W18 2025: Peanut Weekly Update

In W18 in the peanut landscape, some of the most relevant trends included:

- Despite challenges like delayed harvesting due to weather conditions, Córdoba’s 2024/25 harvest is expected to yield 727,000 mt of peanuts, marking a 2% annual increase.

- Bangladesh's Rangpur region is experiencing strong profits from peanut cultivation, with yields of 22 to 28 maunds per acre, attributed to high-yielding varieties and favorable market prices.

- The US is seeing a rise in peanut acreage for 2025, projected at 1.95 million acres, as farmers respond to weak commodity prices and favorable profitability despite rising input costs. The surge is most notable in Georgia and other Southeastern states.

- Brazil's wholesale peanut prices rose 3.97% WoW, with a 15.02% YoY increase, due to strong harvest volumes and high-quality peanuts. However, persistent rainfall poses risks to the overall output.

1. Weekly News

Argentina

Córdoba's 2024/25 Peanut Production Forecasted to Reach 727,000 mt

Peanut production in Córdoba for the 2024/25 season is projected to reach 727,000 metric tons (mt), reflecting 2% annual growth despite recent weather-related delays in harvesting. Favorable conditions during the yield-setting period supported this increase, though rain has hindered crop drying and machinery access to fields. The steady rise in peanut output underlines the crop's resilience and its growing contribution to the region's agricultural sector.

Bangladesh

Bangladesh's Rangpur Region Sees Strong Profits and Growth in Peanut Cultivation

Farmers in Bangladesh's Rangpur region are reporting strong profits from peanut cultivation this season, earning up to USD 658.45 per acre (BDT 80,000/acre) with yields of approximately 0.82 to 1.05 mt/acre and favorable market prices of USD 32.94 to 34.59 per 37.3 kilograms (BDT 4,000 to 4,200/37.3 kg). Despite planting slightly below the initial target, the region produced 11,928 mt of peanuts from 5,679 hectares (ha) at an average yield of 2.10 mt/ha. The success is attributed to high-yielding varieties developed by the Bangladesh Agricultural Research Institute (BARI), low input costs, and growing demand from the food industry. Due to consistent profitability, peanut cultivation is expanding, particularly in riverine char areas.

United States

US Peanut Acreage Expected to Rise in 2025 Amid Profitability and Market Uncertainty

The United States (US) peanut acreage is projected to rise to 1.95 million acres in 2025, up from 1.76 million in 2024, driven by weak competing commodity prices and sustained profitability in peanuts. Georgia leads with a 12% year-on-year (YoY) increase, followed by notable gains in Florida, Mississippi, South Carolina, and Oklahoma. However, concerns are growing over potential carryover and price pressure if yields are strong. Producers face high input costs, with fertilizer and herbicides remaining expensive, prompting some to adjust cropping strategies or diversify into cattle operations. Despite economic challenges, peanuts remain a relatively profitable option, especially in irrigated systems.

2. Weekly Pricing

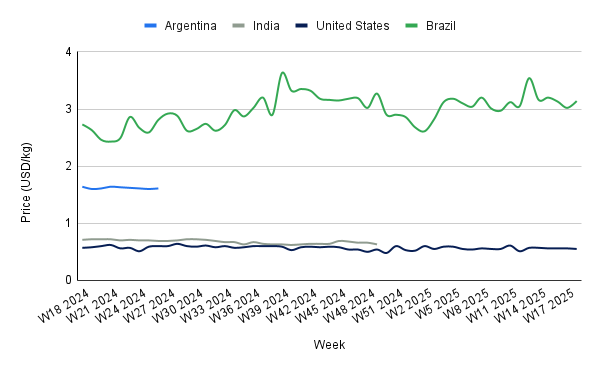

Weekly Peanut Pricing Important Exporters (USD/kg)

Yearly Change in Peanut Pricing Important Exporters (W18 2024 to W18 2025)

United States

US peanut prices declined to USD 0.55/kg in W18, down 1.79% both week-on-week (WoW) and month-on-month (MoM), reflecting early signs of potential oversupply as planted acreage expands. The projected rise in peanut acreage to 1.95 million acres, up 11% from 2024, is driven by comparatively weak prices in other row crops and continued profitability in peanuts, especially in irrigated systems. Georgia's 12% YoY increase leads the surge, with similar gains in other Southeastern states. However, if favorable weather results in strong yields, market pressures may intensify due to carryover concerns.

Brazil

Brazil's wholesale peanut prices surged to USD 3.14/kg in W18, marking a 3.97% WoW increase and a 15.02% YoY rise from USD 2.73/kg. This price uptick coincides with strong harvest volumes and high-quality peanuts reported as of W17, signaling favorable export prospects. However, persistent rainfall poses a significant risk to harvest progress, threatening to delay completion and reduce overall output. If adverse weather conditions continue and disrupt harvest timelines, reduced supply could exert upward pressure on prices in the medium term, potentially reversing recent declines.

3. Actionable Recommendations

Diversify Sourcing to Mitigate Weather Risks in Peanut Production

As weather disruptions, including persistent rainfall, threaten peanut harvests in key producing regions like Brazil and Córdoba, stakeholders should diversify their sourcing strategies. Expanding supplier networks across different regions, such as the US, Bangladesh, and other parts of South America, will help balance supply disruptions. Long-term contracts and strategic partnerships with multiple producers can further secure consistent peanut supply amid unpredictable weather patterns.

Adapt to Growing Demand for Peanuts in Emerging Markets

With rising profitability and expanding cultivation in regions like Bangladesh and the US, there is an opportunity to tap into the growing demand for peanuts in both local and international markets. Exporters should focus on strengthening their presence in high-demand regions, especially in Southeast Asia and Europe, by promoting the nutritional value and versatility of peanuts in the food industry. This can be achieved through marketing campaigns and partnerships with food processors, tapping into both traditional and emerging consumer segments.

Sources: Tridge, Farm Progress, The Business Standard, La Voz