.jpg)

In W21 in the wheat landscape, some of the most relevant trends included:

- Global wheat production will grow by 1.1% YoY to 808.5 mmt.

- Meanwhile, US output will fall to 52.3 mmt, raising US ending stocks to 25.1 mmt and slightly lowering farmgate prices to USD 5.30/bushel.

- China anticipates a strong harvest due to favorable weather and improved management.

- Amid adverse weather, Türkiye’s production may drop to 18.65 mmt, below the USDA’s steady forecast of 19 mmt for 2025/26.

- Wheat prices rose WoW in the US and France due to delayed planting progress and strong market sentiment. Prices remained stable in Russia at USD 0.25/kg, supported by ample stocks and steady export volumes. Ukrainian prices fell MoM on rising supply and weaker export demand.

1. Weekly News

Global

Wheat Market Stable Despite US Production Drop and China’s Rising Imports from Other Suppliers

The United States Department of Agriculture (USDA) projected a 1.5% year-on-year (YoY) reduction in United States (US) wheat planting area and a production decline to 52.3 million metric tons (mmt) for 2025/26. US ending stocks will rise to 25.1 mmt, while the average farmgate price may drop slightly to USD 5.30 per bushel. Globally, wheat production is forecast to grow by 1.1% YoY to 808.5 mmt, with final stocks reaching 265.7 mmt. China, facing a heat wave in key growing regions, imported 400 thousand to 500 thousand metric tons (mt) of wheat from Australia and Canada, continuing its annual import trend of around 11 mmt. However, ongoing trade tensions have limited China’s purchases of US wheat, contributing to recent declines in futures prices on the Chicago Board of Trade (CBOT).

China

China Begins Wheat Harvest in Southwest with Strong Yield Outlook

Wheat harvesting has commenced in China’s southwestern provinces of Sichuan, Yunnan, and Guizhou, with expectations of a strong yield due to favorable weather and improved crop management, including high-yield technologies application. In Sichuan, winter wheat is in good condition with minimal pest or disease pressure, while field surveys in Yunnan and Guizhou also show positive crop development. Wheat experts from the Ministry of Agriculture and Rural Affairs noted a significant increase in ear numbers, a slight rise in grains per ear, and stable grain weight, all contributing to a projected overall yield increase. With large-scale harvesting to follow soon, China is on track for a stable or improved wheat harvest.

Russia

Russian Wheat Exports Dropped to Record Low Amid Global Competition and Falling Domestic Sales

Russian wheat exports will fall to a record low of 1.8 mmt in May-25, down from 2.4 mmt in Apr-25 and 1.9 mmt in Mar-25. This decline signals a broader slowdown in Russian wheat sales domestically and internationally. During Q1-25, farmers only sold 7.9 mmt of wheat on the domestic market, a 26% drop from 10.7 mmt the previous year. Wheat stocks in southern Russia, a key export region, fell 49% YoY to 4.7 mmt. However, analysts believe that existing stock levels remain substantial and do not foresee a rise in domestic wheat prices. The export slowdown is due to heightened global competition, particularly from countries like India, with increased production and potential logistical challenges.

Türkiye

Türkiye Cuts Wheat Harvest Forecast to 18.65 MMT Due to Spring Weather Extremes

Adverse weather anomalies, including a prolonged drought in Mar-25 followed by heavy rainfall and unusually low temperatures in Apr-25, may reduce Türkiye’s wheat production in the 2024/25 season. The National Grain Council (UHK) forecasted harvest at no more than 18.65 mmt, down from a previous estimate of 20 mmt. Despite these unfavorable conditions, Turkish farmers have expanded wheat acreage from 6.8 million to 7.6 million hectares (ha) over the past three years. Meanwhile, USDA experts projected Türkiye’s wheat production for the 2025/26 marketing year (MY) at 19 mmt, maintaining the current season’s level but 2 mmt below the 2023/24 figure.

United States

Winter Wheat Planting Ahead of Five-Year Average but Behind 2024

The USDA reported in its Weekly Weather and Crop Bulletin released on May 20, that farmers had sown 64% of the country’s winter wheat crop. This planting progress is 6% above the five-year average but 3% below the same period last year. As of May 18, 52% of the winter wheat crop was rated in good to excellent condition, a 2% decline from the previous week but still 3% higher than the 2024 average. In Kansas, the largest winter wheat producer, 49% of the crop received good ratings.

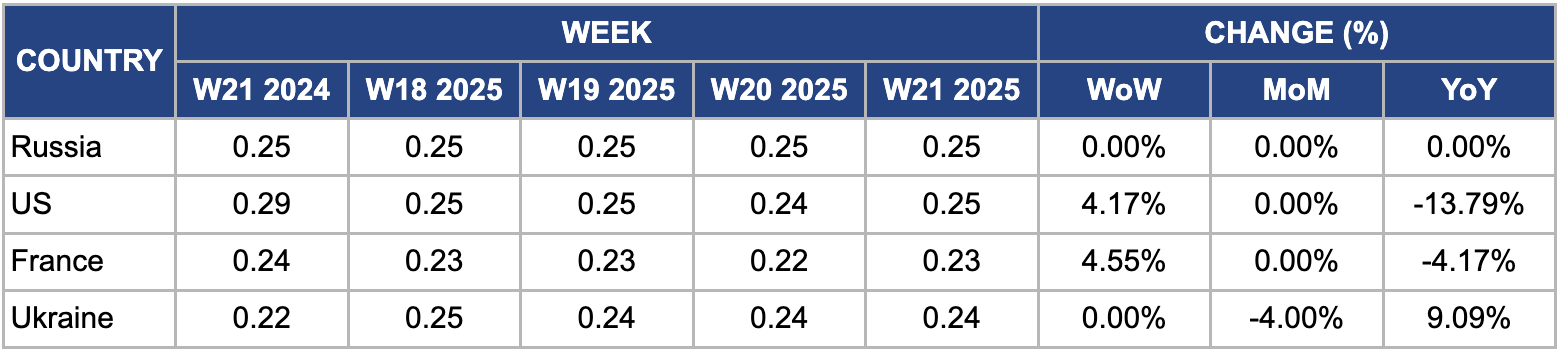

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W21 2024 to W21 2025)

