In W18 in the soybean oil landscape, some of the most relevant trends included:

- China's record soybean imports from South America in Q2-2025, exceeding 30 mmt. China is reducing reliance on US supplies, driven by the US-China trade tensions and new US tariffs. This shift is tightening soybean availability for oil extraction, adding upward pressure on global soybean oil prices.

- The US soybean oil market outlook remains uncertain due to ambiguous trade and biofuel policies. While biofuel demand supports prices, falling biodiesel production and fragile export prospects, especially to China, pose downside risks.

- Brazil’s soybean oil prices rose due to strong Chinese demand for whole soybeans, limiting crushing volumes, while Argentina’s prices dropped amid seasonal supply pressures and logistical bottlenecks.

- European soybean oil markets face volatility as the EU weighs retaliatory tariffs on US soybeans. The Netherlands saw modest price declines amid geopolitical uncertainty, while Spain experienced price hikes on tightening global supplies and trade risks.

1. Weekly News

China

China's Surging South American Soybean Imports May Tighten Global Soybean Oil Supply

China's record-high soybean imports from South America in Q2-2025, exceeding 30 million metric tons (mmt), are easing domestic feed costs and reducing China’s reliance on United States (US) supplies. Driven by the ongoing US-China trade tensions and new tariffs under the US President's administration, this shift has strengthened Brazil's position as China's top soybean supplier. Although US soybean exports to China totaled over 27 mmt in 2024, recent purchases have stalled since Jan-25. The influx of South American soybeans may tighten availability for oil extraction, potentially impacting global soybean oil supply and prices.

United States

Policy Uncertainty Weighs on US Soybean Oil Outlook Amid Biofuel Demand and Trade Tensions

Uncertainty surrounding US trade and biofuel policy under the current US President continues to cloud the outlook for soybean oil. While China remains firm in opposing tariff pressure and has not engaged in recent trade talks with the US, demand from the biofuel sector is currently the main support for US soybean prices. However, unclear government direction has contributed to a decline in domestic biodiesel production, despite rising soybean oil exports. Clean Fuels Alliance America, a US-based industry association that represents producers, marketers, and distributors, is urging clarity on biodiesel policy, as hedge funds remain cautiously optimistic about soybean prices amid ongoing weather concerns and policy ambiguity.

US Soybean Crushing Capacity Expands 14%, Driven by Rising Soybean Oil Demand

US soybean crushing capacity has expanded by 14% since early 2023, rising from 2.23 to 2.55 billion bushels annually, with further growth expected to surpass 2.78 billion bushels by 2030 if planned expansions proceed. This growth is largely driven by rising domestic demand for soybean oil, fueled by the surge in renewable diesel production, which has grown nearly sixfold since 2021. As soybean oil accounts for about 20% of the crush yield, this increased biofuel demand has reshaped processing dynamics, encouraging new investments in crushing facilities, particularly in regions like the Dakotas that were previously focused on soybean exports. This shift is likely to continue supporting strong domestic soybean oil demand and prices in the coming years.

