In W18 in the orange landscape, some of the most relevant trends included:

- Prices are rising in Spain, Italy, and California, while Greece is seeing lower prices and Peru is experiencing declining exports. South Africa anticipates growth in exports despite tariff concerns.

- Favorable weather conditions support good fruit quality in Spain, California, and South Africa, while Greece faces challenges due to market pressures.

- Peru's limited focus on Valencia oranges has led to a sharp export decline, while Mexico shifts to alternative orange types due to limited Valencia supply.

- South Africa faces risks from unresolved tariff issues with the US and phytosanitary concerns in the EU, which could disrupt orange exports.

1. Weekly News

Europe

Southern Europe Sees Diverging Orange Price Trends in Early 2025

In the first quarter of 2025 (Q1-25), orange prices in Southern Europe showed mixed trends. Spain saw steady growth, with prices rising from USD 89.72 per 100 kilograms (EUR 79/100 kg) to USD 95.40/100 kg (EUR 84/100 kg) between Jan-25 and Mar-25, staying above the five-year average and signaling stable demand. Italy posted the highest prices, beginning at USD 159/100 kg (EUR 140/100 kg) and easing slightly to USD 144.61/100 kg (EUR 129/100 kg), still well above historical norms due to favorable market conditions. Portugal maintained relatively stable prices, ranging from USD 90.80/100 kg (EUR 81/100 kg) to USD 86.31/100 kg (EUR 76/100 kg), indicating balanced supply and demand. Meanwhile, Greece faced market pressure, with prices dipping to USD 55.65/100 kg (EUR 49/100kg) in Feb-25 before a slight rebound to USD 60.19/100 kg (EUR 53/100 kg) in Mar-25, remaining below last season's figures and the five-year average.

Mexico

Valencia Orange Season Ends in Veracruz Due to Limited Supply

In Veracruz, Mexico, the recent conclusion of the Valencia orange harvest, commonly referred to as the 'late' orange season, underscored the variety’s economic and culinary importance in the region. Valencia oranges, typically harvested twice a year, are prized for their sweetness, low seed content, and juicing qualities. This season, however, saw reduced availability, prompting some growers to shift to alternative varieties such as ‘Mayera’ and ‘Norteña.’ The late Valencia harvest usually runs from November through April, sometimes extending into May. This year’s limited supply has driven up market prices, while the fruit’s versatility continues to sustain strong demand across fresh consumption and culinary applications, including sauces, desserts, beverages, and jams.

Peru

Peru’s Orange Exports Drop Sharply in 2024/25 Season

As of W16, Peru's orange exports have dropped sharply to just 179 tons, a 61.34% year-on-year (YoY) decrease from the 463 tons exported during the same period last year. All shipments were destined for Latin America, with the Dominican Republic as the top market. Production was concentrated in the Junín region, which accounted for 58.1% of the volume, followed by Lima at 41.9%. The exports consisted entirely of the Valencia variety, reflecting limited diversification and a narrower market focus this season.

South Africa

South Africa Projects Growth in Orange Exports Despite Tariff Concerns

South Africa’s citrus industry anticipates a 6% YoY increase in Valencia orange exports for the 2025 season, reaching 52 million 15-kg cartons. Meanwhile, Navel orange exports are expected to rise by 5% to 26.1 million cartons. This growth supports a projected total citrus export volume of 171.1 million cartons across all types, reflecting a 3.6% YoY increase. However, the Citrus Growers' Association of Southern Africa cautions that unresolved tariff issues with the United States (US) could disrupt orange shipments if no trade agreement is reached soon. Additional concerns include port inefficiencies, existing tariffs in other key markets, and phytosanitary barriers in the European Union (EU). These factors pose risks to the industry’s export potential. Nonetheless, the industry remains cautiously optimistic about maintaining its growth momentum.

United States

California Orange Market Sees Strong Demand and Rising Prices Due to Seasonal Shift

California’s citrus season is progressing well under favorable weather conditions, with light rainfall enhancing fruit quality without causing harm. As of early May-25, Navel orange supplies are nearly exhausted, with the final harvest beginning on May 2, 2025, and expected to conclude by late May-25 or early Jun-25. In contrast, Valencia oranges are still widely available, though their sugar content is still developing and is anticipated to reach ideal levels in about four weeks. Most of the current Valencia crop consists of smaller-sized fruit (113s to 168s). With Navel stocks dwindling and a shortage of large, sweet Valencias, market demand remains strong, driving prices upward and reinforcing a clear bullish trend in the California orange market.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W18 2024 to W18 2025)

