In W23 in the orange landscape, some of the most relevant trends included:

- In Brazil, orange production for the 2025/26 season is estimated at 314.6 million 40.8-kg boxes. Improved fruit quality is anticipated, and most contracts are expected to be finalized from mid-Jun-25 onward.

- Orange production in India reached 10.6 mmt in 2025. Key contributions from Maharashtra and Madhya Pradesh solidified its position as the second-largest global producer.

- Spain’s 2025 orange harvest ended early due to rainfall-related yield losses, but strong demand and limited supply helped maintain high prices throughout the season.

1. Weekly News

Global

Top Global Orange Producers in 2025 Led by Brazil, India, and China

In 2025, global orange production totaled approximately 76.41 million metric tons (mmt), with Brazil, India, and China together contributing nearly 45.4% of the supply. Brazil led with around 16 mmt, mainly from São Paulo, and remained dominant in global orange juice exports, accounting for about 60% of the total. India followed with 10.6 mmt, particularly from Maharashtra and Madhya Pradesh, where Nagpur oranges are a key variety. China produced 7.5 mmt, focusing on meeting strong local demand with cultivation centered in Jiangxi and Hunan. The United States (US) ranked fourth with 4.8 mmt, splitting production between juice-focused Florida and fresh-market California, known for Navel and Valencia oranges. Mexico, at 4.2 mmt, concentrated in Veracruz, also plays a significant role, especially in juice exports. Collectively, these five countries shape the backbone of the global orange and orange juice supply.

Brazil

Brazil’s 2025/26 Orange Contracts Await Finalization as Fruit Quality Improves

In Brazil, the 2025/26 orange season is progressing toward contract finalizations following Fundecitrus’s May estimate of 314.6 million 40.8-kilogram (kg) boxes, with most agreements expected from mid-Jun-25 onward. The bulk of production stems from the second blossoming phase, pointing to widespread harvesting starting after July. Meanwhile, industry purchases remain limited to volumes from earlier contracts or spot market transactions, contributing to modest price fluctuations in May-25. Favorable weather has supported improved fruit quality this season, which could reduce the volume of fruit needed for juice production, offering potential efficiency gains for processors.

Spain

Spain’s Orange Harvest Ends Early as Yields Fall and Demand Remains Strong

Spain's 2025 orange harvest wrapped up earlier than usual in key regions like the Valencian Community and Andalusia, where yields were lower than expected due to persistent rainfall that affected fruit quality and reduced marketable output. Despite this, strong demand, driven by cool spring weather, limited Egyptian supply, and a delayed stone fruit season, helped maintain high prices through the latter part of the campaign. With Spain’s harvest completed, European buyers are now turning to the Southern Hemisphere for supply, anticipating arrivals in the coming weeks that are likely to sustain elevated market prices.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W23 2024 to W23 2025)

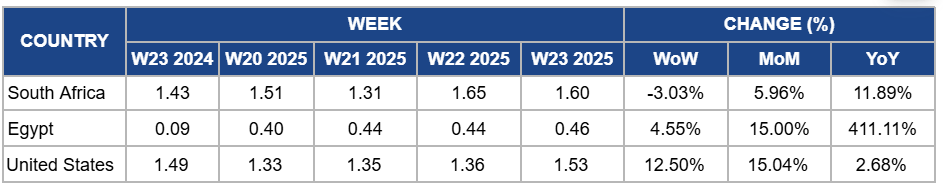

South Africa

South Africa’s orange prices dropped by 3.03% WoW to USD 1.60/kg in W23 due to a slight uptick in local market volumes following the easing of supply-chain challenges and a brief improvement in weather that led to better harvest delivery to fresh‑produce markets. However, on an MoM and YoY basis, prices still rose by 5.96% and 11.89%, respectively, driven by persistent tight overall supply, stemming from adverse weather (dry spells, frost, and storms) that reduced crop yields, strong demand from juice‑processing plants fueled by soaring global orange‑juice futures, and export diversions to more profitable markets, all of which kept fresh‑fruit availability constrained.

Egypt

In Egypt, orange prices increased by 4.55% WoW to USD 0.46/kg in W23, with a sharp 15% MoM rise and a staggering 411.11% YoY surge. This surge was driven mainly by supply-side constraints, production fell nearly 12 to 20% in 2024/25 due to heatwaves, irregular rainfall during critical flowering stages, and erratic weather last season. Export volumes also declined by 5%, further tightening local availability. Meanwhile, strong international demand, especially for processing oranges amid soaring juice prices, prompted Egypt’s growers to divert more fruit to juice production, worsening fresh-market shortages. Shipping challenges from Red Sea disruptions forced rerouting, increased export costs, and reduced volumes available locally. All these factors combined to push local orange prices sharply higher in W23.

United States

Orange prices in the US surged by 12.50% WoW to USD 1.53/kg in W23, with a 15.04% MoM rise and a modest 2.68% YoY increase. The sharp weekly uptick was driven by tightening fresh-fruit supplies. Florida's orange output continues to struggle due to citrus greening disease, hurricane recovery challenges, and orchard acreage reductions in favor of real estate. Meanwhile, the ongoing shortage prompted increased reliance on California and imported oranges, but processing capacity constraints and higher costs, from labor and logistics, further strained overall availability and put upward pressure on wholesale prices. Despite softer consumer demand in juice markets due to elevated retail prices, the tight supply balance has maintained pressure on fresh orange prices, underlining why YoY gains have stayed in positive territory.

3. Actionable Recommendations

Strengthen Alternate Market Planning During Tight Supply

Orange producers should actively identify and secure alternate export markets early in the season to maximize returns during periods of tight global supply. Producers in Spain, Egypt, the US, and South Africa can prioritize building relationships with buyers in Asia and the Middle East, where demand is growing and competition may be lower. For example, packing houses can pre-negotiate flexible contracts with multiple regional importers or explore niche segments like premium juice-grade fruit for processors. This approach reduces dependence on saturated EU markets and helps maintain stable sales when weather or competitor delays shift buyer attention.

Optimize Juice Yields Through Quality-Based Harvest Planning

Orange producers should coordinate harvest schedules with processors to prioritize groves showing superior fruit quality for early juice delivery. This allows processors to extract more juice per fruit, cutting down processing volumes and costs. For example, growers in Brazil, South Africa, or Florida can use maturity and brix-acid ratio testing to identify high-juice-yield blocks and align harvest timing accordingly. By tightening collaboration with juice buyers and staggering harvests based on quality data, producers can secure better contract terms and reduce post-harvest losses.

Sources: Tridge, Adda24/7, Citrus Industry, FoodbusinessAfrica, Fontestad, Freshfruitportal, Freshplaza