Russia

In W21, Russian FOB wheat prices stood at USD 0.25 per kilogram (kg), remaining steady week-on-week (WoW), month-on-month (MoM), and YoY for the fourth consecutive week. This is despite Russian wheat exports predicted to fall to a record low of 1.8 mmt in May-25, down from 2.4 mmt in Apr-25 and 1.9 mmt in Mar-25. This decline results from reduced sales on both international and domestic markets, with farmers selling 26% less wheat in the Q1-25 compared to the same period last year. Despite large wheat stocks, domestic prices will rise. However, decreased exports could push prices higher in regions dependent on Russian grain, such as the Middle East and North Africa, due to increased competition and possible logistical challenges.

United States

In W21, US FOB wheat prices rose 4.17% WoW, reaching USD 0.25/kg from USD 0.24/kg in W20 due to planting progress. According to USDA, farmers planted 64% of the country's winter wheat crop by the end of the week, marking a 6% increase compared to the five-year average but remaining 3% lower YoY. The USDA bulletin also reported that as of May 18, 52% of the winter wheat crop was rated in good to excellent condition, representing a slight 2% decline WoW but still 3% above the 2024 average.

France

In W21, wholesale wheat prices in France rose 4.55% WoW to USD 0.23/kg from USD 0.22/kg. This is driven by improved crop conditions, with 76% of the 2025 wheat rated good or excellent compared to 65% last year, boosting the supply outlook. Moreover, while exports to traditional markets like Algeria and China remained subdued, increased shipments to Morocco and efforts to diversify export destinations helped stabilize demand. A weaker euro (EUR) enhanced French wheat competitiveness internationally, supporting the price increase amid a more balanced supply-demand environment.

Ukraine

In W21, Ukrainian wheat prices remained unchanged WoW but declined 4% MoM to USD 0.24/kg. The new harvest increased supply, causing the monthly price drop. Better weather conditions in key growing regions improved crop development, which raised availability. At the same time, traditional buyers reduced their export demand due to global market uncertainties and competition from other wheat exporters, putting downward pressure on prices. Rising supply combined with cautious demand led to a moderate monthly price decline.

3. Actionable Recommendations

Promote Domestic Wheat Utilization Through Processing and Value Addition

The US and Russia, which produce surplus wheat, should actively expand domestic wheat utilization to reduce growing inventories and prevent farmgate prices from falling. Developing processing industries such as flour mills, pasta factories, and snack food manufacturers can significantly boost internal demand for wheat. For example, the USDA projects that US wheat ending stocks will rise to 25.1 mmt despite a slight decline in production and planted area, which may keep farmgate prices low. Instead of relying solely on export markets to absorb the surplus, policymakers and agribusinesses must focus on building stronger domestic value chains. They can do this by offering tax incentives to processors using locally produced wheat and supporting wheat-based animal feed production. By strengthening domestic consumption and adding value, these countries can stabilize the market, support rural economic growth, and foster more sustainable development in the wheat sector.

Invest in Climate-Resilient Wheat Varieties and Regional Agronomic Adaptation

With adverse weather increasingly disrupting wheat production in regions like Türkiye, the US, and Russia, stakeholders must urgently invest in climate-resilient agricultural strategies. National agricultural research agencies, private seed companies, and extension services need to collaborate closely to develop and deploy wheat varieties that tolerate drought, cold snaps, and excessive rainfall. For instance, weather anomalies in Mar-25 and Apr-25 have reduced Türkiye’s wheat harvest projections despite an expanded planted area. Farmers can mitigate such setbacks by adopting improved wheat varieties alongside region-specific agronomic practices, such as enhanced soil moisture conservation and adjusted sowing calendars. Real-time monitoring through satellites and drones can further enable early risk detection and timely interventions. Beyond these biological and technological solutions, governments should implement regional contingency plans that include crop insurance schemes and strategic wheat reserves to shield farmers and safeguard national food security from climate-induced shocks.

Expand and Diversify Wheat Export Markets

Wheat-exporting countries like the US, Russia, and Ukraine must actively diversify their export markets to reduce vulnerability. Relying heavily on a limited number of key importers, such as China, which continues to avoid US wheat due to trade tensions, exposes exporters to risks during diplomatic conflicts or market saturation. Exporters can build a broader customer base by strategically expanding into emerging regions like Southeast Asia, Sub-Saharan Africa, and Latin America. They can achieve this through trade missions, bilateral agreements, and participation in regional food security initiatives that foster stable, long-term grain partnerships. Furthermore, exporters should customize their offerings by promoting wheat grades and quality certifications tailored to the specific needs of new markets, including baking or animal feed industries. Strengthening diplomatic engagement and commercial outreach through embassies and agricultural attachés will help exporters reduce dependence on traditional buyers and withstand future market disruptions.

Sources: Tridge, Agrolink, Grain Trade, Sinor, UkrAgroConsult