In W23 in the maize landscape, some of the most relevant trends included:

- IMEA increased the 2024/25 Brazilian corn area estimate to 7.13 million ha, supported by favorable late-season rains. Total production is projected at 50.38 mmt, a 3.05% increase from the May-25 forecast and 6.79% YoY, reflecting improved crop conditions and a more optimistic outlook.

- Meanwhile, Indonesia launched its first corn exports from West Kalimantan. It aims to export 27 thousand mt in Jun-25, signaling expanding regional trade opportunities.

- In W23, US corn prices dropped both WoW and MoM, driven by accelerated planting progress, strong crop conditions, and competition from South American corn, particularly Brazil’s Safrinha crop. Similarly, Brazil’s wholesale maize prices declined WoW and MoM amid robust production forecasts. Argentina’s maize prices dropped, pressured by favorable crop prospects but hampered by logistical export challenges.

- Ukraine’s 2024/25 corn exports decreased by 29.2% YoY to 20.58 mmt due to competitiveness issues and logistical constraints. Ukrainian maize prices softened MoM, while export volumes eased from 2 mmt in May-25 to 1 mmt in Jun-25.

1. Weekly News

Brazil

Mato Grosso Corn Outlook Upgraded for 2024/25 on Improved Weather and Yields

The Mato Grosso Institute of Agricultural Economics (IMEA) raised area and productivity projections for the 2024/25 corn harvest in Mato Grosso. The cultivated area will reach 7.13 million hectares (ha), 0.25% higher than the May-25 estimate and 4.85% year-on-year (YoY). Productivity was also increased to 117.74 bags/ha, a 2.79% increase over the May-25 estimate, driven by favorable weather and consistent rains through late May-25. Even fields planted outside the optimal window benefited from rainfall, supporting crop development. As a result, total production is projected at 50.38 million metric tons (mmt), up 3.05% from the May-25 forecast and 6.79% from 2023/24. The new productivity estimate is 1.86% higher than the previous season, reflecting a more optimistic outlook for Mato Grosso’s corn crop.

Indonesia

Indonesia Launches First Corn Export from West Kalimantan to Malaysia in Milestone Event

On June 5, 2025, Indonesia launched its first corn export from Bengkayang district, West Kalimantan, to Malaysia, marking a milestone for the region’s agricultural sector. Accompanied by key officials, the President oversaw the shipment to Kuching and inaugurated the Pangan Merah Putih warehouse and drying plant, which can store 5 thousand metric tons (mt) and dry up to 300 mt of corn daily. This facility aims to boost regional corn processing and distribution. The initiative is part of Indonesia’s broader strategy to tap into international markets, with 27 thousand mt of corn scheduled for export on Jun-25. Building on surplus production recorded in 2022, the move strengthens economic ties with Malaysia, enhances food security, and empowers local farmers.

India

Punjab Launches Incentive Scheme to Shift from Paddy to Maize on 10 Thousand HA

The Punjab government in India will provide financial incentives to farmers to grow maize instead of paddy, aiming to boost maize production amid rising demand driven by the Indian government’s ethanol blending policy. With petrol now allowed to be blended with 20% ethanol, maize has gained strategic importance as a feedstock. As part of a pilot initiative, the state plans to shift 10 thousand ha of rice cultivation to maize across Sangrur, Bhatinda, Pathankot, Gurdaspur, Jalandhar, and Kapurthala. To support the transition, authorities will reward approximately USD 200/ha of maize annually.

Ukraine

Ukraine’s 2024/25 Grain Exports Down 22.5% YoY as Corn Shipments Drop Sharply

As of June 2, Ukraine exported 38.31 mmt of 2024/25 season grain and pulses, marking a decline of 8.65 mmt or 22.5% YoY, according to the Ministry of Agrarian Policy and Food of Ukraine (MAPFU). Corn exports reached 20.58 mmt, down by 6.02 mmt or 29.2% YoY, reflecting a significant contraction in export volumes compared to the previous year.

