In W22 in the soybean oil landscape, some of the most relevant trends included:

- Bolivia is experiencing a severe refined soybean oil shortage, with prices up nearly 60% YoY, driven by alleged hoarding and speculation despite adequate domestic production. Government interventions include export restrictions, border controls, and tax-free imports, though supply chain inefficiencies persist.

- Venezuela’s 2024 soybean oil imports surged due to economic stabilization and rising demand. However, a projected GDP decline and inflation in 2025 may reduce agricultural imports by 10 to 15%, though US exports may remain resilient due to competitive pricing and proximity.

- Argentina’s soybean oil prices fell by 4.90% WoW in W22, pressured by lower US futures linked to biofuel policy uncertainty. Improved harvest conditions may support market stabilization as Argentina maintains its lead in global exports.

- US soybean oil prices declined 1.83% WoW in W22, tempered by favorable planting conditions and ample South American supply. Nonetheless, medium-term support is likely from rising global demand, constrained alternative oil supplies, and a projected record soybean harvest in 2025/26.

1. Weekly News

Bolivia

Bolivia's Refined Soybean Oil Shortage Worsens as Rationing, Export Pressure, and Alleged Speculation Intensify

Bolivia faces a severe shortage of refined soybean oil, with retail prices reportedly rising by nearly 60% year-on-year (YoY) amid widespread rationing and long consumer queues. Despite sufficient domestic soybean production, the government attributes the crisis to speculation and hoarding by producers and merchants.

With 70% of refined oil output allocated to exports, the government has intensified anti-profiteering measures, enhanced border controls, and authorized tax-free imports of oil inputs through year-end. The state-run Food Production Support Company (EMAPA) has maintained subsidized prices but restricted sales, contributing to growing public discontent. This crisis echoes a similar shortage in late 2024 and underscores persistent structural issues in Bolivia’s edible oil supply chain.

Venezuela

Venezuelan Soybean Oil Imports Rose in 2024, but 2025 Outlook Weakens

In 2024, Venezuelan soybean oil imports rose significantly in both volume and value, supported by improved economic conditions, stable inflation, and increased demand. The United States (US), Venezuela's second-largest agricultural supplier, recorded a notable rise in soybean oil exports, driven by competitive pricing and rising feedstock needs.

Soybean oil ranked among Venezuela's top ten agricultural imports by both volume and value, reflecting its strategic role in food processing and biofuel use. However, the outlook for 2025 is less optimistic. A projected 2 to 4% Gross Domestic Product (GDP) contraction, triple-digit inflation, and currency depreciation are expected to reduce overall agricultural imports by 10 to 15%. While consumer goods will be most affected, imports of bulk and intermediate products, including soybean oil, will face moderate declines. Nonetheless, the US is expected to retain its strong position due to price competitiveness, quality, and proximity, particularly in feed-related commodities like soybean oil.

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W22 2024 to W22 2025)

.png)

