.jpg)

In W22 in the wheat landscape, some of the most relevant trends included:

- Australia’s 2024/25 wheat production will decline 10% YoY to 30.6 mmt due to dry conditions and reduced planted area. Exports to China have sharply dropped, and increased competition from Russian supplies is pressuring Australia’s exports and prices.

- China’s wheat output will fall 5% YoY in 2025 to 133 mmt, the lowest since 2018, due to drought and heat stress. Despite this, imports remain weak, hitting a seven-year low in early 2025 amid ample stockpiles and geopolitical tensions.

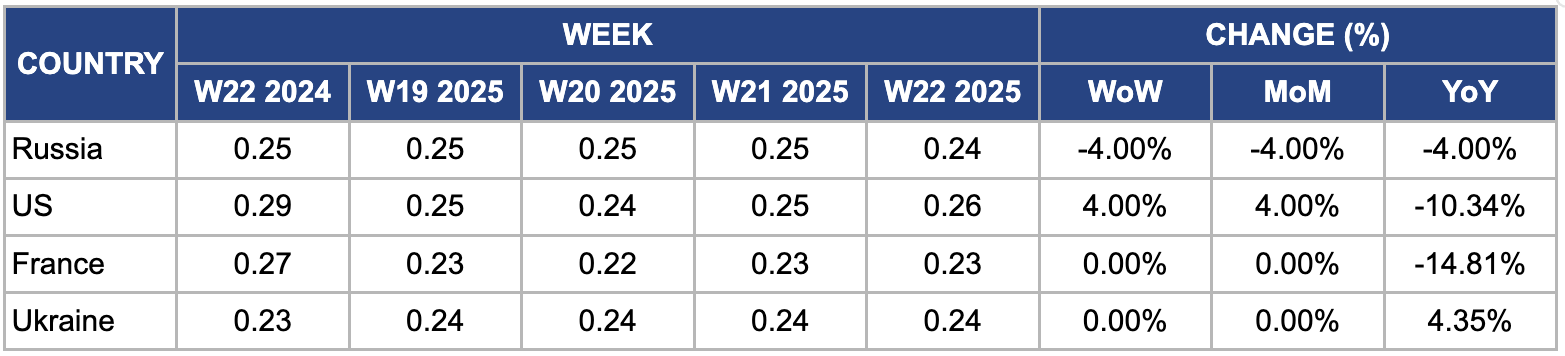

- In W22, Russian wheat FOB prices fell WoW, MoM, and YoY on expectations of a record harvest and export quotas boosting local supply. In contrast, US FOB wheat prices rose WoW and MoM, supported by delayed harvests and strong global demand. France’s wheat prices remained stable WoW and MoM but declined YoY due to improved crop conditions and weaker export demand. Ukrainian wheat prices increased YoY, reflecting a lower production forecast.

1. Weekly News

Australia

Australia Faces Wheat Glut in 2024/25 as Chinese Demand Falls and Russian Competition Grows

Australia will likely end the 2024/25 season with significantly higher wheat inventories as reduced Chinese imports and competition from Russian supplies pressure exports and drag down prices. Between Oct-24 and Mar-25, Australia shipped just 546 thousand metric tons (mt) of wheat to China, down sharply from 2.9 million metric tons (mmt) in 2023/24 and 4.4 mmt in 2022/23. With global supplies remaining abundant and Russia maintaining strong exports even during its usual lean season, Australia struggles to secure export opportunities ahead of the Northern Hemisphere harvests, which will flood the market with cheap grain. Analysts warn that Australia may have to conduct a fire sale of stored wheat to clear space for the next harvest in Q4, which could further pressure benchmark Chicago futures trading near four-year lows. If exports remain sluggish, Australia could carry over 5 to 6 mmt from last season’s crop.

Australia’s 2024/25 Wheat Output Forecast Down 10% Due to Dry Conditions and Reduced Planting

According to the Australian Agriculture Ministry, Australia will produce 30.6 mmt of wheat in the 2024/25 season, a 10% decline from the 2023/24 season, as dry conditions across key cropping regions reduce output. Low soil moisture in southern New South Wales, Victoria, South Australia, and the northern wheat belt of Western Australia led some farmers to cut planted areas, and many dry-sown crops now depend on June rainfall for germination and establishment. In contrast, Queensland, northern New South Wales, and southern Western Australia are experiencing more favorable conditions, with forecasts pointing to above-average winter rainfall. Australian farmers will plant 12.6 million hectares (ha) of wheat in the 2024/25 season, down 3% year-on-year (YoY).

China

China’s 2025 Wheat Output to Hit 6-Year Low Due to Drought

China's wheat production is forecasted to decline by 5% YoY in 2025 due to drought and extreme heat stressing crops in key northern regions like Henan and Shaanxi. This brings output down to 133 mmt, the lowest since 2018. This would represent a notable decline from the 2024 record of 140 mmt. However, ample stockpiles and weak domestic demand may cushion the domestic market from key disruptions. Still, the drop challenges Beijing’s food security agenda, pushing authorities to reassess import strategies, particularly amid ongoing geopolitical tensions and the recent imposition of a 15% tariff on United States (US) wheat. Between Jan-25 and Apr-25, imports have already fallen to a seven-year low of just over 1 mmt. As climate volatility worsens from floods two years ago to the current drought, China faces growing threats to wheat supply stability. With wheat remaining a key dietary staple and a critical feed grain, these climate risks are becoming increasingly urgent for national planning.

