.jpg)

In W18 in the potato landscape, some of the most relevant trends included:

- Idaho's potato acreage is expected to decrease by 5% in 2025, reaching its lowest level since 1952, due to oversupply, reduced demand from frozen potato processors, and a shift towards alternative crops.

- Spain's potato production faced severe disruptions due to excessive rainfall and flooding. This caused significant crop quality damage and delays in planting, which may lead to reduced yields and higher prices, increasing reliance on imports.

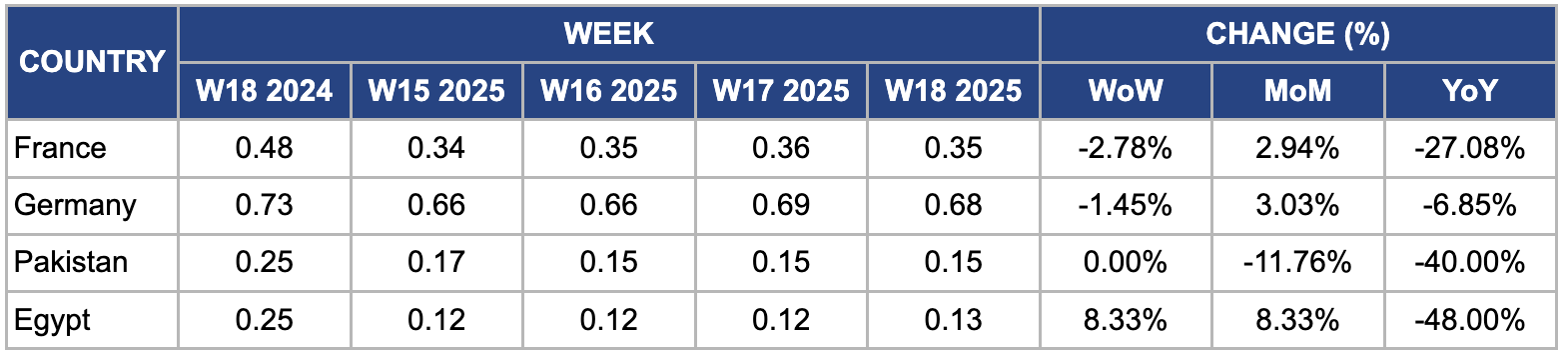

- Global potato prices showed mixed trends in W18, with France and Germany experiencing price declines due to increased supply and reduced demand from processors. In contrast, Egypt's prices rose WoW, driven by strong export demand, particularly from new markets like Tajikistan and the Balkans.

1. Weekly News

Bangladesh

Rangpur Farmers Harvest 39,862 MT of Sweet Potatoes in 2024/25 Despite Smaller Area

In the 2024/25 Rabi season, farmers across all five districts of Bangladesh's Rangpur agricultural region harvested 39,862 metric tons (mt) of sweet potatoes, exceeding 2024's output by 174 mt. Although the Department of Agricultural Extension (DAE) had initially targeted production of 44,617 mt from 1,895 hectares (ha), farmers cultivated only 1,653 ha, as many opted to grow winter vegetables, maize, and potatoes instead. Despite the reduced area, the bumper yield pleased farmers, who received favorable market prices ranging from USD 10.70 to 11.52 per 40 kilograms (kg), depending on the variety and quality.

Spain

Spain's Potato Production Hit by Floods, Only 5% of Area Planted by Late Mar-25

Excessive rainfall and flooding in Spain have severely disrupted the country's potato production, damaging crop quality and delaying planting. Only 5% of the expected area had been sown by late Mar-25, compared to the usual 50%. This is particularly concerning as the Spanish potato season typically begins in April. Despite positive early-season projections, conditions deteriorated rapidly, making a full recovery unlikely for many growers. The disruptions could result in reduced yields, higher consumer prices, and increased import reliance. Exacerbated by climate-related shifts and extreme weather events, these challenges highlight the growing vulnerability of staple crops like potatoes to environmental shocks.