Argentina

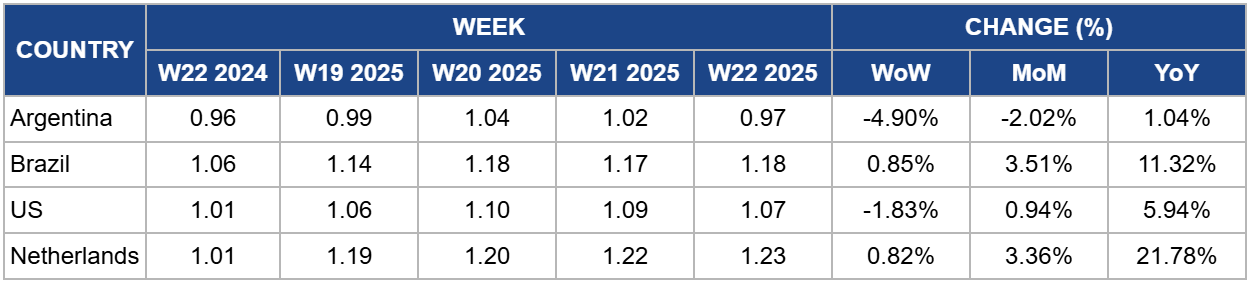

In W22, Argentina's soybean oil prices declined by 4.90% week-on-week (WoW) to USD 0.97 per kilogram (kg) despite remaining 1.04% higher YoY. The weekly decline reflects global market pressures, particularly falling US soybean oil futures, which have been affected by uncertainty surrounding US biofuel tax credit policies. Domestically, despite harvest delays from prolonged rains, prices softened as improved weather forecasts signal a likely acceleration in harvest activity. With 74.3% of the national crop harvested and dry, cold weather aiding field conditions, Argentina's role as the world’s top soybean oil exporter could support market stabilization in the near term.

Brazil

In W22, Brazil's soybean oil prices rose by 0.85% WoW to USD 1.18/kg, experiencing an increase of 11.32% YoY from USD 1.06/kg. This sustained price strength is driven by robust international demand, particularly due to expectations of increased US biodiesel consumption, which has supported global soybean oil markets. Brazil has benefited from this trend, with Q1-2025 soybean oil exports up 30% YoY to 503,000 metric tons (mt). Tight global supplies, amplified by Argentina's weather-related harvest delays, further bolstered Brazil's export position. While near-term prices may remain elevated, rising domestic production and growing stocks could temper further gains in the medium term.

United States

US soybean oil prices declined by 1.83% WoW to USD 1.07/kg in W22, but remaining 5.94% higher YoY. The decline reflects near-term pressure from favorable US planting conditions and ample South American supplies, which have weighed on overall market sentiment.

Despite this setback, US soybean oil remains underpinned by firm global demand and limited availability of alternative vegetable oils. The Food and Agriculture Organization (FAO) reported a 2.3% month-on-month (MoM) increase in global vegetable oil prices in Apr-25, driven by strength in soybean and rapeseed oil. Nonetheless, more competitive Argentine export prices, down 3% MoM, may cap US price gains in the short term. The United States Department of Agriculture (USDA) forecasts record global soybean production and rising crush volumes in 2025/26. These factors, combined with a potential recovery in biodiesel demand and improved trade conditions, could provide medium-term support for US soybean oil prices.

Netherlands

In W22, soybean oil prices in the Netherlands rose by 0.82% WoW to USD 1.23/kg, up 21.78% YoY. The increase is driven by steady export demand, particularly from the United Kingdom (UK), which sourced 80% of its soybean oil imports from the Netherlands in 2024. This trend is reinforced by broader European Union (EU) oilseed market dynamics, such as high rapeseed oil prices and relatively weak sunflower oil prices have shifted demand toward soybean oil. With UK consumption expected to grow through 2035 and Dutch exports rising by 5.3% annually since 2013, near-term prices are likely to remain supported. However, expanded South American supply may moderate price growth over the longer term.

3. Actionable Recommendations

Enhance Regional Sourcing to Alleviate Domestic Shortages

Bolivian importers and distributors should strengthen procurement from nearby low-cost suppliers such as Argentina and Paraguay, where soybean oil prices are relatively competitive and supply is stable. Leveraging regional proximity can reduce logistics costs and ensure quicker turnaround during shortages, especially while domestic bottlenecks persist.

Capitalize on Stable US-Venezuelan Trade Links Amid Import Slowdown

With Venezuela’s bulk soybean oil imports expected to face moderate reductions in 2025 due to economic headwinds, US exporters should prioritize long-term supply agreements with feed and food processors to secure market share. Focused efforts on maintaining price competitiveness and timely delivery will help mitigate demand contraction and sustain volume flows.

Develop Targeted Risk Mitigation Strategies in Response to Policy-Driven Market Volatility

Exporters and importers across the Americas should adopt hedging tools such as futures and forward contracts to manage exposure to price volatility caused by shifting biofuel policies, Argentine tax structures, and South American weather disruptions. Flexibility in contract terms and diversified sourcing will be essential to maintain supply chain stability.

Sources: Tridge, Ukr AgroConsult, El Sitio Avícola, Successful Farming, Infobae, Agro Sector