United States

US Corn Planting Nears Completion with 93% Planted

As of early Jun-25, the United States Department of Agriculture (USDA) reported that United States (US) corn planting reached 93% of the intended area, 3% ahead YoY and consistent with the five-year average. Moreover, 78% of the crop had already emerged, up 6% YoY. Regarding crop quality, 69% of the planted corn was rated in good to excellent condition. Iowa, the top-producing state, showed a strong performance, where 84% of the crop fell into this category.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

* Varieties: US (feed grade), all others (overall average)

Yearly Change in Maize Pricing Important Exporters (W23 2024 to W23 2025)

* Varieties: US (feed grade), all others (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

United States

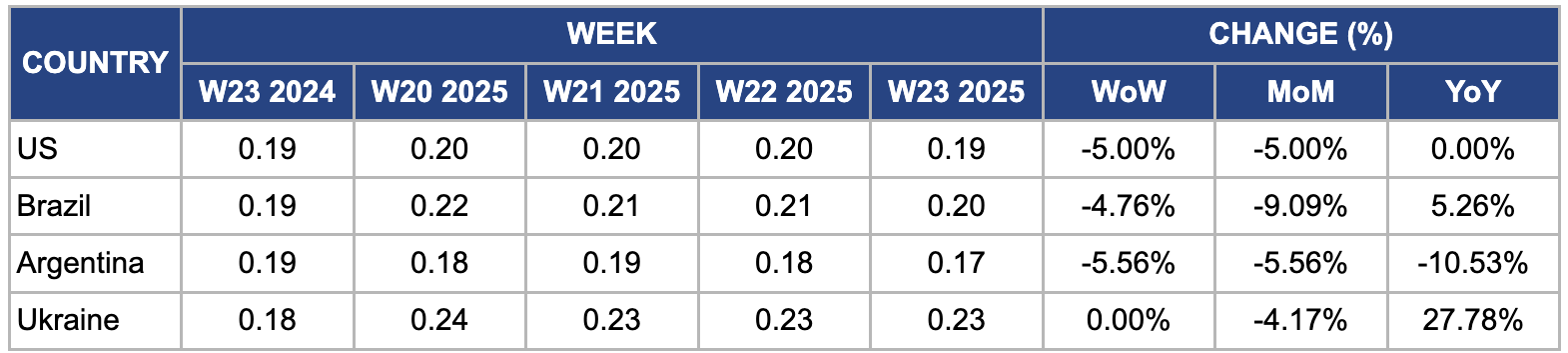

In W23, US corn prices declined 5% week-on-week (WoW) and month-on-month (MoM) to USD 0.19 per kilogram (kg), mainly due to favorable weather conditions accelerating planting progress and supporting strong early crop development. By early Jun-25, planting in key states like Iowa and Illinois was nearly complete, with emergence rates ahead of the five-year average and over 80% of the crop rated good to excellent. The prospect of a larger 2025 harvest, driven by expanded acreage in major producing regions like Illinois, where corn plantings are projected to rise to 11.1 million acres, has further eased supply concerns. Moreover, sluggish export demand and competition from South American corn, particularly Brazil’s Safrinha crop, have weighed on US prices, contributing to the recent decline.

Brazil

In W23, Brazil’s wholesale maize prices declined 4.76% WoW and 9.09% MoM to USD 0.20/kg, driven primarily by strong production prospects and delayed harvesting in key second-crop (Safrinha) regions. Ongoing rainfall and cooler temperatures have slowed harvest progress, especially in Mato Grosso do Sul and Paraná, where only about 2% of the Safrinha area was harvested by late May-25. The first-season crop is nearly complete, with 80% harvested. The Brazilian supply outlook remains robust, as National Supply Company (CONAB) raised its 2024/25 total corn production forecast in May-25 to 126.8 mmt, up 2.13 mmt from Apr-25.