Türkiye

Türkiye Lowers 2024/25 Wheat Forecast Amid Weather Anomalies

Adverse weather anomalies, including a prolonged drought in Mar-25 followed by heavy rainfall and unusually low temperatures in Apr-25, may reduce Türkiye’s wheat production in the 2024/25 season. The National Grain Council (UHK) lowered its harvest forecast to no more than 18.65 mmt, down from a previous estimate of 20 mmt. Despite these unfavorable conditions, Turkish farmers have expanded wheat acreage from 6.8 million to 7.6 million ha over the past three years. Meanwhile, United States Department of Agriculture (USDA) experts projected Türkiye’s wheat production for the 2025/26 marketing year (MY) at 19 mmt, maintaining the current season’s level but 2 mmt below the 2023/24 figure.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W22 2024 to W22 2025)

Russia

In W22, Russian FOB wheat prices dropped 4% week-on-week (WoW), month-on-month (MoM), and YoY to USD 0.24 per kilogram (kg). This decline resulted from expectations of a record 2025 wheat harvest, projected at around 88 mmt, supported by favorable weather conditions and expanded planting areas. Moreover, government-imposed export quotas limited shipments to 10.6 mmt from Feb-25 to Jun-25 to protect domestic supply, increasing local availability and putting downward pressure on prices. A stronger ruble also made Russian exports less competitive, while rising production and logistical costs squeezed exporter profits.

United States

In W22, US FOB wheat prices rose 4% WoW and MoM to USD 0.26/kg, driven by concerns over tighter supplies amid delayed winter wheat harvest progress due to wetter-than-average conditions in key producing states like Kansas and Oklahoma. Furthermore, strong global demand, especially from importers seeking alternative sources amid geopolitical uncertainties, supported price gains. Limited export competition from other major producers experiencing production challenges also helped bolster US wheat prices during this period.

France

In W22, wholesale wheat prices in France remained unchanged WoW and MoM but declined significantly by 14.81% YoY to USD 0.23/kg. This weekly price stability was due to a reduced wheat production estimate of 25.78 mmt for the 2024/25 season, reflecting slightly lower yields of around 6.15 mt/ha due to unfavorable weather. However, the price dropped 14.81% YoY as French wheat exports outside the European Union (EU) were forecasted at just 3.5 mmt, the lowest in decades due to weaker demand from key buyers like Algeria and China. This was coupled with stronger competition from major exporters such as Russia flooding the market with cheaper wheat. These factors increased supply pressure while dampening export opportunities, causing a significant YoY price drop.

Ukraine

In W22, Ukrainian wheat prices remained unchanged WoW and MoM but increased 4.35% YoY to USD 0.24/kg. This YoY increase is mainly due to a lower 2025 production forecast of around 21.5 mmt, down from approximately 23 mmt in 2024, as ongoing geopolitical tensions and adverse weather conditions limited planting and harvesting. Moreover, export volumes faced logistical constraints, with shipments estimated at 15 mmt for 2025, slightly below previous years, while strong global demand and tight supplies from other origins bolstered Ukrainian wheat prices compared to 2024.

3. Actionable Recommendations

Diversify Export Markets and Strengthen Trade Partnerships

Given the significant reduction in wheat exports to China, Australian exporters face increasing pressure to find alternative markets. By diversifying their export destinations, they can reduce vulnerability to geopolitical tensions and fluctuating demand from one country. This involves conducting market research to identify emerging buyers in regions such as Southeast Asia, the Middle East, and Africa, where demand for wheat is growing. Exporters can engage in targeted trade missions and build strategic relationships with importers and distributors in these regions. Moreover, improving logistics such as port efficiency and transportation networks can lower costs and delivery times, making Australian wheat more competitive. Governments and industry bodies can support these efforts by providing export facilitation services, trade financing, and promotional campaigns.

Invest in Climate-Resilient Wheat Varieties and Agronomic Practices

Climate volatility, including droughts and heat stress, threatens wheat yields in major producing countries like Australia, China, and Türkiye. To mitigate these risks, China must invest in drought- and heat-tolerant wheat varieties such as Bainong 207, Zhengmai 7698, and Shannong 20. Agricultural research institutions and seed companies should accelerate breeding programs and actively distribute these resilient seeds to farmers. Farmers can adopt complementary agronomic practices like precision irrigation to optimize water use, conservation tillage to maintain soil moisture, mulching to reduce evaporation, and adjusting planting schedules based on weather forecasts to enhance crop resilience. Extension services and training programs must expand to support farmers in effectively implementing these innovations. By taking these actions, China will stabilize wheat production, reduce vulnerability to weather shocks, and secure food supply and farmer incomes.

Optimize Storage and Supply Chain Management to Avoid Price Depressions

Australia faces the risk of carrying over wheat inventories and potentially conducting “fire sales” to clear storage for new harvests, which can depress prices and harm farmers’ incomes. To address this, the government and private sector must invest in modern, high-capacity grain storage facilities equipped with temperature and humidity controls to preserve grain quality for longer. Improved storage infrastructure will enable farmers and traders to manage supply flows more effectively, allowing them to time their sales strategically and avoid flooding the market. Moreover, stakeholders should strengthen supply chain coordination by enhancing communication and logistics between farmers, processors, exporters, and transporters to reduce bottlenecks, post-harvest losses, and delays. Authorities and industry groups should also consider implementing grain reserve policies or buffer stocks, either publicly or privately managed, to stabilize prices during periods of oversupply and market volatility. These measures will help protect farmers’ revenues, maintain buyer confidence, and ensure steady export volumes, supporting the long-term sustainability of Australia’s wheat sector.

Sources: Tridge, Miller Magazine, Reuters, The Edge Malaysia, Ukr Agro Consult