.jpg)

In W18 in the wheat landscape, some of the most relevant trends included:

- Argentina's wheat area surged by 28% YoY in 2024/25, supported by favorable moisture and weather, signaling a possible return to record 2021/22 production levels.

- India leads global wheat procurement, purchasing 18.39 mmt by April 23, 2025, up 54% YoY.

- Meanwhile, Pakistan fell short of its wheat production target for the Rabi season 2024/25, achieving an estimated yield of 28.42 mmt, significantly below the target of 33.58 mmt.

- Wheat weekly prices remained stable, with Russia and the US holding at USD 0.25/kg in W18, but Ukraine’s price rose YoY, due to tight supply and the lowest harvest forecast in 13 years.

1. Weekly News

Argentina

Argentina's Wheat Sowing Projected to Rise 10% in 2024/25

In the 2024/25 season, Argentina has sown 28% more wheat than in the 2023/24 season, equivalent to 1.28 million hectares (ha). This increase suggests that the current campaign may approach the 1.8 million ha planted during the record 2021/22 season, when Argentina achieved a wheat production record of 23 million metric tons (mmt). Several factors support the 2025/26 wheat production, including excellent moisture reserves, a projected ’neutral’ winter in the Pacific, and favorable wheat/urea ratios, particularly in northeast Buenos Aires.

Egypt

Egypt's Wheat Procurement Declined 37% YoY in 2024/25

Egypt has purchased 466,266 metric tons (mt) of wheat from local farmers since the official start of the procurement season in mid-Apr-25. This figure is 37% lower year-on-year (YoY). Despite reduced wheat acreage in the 2024/25 season, the government expects to purchase 4 to 5 mmt from local producers by raising the purchase price by 10%. This will enable the country to import about 6 mmt. Typically, authorities purchase around 3.5 mmt of wheat from local farmers per season.

India

India's Wheat Procurement Up 54% in 2024/25 Season

The arrival of wheat has accelerated across India's key producing states, with government agencies purchasing over 18.39 mmt of the grain between March, 15, 2024 and April, 23, 2025. This represents a 54% YoY increase compared to 11.92 mmt procured during the same period in the 2023/24 season. Punjab leads the with 5.92 mmt producred as of April 23, 2025, compared to 3.49 mmt during the same period in the 2023/24 season. The procurement process in Punjab started late, only gaining momentum after the Baisakhi festival on April 13, 2025. However, wheat arrivals will rise in the coming days, with a target set to reach daily arrivals of 500 thousand mt. The government aims to procure 12.4 mmt from Punjab. Haryana follows with 5.66 mmt procured as of 23 April, up from 4.81 mmt in the previous season. The state's procurement target stood at 7.5 mmt.

Pakistan

Pakistan Wheat Production Misses Target in 2024/25 Rabi Season

Pakistan fell short of its wheat production target for the Rabi season 2024/25, achieving an estimated yield of 28.42 mmt from 9.1 million ha, significantly below the target of 33.58 mmt from 10.37 million ha. During the Federal Committee on Agriculture (FCA) meeting, chaired by the Federal Minister for National Food Security and Research, officials revealed that other crops have shown positive trends while wheat production declined.

United States

US Winter Wheat Conditions Worsen in W18, Spring Wheat Planting Delayed Due to Drought

United States (US) winter wheat conditions have worsened in W18, with a decline in the percentage of crops rated as excellent and a slower-than-expected heading rate. However, rainfall will provide some relief and boost growth. According to the United States Department of Agriculture's (USDA) crop progress report, spring wheat planting is behind schedule due to drought conditions in several states, with 33% of winter wheat and 49% of spring wheat currently in drought-affected areas.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W18 2024 to W18 2025)

