In W18 in the olive oil landscape, some of the major trends include:

- Albania's olive oil exports collapsed in Q1-2025, down 75% in volume and 81% in value YoY, due to high production costs, low mechanization, lack of subsidies, and uncompetitive pricing compared to Spain and Greece.

- Spain's export value in 2024 surged by 46% YoY to USD 7.38 billion, driven by a recovery in volume, growing demand in the US, and a broader agri-food trade surplus. However, prices fell 49% YoY to USD 4.30/kg by W18, raising concerns over oversupply and potential impact of US tariffs.

- Turkish olive oil exports declined 40.6% YoY in early 2025 despite record production as exporters faced intense price competition from Spain and Tunisia, compounded by trade restrictions and lack of EU privileges.

1. Weekly News

Albania

Albanian Olive Oil Exports Plunge 75% YoY in Q1-2025 Due to Intense Competition and High Production Costs

Olive oil exports from Albania have sharply declined in Q1-2025, with a 75% drop year-on-year (YoY) in volume and an 81% YoY decrease in value compared to 2024. Exporters face intense competition from Spain and Greece, where prices are lower than in Albania, making Albanian oil uncompetitive. High production costs, limited mechanization, and a lack of state subsidies contribute to the challenges. While the Albanian government is working on improving olive oil storage and marketing through a World Bank-funded project, exporters are relying on increased demand during the tourist season to recover losses.

Italy

Tuscany Defends Olive Oil Identity Against US GI Challenges and Calls for Boosted Production

In Tuscany, concerns over US opposition to geographical indications (GIs) have intensified, with the Tuscan Olive Oil Protection Consortium warning that such efforts threaten the identity and value of Italian extra virgin olive oil. The Consortium president emphasized that the issue is not tariffs, but the risk of market homogenization and price erosion. At a meeting in Bibbona, industry leaders called for increased production to meet rising demand, citing the need to recover abandoned groves and adopt super-intensive cultivation methods compatible with native varieties. The initiative also highlighted the importance of producer organizations in aggregating supply and promoting certified Toscano Protected Geographical Indication (PGI) oil, supported by EU rural development funds.

Spain

Spanish Olive Oil Leads Agri-Food Export Growth with 46% Surge in 2024

Spanish olive oil exports in 2024 surged by 46%, reaching USD 7.38 billion (EUR 6.58 billion) and making it the leading product in the country's agri-food sector by value. This growth contributed significantly to Spain's overall agri-food export performance, which rose 5.9% YoY to USD 83.34 billion (EUR 74.231 billion), with a record trade surplus of USD 20.71 billion (EUR 18.449 billion), according to the annual report of the Cajamar Cooperative Group (Cajamar), the largest cooperative bank in Spain. Olive oil was highlighted for its strong recovery in volume (up 12%) and its growing importance in non-European Union (EU) markets, particularly the United States (US), which increased its imports of Spanish agri-food products by 21%.

Türkiye

Turkish Olive Oil Production Surge Fails to Offset 40.6% YoY Export Decline Amid Global Price Pressure

In Q1-2025, Turkish olive oil exports fell by 40.6% YoY to USD 145.3 million, despite a 150% increase in national production to 475,000 metric tons (mt). Exporters cite intensified price competition from Tunisia and Spain, where average export prices are significantly lower, as a key factor. While Turkish table olives became the world’s largest crop at 700,000 mt, surpassing Egypt and Spain, olive oil exports were constrained by past restrictions, lack of EU trade privileges, and lower international prices. Although EU imports from Türkiye rose 55.9% to 1,146 mt, total EU olive oil import value dropped 50.1% due to declining global prices and stronger European production.

2. Weekly Pricing

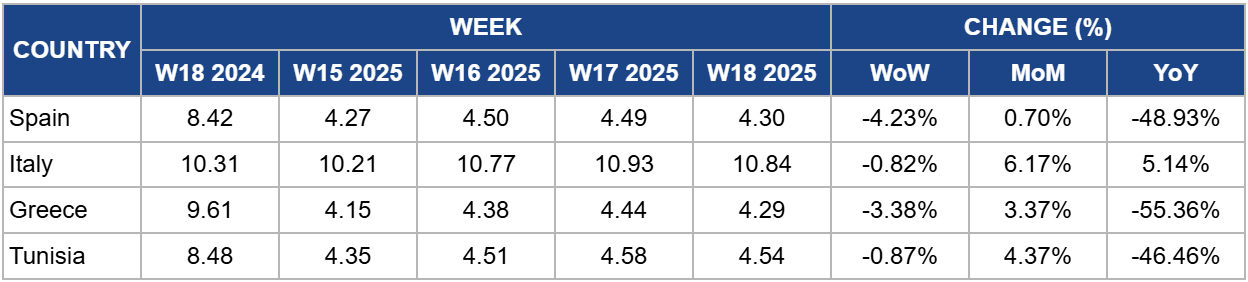

Weekly Olive Oil Pricing Important Exporters (USD/kg)