United States

Idaho Potato Acreage Projected to Fall 5% YoY in 2025, Hitting Lowest Level Since 1952

Renowned worldwide for its potato production, Idaho is projected to reduce its potato acreage by 5% year-on-year (YoY), from 127,500 ha in 2024 to 121,400 ha in 2025. According to the Idaho Farm Bureau Federation, this marked the state's lowest planted area since 1952. Farmer emphasized the crop’s economic and cultural significance, noting its global impact and popularity in various forms, from French fries to hash browns. The decline is primarily driven by oversupply and weakened demand, with frozen potato processors cutting contract volumes by 5% to 15%, and some farmers left without contracts altogether, prompting a shift toward alternative crops.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W18 2024 to W18 2025)

France

In W18, France's potato prices declined 2.78% week-on-week (WoW) to USD 0.35/kg due to a combination of factors. One key reason was the increased supply of potatoes from cold storage, which added to the available stock in the market. Moreover, favorable weather conditions in southern France, particularly in regions like Provence and Occitanie, led to an earlier-than-usual harvest of new-season potatoes. This surge in fresh potato supply, coupled with a decrease in demand from processors who had ample inventory, put downward pressure on prices. Furthermore, the general market slowdown due to the transition from stored to fresh potatoes also contributed to the price drop.

Germany

In W18, Germany's wholesale potato prices declined by 1.45% WoW, falling to USD 0.68/kg from USD 0.69/kg. The drop was mainly due to dry weather in early Mar-25 and Apr-25, facilitating early planting, with half of the potato crops already planted as of April 23. The expectation of an early harvest put downward pressure on prices. Moreover, lower demand from the food processing sector, where customers were already stocked up, contributed to the price drop. Seasonal effects, with an increased supply of newly harvested potatoes, added to the downward pressure on prices. Despite the slight decline, potato prices remained relatively stable compared to previous weeks, reflecting a balance between supply and demand in the German market.

Pakistan

In W18, Pakistan’s potato prices remained stable WoW, but saw a significant drop of 11.76% month-on-month (MoM), falling to USD 0.15/kg, marking a 40% YoY decline. The decline is due to the active harvesting of potatoes in Punjab, the country’s primary production region, which flooded the market with fresh supplies. Many farmers expanded their planting areas, buoyed by favorable returns from the previous season, while favorable weather conditions also boosted yields. Stable input costs, particularly for fertilizers and fuel, eased financial pressures on farmers, helping them remain profitable despite lower prices. On the demand side, reduced export interest kept more potatoes within the domestic market. Meanwhile, improvements in the internal distribution system helped move products efficiently to key consumption areas, maintaining balanced market conditions.

Egypt

In W18, Egypt's potato prices rose 8.33% WoW and MoM, reaching USD 0.13/kg. This price increase was due to strong export demand, fueled by expanded access to new markets such as Tajikistan and the Balkans, and renewed demand in traditional markets like Spain and the Gulf. Moreover, exports to Russia have surged, supported by reduced customs duties to curb food inflation. Egypt's potato exports will grow by 10 to 15% YoY in 2025.

3. Actionable Recommendations

Diversify Potato Crop Varieties and Explore Alternative Markets

Given the 5% reduction in potato acreage and the challenges from oversupply and weakened demand, Idaho should focus on diversifying its potato crop varieties and exploring new markets. This could include investing in niche potato varieties (such as specialty or organic potatoes) that can command premium prices in both domestic and international markets. Furthermore, expanding into new export markets or diversifying into value-added products like dehydrated potatoes, potato chips, and frozen potato products could help offset declining demand from traditional buyers.

Build Resilient Potato Farming Systems Against Climate Shocks

Extreme weather conditions, such as excessive rainfall and flooding, have severely impacted Spain’s potato production, causing delayed planting and potential yield reductions. The government, agricultural organizations, and producers should explore and invest in climate-resilient farming practices. They could adopt early-warning climate systems and implement crop insurance schemes tailored to extreme weather events. Encouraging greenhouse technology or raised beds for crop protection could mitigate some of the risks posed by erratic rainfall patterns. Promoting climate-resilient farming technologies like raised beds and greenhouses will help protect against extreme weather.

Strengthen Export Infrastructure and Diversify Market Base

Egypt’s potato market has experienced price increases due to rising export demand, particularly from new markets like Tajikistan and the Balkans. Egypt should strengthen its potato export infrastructure to meet international quality standards and sustain export growth. Moreover, continued market diversification is essential to reduce reliance on traditional markets and increase resilience against global economic shifts. Expanding partnerships with emerging markets in Asia, Africa, and the Middle East will be crucial. This includes investing in modernizing storage, packaging, and transportation facilities to improve export quality and shelf life. Egypt should also engage in market research to identify new potential markets and build export relationships with emerging economies.

Sources: Tridge, BSS News, Fresh Plaza, The Cool Down