Argentina

In W23, improved weather conditions across key growing regions such as Buenos Aires and Córdoba enhanced crop development. This boosted production prospects, causing Argentine maize prices to decline by 5.56% WoW and MoM to USD 0.17/kg. The Buenos Aires Grain Exchange (BAGE) projected that Argentina would produce approximately 54 mmt of maize in 2025, slightly up from 52.5 mmt in 2024, due to favorable rainfall and soil moisture levels. Meanwhile, increased global maize supply from competitors like Brazil and the US and logistical challenges hampering Argentine exports through key ports reduced export demand and further pushed prices down.

Ukraine

In W23, Ukrainian EXW maize prices held steady WoW but declined by 4.17% MoM, dropping to USD 0.23/kg from USD 0.24/kg in W20. Improved weather conditions in key producing regions boosted crop development and eased earlier concerns about yield losses. Recent agricultural reports projected that farmers would expand Ukraine’s 2025 maize harvest area by approximately 2% YoY, pushing production forecasts to around 39 mmt. Moreover, improved export logistics and increased throughput at Black Sea ports have enabled exporters to ship higher volumes, which enhanced domestic supply availability. However, the Ukrainian Agrarian Council (UAC) reported that corn exports would fall to 1 mmt in Jun-25, down from 2 mmt in May-25, as Ukraine-origin corn remains uncompetitive compared to US supplies. Ukraine, a traditional corn producer, and exporter, is expected to export around 22 mmt in the 2024/25 season.

3. Actionable Recommendations

Promote Climate-Resilient Corn Cultivation Practices in Mato Grosso to Sustain Yield Growth

With Mato Grosso’s 2024/25 corn productivity and area projections revised upward due to favorable weather, local agricultural extension agencies and input suppliers should accelerate the promotion of climate-smart practices such as optimized planting windows, improved water management, and integrated pest control. For example, farmers could adopt precision planting and drought-tolerant hybrid varieties that capitalize on consistent rains to safeguard yields against potential dry spells. Extension programs could use weather forecast data to help farmers adjust planting schedules dynamically, maximizing the benefits of late-season rainfall. These measures would sustain Mato Grosso’s productivity gains, support higher production forecasts, and strengthen Brazil’s position as a leading corn exporter.

Expand Corn Export Infrastructure and Market Diversification in Indonesia’s Emerging Regions

Following the inauguration of Indonesia’s first corn export from West Kalimantan, stakeholders, including government agencies and agribusiness firms, should scale up investments in regional post-harvest infrastructure, such as warehouses and drying facilities, across other surplus production zones. Building on the success of the Pangan Merah Putih facility, developing additional storage and processing hubs with capacities tailored to local surpluses will reduce post-harvest losses and enhance grain quality. Furthermore, exporters should actively explore diversified international markets beyond Malaysia to mitigate trade risks and expand demand. For example, joint public-private initiatives could promote Indonesian corn in Association of Southeast Asian Nations (ASEAN) countries with growing feed and ethanol sectors, enhancing farmers’ incomes and food security.

Facilitate Maize Transition and Farmer Support Programs in India’s Punjab to Meet Ethanol Demand

To meet rising domestic maize demand driven by India’s ethanol blending policy, Punjab’s government, and agri-input companies should streamline farmer incentives and support services for the planned 10 thousand ha shift from paddy to maize cultivation. Practical actions include timely disbursement of the USD 200/ha subsidy, access to quality maize seeds and fertilizer packages optimized for regional conditions, and extension services on crop management for first-time maize growers. Establishing forward contracts with ethanol producers and feed mills would further reduce market uncertainty and encourage sustained maize cultivation. This approach would improve maize supply reliability, lower paddy water footprint, and align with India’s energy and agricultural sustainability goals.

Sources: Tridge, Agrolink, Grain Trade, UkrAgroConsult