2. Weekly Pricing

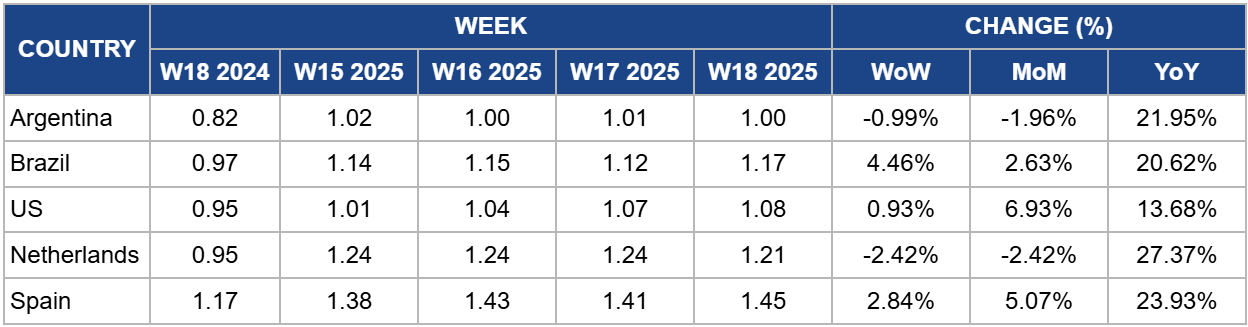

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

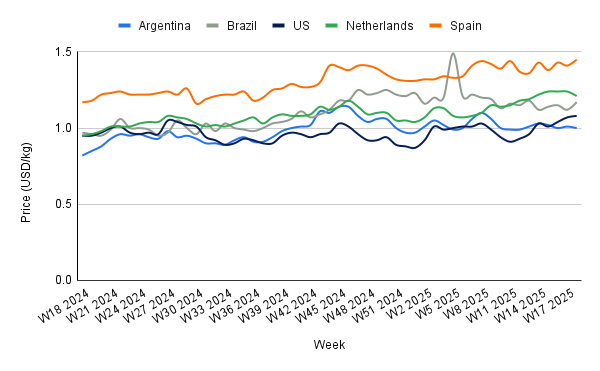

Yearly Change in Soybean Oil Pricing Important Exporters (W18 2024 to W18 2025)

Argentina

In W18, Argentina’s soybean oil prices declined marginally by 0.99% week-on-week (WoW) to USD 1 per kilogram (kg), but remained 21.95% higher year-on-year (YoY), up from USD 0.82/kg. This slight correction reflects seasonal supply pressure from delayed harvest progress and ongoing logistics constraints, which have slowed exports and reduced overall processing activity. However, continued strength in global vegetable oil markets, driven by lower sunflower oil availability and steady US biodiesel demand, has helped keep prices relatively stable.

Brazil

Brazil's soybean oil prices rose to USD 1.17/kg in W18, marking a 4.46% WoW and 20.62% YoY increase. This price growth reflects tightening global vegetable oil supplies and heightened competition for raw soybeans within Brazil, as strong Chinese demand for whole soybeans diverts volumes away from domestic crushers. The price increase is linked to reduced domestic soybean availability for oil extraction, as export-oriented whole bean shipments to China remain elevated. This dynamic limits processing margins for oil and meal producers, contributing to constrained domestic output and firmer prices. If global soybean trade continues to prioritize raw exports over crushing, soybean oil supply could tighten further, supporting elevated prices in the coming months.

United States

US soybean oil prices increased to USD 1.08/kg in W18, marking a 0.93% weekly increase and a 13.68% YoY rise from USD 0.95/kg. This price surge is primarily driven by robust domestic demand and tightening export prospects, which have supported market stability. However, the outlook for soybean oil remains clouded by uncertainty surrounding US trade and biofuel policies. The ongoing trade tensions with China, compounded by a lack of recent talks, have left soybean oil exports in a fragile position, with tariffs continuing to weigh on trade dynamics. Despite these challenges, the biofuel sector, particularly renewable diesel demand, remains a key driver for soybean oil prices.

Netherlands

In the Netherlands, wholesale soybean oil prices fell to USD 1.21/kg in W18, reflecting a 2.42% WoW and month-on-month (MoM) decline from USD 1.24/kg. This price reduction comes amid ongoing supply uncertainties and geopolitical tensions that could impact future price movements. As a critical import hub for the European Union (EU), the Netherlands is particularly vulnerable to changes in trade dynamics. The EU's approval of retaliatory tariffs on US agricultural products, including soybeans, could disrupt US soybean shipments to Europe. A reduction in these shipments may strain crushing margins, leading to further price volatility.

Spain

In W18, Spain's soybean oil price increased to USD 1.45/kg, a 2.84% WoW rise and a significant 23.93% YoY increase. This upward trend is driven by tightening global supplies and uncertainty in trade policies, particularly the ongoing tariff dispute between the EU and the US. The EU's potential imposition of retaliatory tariffs on US agricultural products, including soybeans, could severely disrupt Spain's soybean supply. The EU's 90-day moratorium on these tariffs adds to the uncertainty, with soybeans facing potential price hikes.

3. Actionable Recommendations

Diversify Supply Contracts to Mitigate Processing Risks

Given the surge in South American soybean exports to China and reduced crushing volumes in Brazil, importers in Asia, the EU, the Middle East and North Africa (MENA) region should secure diversified supply contracts with both Brazil and Argentina. This strategy ensures consistent access to soybean oil despite tightening raw bean availability and protects against further trade disruptions with the US.

Advocate for Policy Clarity to Stabilize US Supply Outlook

US industry stakeholders, including processors, biofuel producers, and exporters, should jointly advocate for clearer biofuel and trade policies. Improved regulatory transparency would help stabilize domestic crushing levels, maintain export competitiveness, and reduce the risk of price volatility linked to uncertain biodiesel mandates and trade tensions.

Sources: Tridge, Successful Farming, Bichos de Campo, Sur 24, Ukr AgroConsult, Grain Journal