukrainian wholesale maize prices increased by 4.35% WoW and 60% YoY, reaching USD 0.24/kg. This price surge is due to several key factors, including reduced global maize availability and ongoing challenges in Ukraine's domestic supply chain. Ukraine's 2025 maize harvest is estimated to be lower, while the country has maintained high export demand, particularly from the EU, due to the global supply shortage exacerbated by production issues in other major maize-producing regions such as Argentina and Brazil. Moreover, the weakening Ukrainian hryvnia has made Ukrainian maize more competitive globally, further driving export demand. Despite Ukraine’s relatively smaller crop this year, the overall market dynamics of lower global supply and higher demand have led to sharp price increases.

3. Actionable Recommendations

Diversify Export Destinations and Strengthen Trade Relationships

As the EU has seen a significant surge in corn imports from the US, offsetting declines from Ukraine and Brazil, corn exporters, especially from regions like the US and Canada, should focus on strengthening relationships with key importers and diversifying their markets. This can mitigate risks associated with fluctuations in demand from specific regions. Exporters should also explore emerging markets outside traditional EU buyers, such as Asia and North Africa, where growing demand for animal feed and biofuel (ethanol) could drive corn consumption. For instance, expanding shipments to countries in the Middle East and North Africa, where there is growing demand for corn as animal feed, can offer additional stability to export volumes.

Invest in Infrastructure and Technology to Boost Productivity

The slow pace of the corn harvest in Argentina due to weather-related delays underscores the importance of infrastructure investments to mitigate weather-related production slowdowns. Farmers and agribusinesses in key producing regions should invest in improved irrigation systems, crop monitoring technologies (such as satellite imaging and sensors), and more efficient storage facilities. These measures will help optimize yields, reduce post-harvest losses, and boost crop productivity even in challenging weather conditions. Furthermore, these investments can better position farmers to take advantage of favorable market conditions when they arise, such as the improved weather in Argentina that led to a more positive outlook for the maize harvest.

Leverage Biofuel Demand and Encourage Crop Substitution for Future Sustainability

The growing demand for corn in Paraguay, driven by the expanding ethanol sector, presents a significant opportunity for stakeholders to optimize their biofuel-related market strategies. Ensuring ethanol plants operate at full capacity is essential for stabilizing local corn demand and encouraging increased production. Furthermore, stakeholders should focus on adding value to the corn harvest by diversifying into higher-value biofuels, animal feed, and co-products like bioplastics. Strengthening the corn supply chain through better logistics and direct agreements between farmers and ethanol plants will help minimize costs and inefficiencies. Finally, adopting sustainable farming practices and staying ahead of regulatory requirements will ensure the biofuel industry remains competitive in global markets, meeting the rising demand for renewable energy while supporting economic growth.

Sources: Tridge, Agromeat, Agravery, Foodmate, UkrAgroConsult