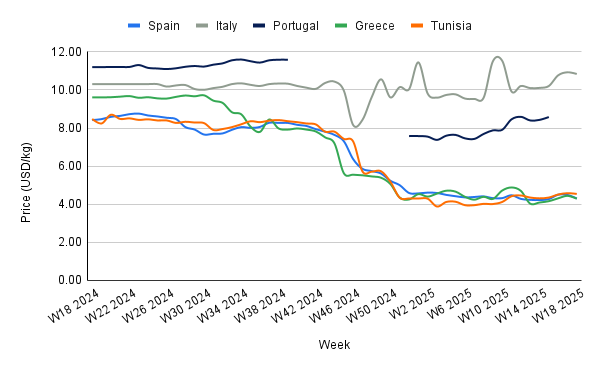

Yearly Change in Olive Oil Pricing Important Exporters (W18 2024 to W18 2025)

Spain

Spain's wholesale olive oil prices have experienced a significant decline, falling to USD 4.30 per kilogram (kg) in W18, marking a 4.23% decrease week-on-week (WoW) and a 48.93% YoY drop from USD 8.42/kg. While recent months have seen some stability following previous price surges caused by drought and production shortages, the market faces new uncertainty due to the potential imposition of 20% tariffs by the US on European products, including olive oil.

The US accounts for 40% of Spain's olive oil exports, and potential tariffs could severely impact producers. If tariffs are imposed, Spain may face either an oversupply in Europe, lowering prices, or producers could restrict supply to maintain margins, raising prices domestically. This could worsen the financial strain on consumers already facing high olive oil prices. Additionally, the tariffs could disrupt the supply chain, increasing production costs and leading to higher consumer prices, potentially reducing demand as people seek cheaper alternatives.

Italy

In W18, Italy's olive oil prices decreased slightly to USD 10.84/kg, reflecting a 0.82% WoW drop, but a 5.14% YoY increase from USD 10.31/kg. This price movement comes amidst growing concerns about potential retaliatory tariffs following the US President's tariff announcements. The Italian Economy Minister cautioned against imposing counter-tariffs, fearing the negative impact they could have on Italy, which has a substantial trade surplus with the US. If tariffs are enacted, the olive oil market could see increased costs for Italian exports, potentially driving up prices further and disrupting trade, especially to key markets like the US. This would affect current pricing dynamics and future trade relationships.

Greece

Greece's olive oil prices fell to USD 4.29/kg in W18, marking a 3.38% WoW drop and a sharp 55.36% YoY decline from USD 9.61/kg. The yearly decrease reflects a significant recovery in production following previous supply shortages, which had driven prices to historic highs. Current production estimates for 2024/25 remain stable at 250,000 mt. However, minimal stock levels continue to limit supply flexibility. As mid-2025 approaches, tightening availability and resilient demand are beginning to reverse the downward price trend. Despite improved yields, the Greek olive oil market remains vulnerable to climatic variability, which could quickly alter future pricing trajectories.

Tunisia

In W18, Tunisia's olive oil prices declined to USD 4.54/kg, down by 0.87% WoW and a significant 46.46% YoY from USD 8.48/kg. The sharp annual drop is primarily attributed to a record harvest, up 75%, and a 41% increase in exports between Nov-24 and Feb-25, which expanded global supply and exerted downward pressure on prices. However, recent stabilization is supported by rising international demand and Tunisia's pivot toward premium, value-added packaged exports. Combined with ongoing export regulation reforms and diversification into 64 global markets, these strategies are mitigating price volatility and could support moderate price recovery in the near term.

3. Actionable Recommendations

Modernize Production and Support Smallholders in High-Cost Regions

Albanian producers should prioritize investments in mechanization, cooperative development, and training programs to reduce production costs and improve efficiency. Government and donor-funded programs should expand access to machinery, support cluster-based production models, and incentivize certifications (e.g., organic, PGI) to increase competitiveness against low-cost exporters like Spain and Tunisia.

Target Premium and Tourism-Linked Segments to Offset Price Competition

In light of Albania's pricing disadvantage, exporters should pivot toward value-added, packaged olive oils tied to regional identity and quality certifications. Coordinating with tourism boards, producers can promote olive oil tastings, farm tours, and co-branded products during the tourist season to capture premium margins and raise brand recognition in international markets.

Develop Strategic Export Alliances with Undersupplied Markets

Albania and Türkiye can explore targeted export agreements with countries experiencing domestic shortages, such as Italy, or expanding demand, such as Canada and Brazil. These partnerships can be structured around private-label packaging or bulk supply agreements, supported by diplomatic engagement and trade facilitation tools to ease entry into higher-value segments.

Sources: Tridge, Agro Diario, Mundus Agri, Olivo News, Politiko, OK Diario