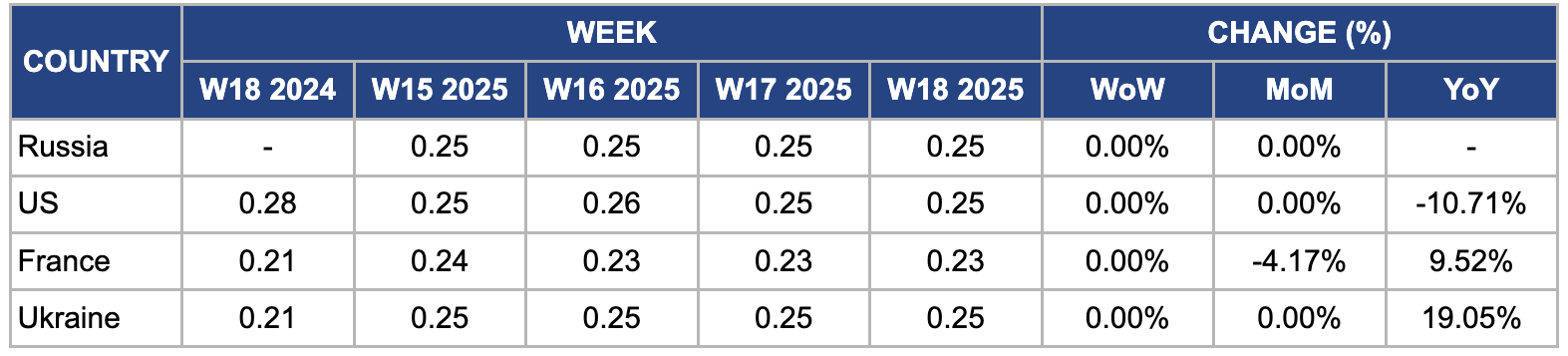

Russia

In W18, Russian FOB wheat prices held steady week-on-week (WoW) at USD 0.25 per kilogram for the fourth consecutive week. This price stability reflects the impact of government interventions, including a minimum export price floor of USD 250/mt set by the Russian Ministry of Agriculture to curb excessive exports and manage domestic inflation. Moreover, the government increased export duties by 12.2% in Mar-25, further controlling outbound wheat flows and reinforcing price stability. Russian wheat production for the 2024/25 season is expected to be strong, driven by favorable weather and improved yields in major growing regions like Krasnodar and Rostov. Despite global market volatility, Russian wheat prices have shown resilience due to stable domestic output, export quotas, and regulatory measures supporting and stabilizing the wheat export market.

United States

In W18, US FOB wheat prices remained unchanged WoW and month-on-month (MoM) at USD 0.25/kg. However, prices declined by 10.71% YoY. Weak global demand, particularly from major importers like Egypt and Türkiye, has limited US wheat sales. According to USDA data, US wheat export inspections in Apr-25 were down 6% YoY, further contributing to the price decline. Moreover, US winter wheat conditions have worsened in W18, with the percentage of crop decline rated as excellent and a slower-than-expected heading rate. However, rainfall will provide some relief and boost growth.

France

In W18, wholesale wheat prices in France remained steady WoW at USD 0.23/kg, but declined 4.17% MoM. Persistent wet weather in key production areas like Hauts-de-France and Grand Est delayed spring fieldwork, with only 80% of the planned soft wheat area planted by early Apr-25, down from 95% during the same period last year. The excess moisture has also heightened the risk of fungal diseases, casting uncertainty over yield and crop quality. Nonetheless, steady demand from North African buyers, particularly Algeria and Morocco, continues to support France's wheat export activity.

Ukraine

Ukrainian wheat prices remained unchanged WoW and MoM in W18. However, prices surged by 19.05% YoY, rising to USD 0.25/kg from USD 0.21/kg in W18 2024. This is due to tight supply as the USDA projects Ukraine’s wheat harvest for the marketing year (MY) 2025/26 at 17.9 mmt, the lowest in 13 years and 23% below last year's output. This significant decline stems from dry soil conditions during the sowing season and a reduction in planted area driven by low crop profitability.

3. Actionable Recommendations

Capitalize on Strong Sowing Momentum by Securing Export Commitments Early

With Argentina’s wheat planting area up by 28% YoY and approaching 2021/22 record levels, exporters should proactively secure forward contracts with major buyers such as Brazil, Indonesia, and Algeria. Given the favorable agronomic conditions, including excellent moisture and better input cost ratios, Argentina is poised for a rebound in wheat output. Locking in export deals early will help hedge against price volatility and strengthen Argentina’s position in international markets, mainly as global demand may rise in response to supply tightness from Pakistan and Ukraine.

Prioritize Domestic Market Stabilization Through Imports and Strategic Stocks

Pakistan is facing a 10% YoY decline in wheat production and should immediately initiate strategic wheat imports to stabilize domestic supply and prices. The government can explore Government-to-Government (G2G) deals or short-term tenders with Russia, Ukraine, or France to procure quality wheat at competitive rates. Moreover, stockpiling wheat before seasonal shortages will help avoid domestic inflationary pressures and social unrest, especially in the monsoon season when transportation can be disrupted.

Target High-Value Niche Markets Amidst Tight Supply

With Ukrainian wheat output expected to drop to a 13-year low, exporters should shift focus from volume-based trade to premium markets that pay more for quality and traceability, such as the EU, Japan, and select Gulf states. Exporters can leverage Ukraine’s track record for high-protein milling wheat and invest in certification schemes (e.g., International Organization for Standardization/ISO, Hazard Analysis and Critical Control Points/HACCP) to boost value. Targeting these markets will help compensate for reduced volumes and maintain foreign exchange earnings despite the production shortfall.

Sources: Tridge, Revista Chacra, Ukr Agro Consult