In W18 in the palm oil landscape, some of the most relevant trends included:

- China is advancing sustainable palm oil sourcing through partnerships and biodiesel research with major producers like Malaysia.

- Indonesia is prioritizing palm oil as a key economic sector, attracting USD 916 million in Q1-2025 investment for downstream processing, expanding biodiesel mandates (B40 to B50), and targeting global leadership in production by 2025.

- Indonesia’s palm oil output is projected to rise 3% to 47 mmt in 2025/26 due to favorable weather and increased fertilizer use.Domestic demand is growing, driven by industrial use and biodiesel policies.

- Palm oil prices fell in W18 across Indonesia, Malaysia, and Thailand due to shared pressures from global edible oil market softness, such as rising inventories and weak exports in Indonesia and Malaysia, and domestic agricultural strain in Thailand.

1. Weekly News

China

China's Sustainability Drive Boosts Global Palm Oil Industry Through Strategic Partnerships and Innovation

China's increasing emphasis on sustainability plays a key role in promoting environmentally and socially responsible practices in the global palm oil industry, according to the Council of Palm Oil Producing Countries (CPOPC). As China is the world's third-largest consumer of palm oil, importing over 6 million metric tons (mmt) annually, it is strengthening cooperation with producing countries through partnerships, research, and trade agreements. Notable initiatives include collaborations between Chinese institutions and Malaysian producers, such as Tsinghua University's joint efforts with the Malaysian Palm Oil Board (MPOB) to advance biodiesel applications.

Indonesia

Indonesia Secures USD 916 Million for Palm Oil Processing in Q1-2025 to Boost Downstream Development

In Q1-2025, Indonesia secured approximately USD 916 million in investment for palm oil processing, according to the Minister of Investment and Downstream Industry. The move is part of a broader strategy to shift from exporting raw commodities to high-value products, as the country seeks to develop its downstream industries. While most investments remain concentrated in nickel processing, the government is working to expand value-added activities in other sectors, including palm oil, to attract both domestic and foreign investors and enhance export revenues.

Indonesia Advances Toward Global Palm Oil Leadership with 2025 Production and Biodiesel Targets

Indonesia is intensifying efforts to become the world’s largest palm oil producer by 2025, positioning the sector as a national economic priority. The Ministry of Agriculture is promoting the use of advanced technologies and high-quality seeds, alongside policies to stabilize pricing and encourage farmer and industry participation. The rollout of the B50 biodiesel mandate is central to absorbing domestic palm oil output, complementing earlier initiatives such as the B40 program.

According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS), Indonesia’s palm oil production is projected to rise by 3% to 47 mmt in the 2025/26 season, supported by favorable weather and increased fertilizer use. While the harvested area remains stable, high global prices are expected to drive future expansion. Domestic consumption is forecast to reach 22.6 mmt, largely fueled by industrial demand linked to biodiesel. However, an additional 4 billion liters (L) of production capacity is still required to fully implement the B50 mandate. Exports are expected to grow modestly to 24 mmt due to higher levies and shifting demand in major markets, while palm oil stocks are projected to increase by 8% to 5.3 mmt, indicating sufficient domestic supply.

Indonesia Proposes Expanded Palm Oil Exports to Japan Following Surplus and Agricultural Cooperation Efforts

Indonesia is exploring opportunities to expand crude palm oil (CPO) exports to Japan amid a domestic surplus of 25 mmt, according to Indonesia's Minister of Agriculture. In recent bilateral talks, Indonesia proposed increasing CPO trade in exchange for Japanese milk imports, with discussions ongoing regarding technical specifications and halal certification. The initiative underscores broader efforts to strengthen agricultural cooperation between the two countries, particularly in addressing climate-related production challenges and enhancing food security through strategic trade partnerships.

2. Weekly Pricing

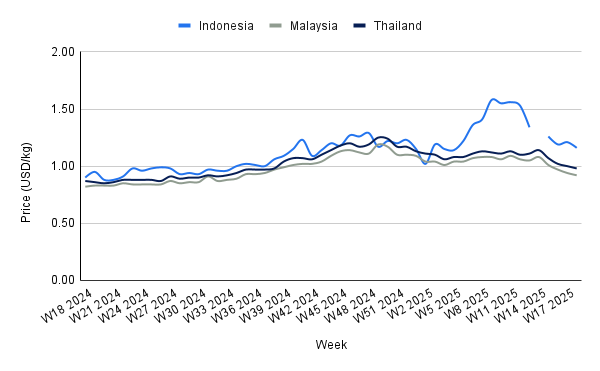

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W18 2024 to W18 2025)

Indonesia

Indonesia's palm oil prices fell to USD 1.16 per kilogram (kg) in W18, a 4.13% week-on-week (WoW) decline, despite showing a 28.89% year-on-year (YoY) increase. This recent price drop follows the government's decision to lower the CPO reference price to USD 924.46 per metric ton (mt) for May-25, reflecting efforts to align domestic pricing with global trends and support export competitiveness. Indonesia's palm oil production is expected to rise 3% to 47 mmt in 2025/26 due to better yields from favorable weather and cheaper fertilizers. While short-term prices may face pressure from rising stocks and modest export growth, strong domestic demand, driven by the B40 mandate and potential B50 rollout, could support prices later in 2025.

Malaysia

Malaysia’s palm oil prices fell to USD 0.92/kg in W18, down 2.13% WoW, amid broader weakness in crude oil and edible oil markets, particularly in China. Although prices remain 12.20% higher YoY, the recent decline reflects mounting short-term pressures. A stronger ringgit (MYR) is reducing Malaysia's export competitiveness, while production gains outpacing export growth are expected to drive inventory build-up by the end of Apr-25. Surveyor data shows Apr-25 exports rose an average of 13.8 to 14.8% versus Mar-25, but the increase remains insufficient to offset rising supplies. If this trend continues, further downward pressure on prices may persist in the short term, although firm global demand and tighter regional supplies could offer support later in the year.

Thailand

In W18, Thailand’s palm oil prices fell to USD 0.98/kg, marking a 2% WoW decline, despite a 12.64% increase YoY from USD 0.87/kg. This continued weakness reflects broader agricultural strain, as rising input costs and falling commodity prices pressure Thai farmers' profitability. The erosion of producer margins has led to growing calls for government intervention to stabilize incomes, with potential supply risks emerging if smallholders reduce output. In the absence of targeted support or stronger regional demand, prices may remain under pressure, particularly amid seasonal production increases and heightened competition from lower-priced producers such as Indonesia and Malaysia.

3. Actionable Recommendations

Enhance Investment in Value-Added Processing

Palm oil producers should prioritize downstream investments, such as refining, biodiesel production, and specialty fats, to increase export revenues and reduce reliance on raw commodity exports. This aligns with Indonesia's current strategy and helps capture more value from rising domestic output.

Strengthen Trade Partnerships with Sustainability Focus

Exporters should deepen bilateral trade agreements with major consumers like China and Japan, integrating sustainability standards and technical certifications. These partnerships can unlock long-term demand while meeting the growing global emphasis on environmentally responsible sourcing.

Sources: Tridge, Jakarta Globe, Oils and Fats International, China Daily, Ukr AgroConsult, Republika