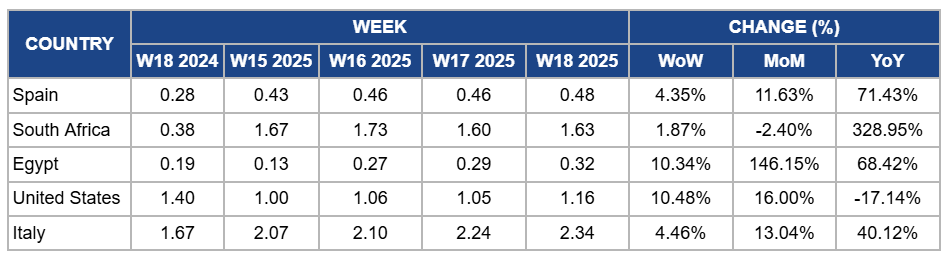

Spain

In W18, orange prices in Spain rose by 4.35% week-on-week (WoW) to USD 0.48/kg, reflecting an 11.63% month-on-month (MoM) increase and a 71.43% YoY surge. This price increase is due to a gradual recovery in the Spanish orange market during the winter months, with prices rising from USD 85.26/100 kg (EUR 76/100 kg) in Dec-25 to USD 90.87/100 kg (EUR 81/100 kg) in Feb-25, indicating improved demand and firmer market conditions. Despite a forecasted 8.8% increase in orange production for the 2024/25 season, the total citrus output remains 8.6% below the five-year average, suggesting that supply constraints may be contributing to the upward price trend.

South Africa

South Africa’s orange prices rose slightly by 1.87% WoW to USD 1.63/kg in W18, marking a significant 328.95% YoY surge. This sharp annual increase can be attributed to strong export demand, as evidenced by a 6% rise in Valencia orange exports and a 5% increase in Navel orange exports. The higher export volumes likely reflect robust international demand, which tightened domestic supply and placed upward pressure on prices. Moreover, while the average export price reached USD 1,024 per ton in 2024, a 59% YoY increase, this rise suggests global buyers are willing to pay more for South African oranges, potentially due to improved quality, limited global supply, or shifts in competing suppliers' availability. These factors collectively reinforced the YoY price surge. On a monthly basis, however, prices declined slightly by 2.40%, likely due to port inefficiencies and unresolved tariff issues with the US. These logistical and trade-related challenges may have disrupted shipping flows, slowing down exports and temporarily relieving price pressure in the domestic market.

Egypt

In W18, orange prices in Egypt increased by 10.34% WoW to USD 0.32/kg, reflecting a 146.15% MoM and 68.42% YoY increase. This price rise is due to a significant reduction in the harvest caused by abnormal heat during the flowering period. This led to a nearly one-third decrease in yield and a predominance of medium-sized fruits, which consisted of 90% of the crop. As a result, supply to premium markets has been limited. Meanwhile, heightened demand for citrus fruits has been exacerbated by drought and increased production costs in competing countries like Spain and Italy. Additionally, the rapid development of Egypt's orange processing industry, driven by high global prices for orange juice concentrate following a sharp decline in Brazil's production, has intensified competition for fresh oranges, further pushing prices upward.

United States

Orange prices in the US increased by 10.48% WoW to USD 1.16/kg in W18, with a 16% MoM rise due to tightening supplies of Navel oranges as the season concludes in early May-25 and strong demand for the still-developing Valencia crop. The limited availability of large, sweet oranges has driven up prices amid strong market demand. However, YoY prices dropped by 17.14% due to a significant decline in orange juice demand, attributed to high prices, reduced quality, and shifting consumer preferences.

Italy

In W18, orange prices in Italy increased by 4.46% WoW to USD 2.34/kg, marking a 13.04% MoM and a 40.12% YoY rise. This price increase is due to strong export demand, particularly for premium varieties like Navel VCR, which are favored in both Eastern and Western European markets. The limited supply from key competitors, especially Spain, has bolstered Italy's export position, allowing for favorable pricing. Additionally, Italy's orange prices have consistently remained above the five-year average, reflecting strong market conditions and sustained demand.

3. Actionable Recommendations

Prioritize Size and Brix Through Targeted Irrigation and Thinning

Orange producers should focus on achieving larger fruit size and higher sugar levels by adjusting irrigation schedules and implementing strategic fruit thinning. Growers in regions such as the US, Spain, Egypt, and South Africa can apply regulated deficit irrigation during early fruit development to control vegetative growth, then gradually increase water as the fruit matures to enhance size. Additionally, thinning excess fruit early in the season ensures better resource allocation per fruit, leading to improved marketable quality. These steps help meet demand for larger, sweeter oranges during peak market windows.

Expand Market Reach with Varietal and Packaging Diversification

Orange producers should diversify varieties and packaging formats to tap into broader export markets beyond regional buyers. At the same time, offering smaller consumer-ready packaging such as netted bags or snack-size boxes can help target retail chains in North America, Europe, and Asia. These steps open access to higher-value markets and reduce overreliance on single destinations or varieties.

Sources: Tridge, Agraria, Citrus Growers' Association of Southern Africa, Eastfruit, European Commission, Freshplaza, OEM