In W23 in the soybean oil landscape, some of the most relevant trends included:

- India’s soybean oil imports surged 10.4% MoM in May-25 to 398,585 mt, driven by low domestic inventories, reduced import duties, and palm oil’s deeper discount. Total vegetable oil imports hit a 5-month high at 1.19 mmt.

- Argentina’s soybean oil prices rose WoW in W23 due to tight supply, strong Indian and Nepali demand, and improved domestic processing after Vicentin’s plant reopened, boosting export capacity and price premiums.

- In contrast, US soybean oil prices fell WoW, pressured by favorable planting and South American supply. However, medium-term support remains from biofuel demand and global tightness in alternative vegetable oils.

1. Weekly News

India

India’s Soybean Oil Imports Hit 4-Month High in May-25

India’s soybean oil imports rose 10.4% month-on-month (MoM) in May-25 to 398,585 metric tons (mt), the highest since Jan-25, amid low domestic inventories and competitive palm oil prices. Although palm oil led the surge due to its deeper discount to soybean oil and sunflower oil, soybean oil still contributed significantly to the 33% overall increase in India’s vegetable oil imports, which reached 1.19 million metric tons (mmt), the highest since Dec-25. Soybean oil imports are expected to remain steady at around 400 thousand mt in Jun-25, with continued support from India’s recent 50% cut in import duties on crude edible oils to lower food prices and aid refiners.

Malaysia

Soybean Oil Regains Premium Over Palm Oil, but Gap Expected to Narrow by Sept-25

Soybean oil has regained a price premium over crude palm oil (CPO) after five months of parity, with the gap expected to narrow by Sept-25 as seasonal production picks up. While palm oil's price competitiveness has recently driven higher Indian imports and may attract Chinese buyers, soybean oil remains supported by strong demand from the United States (US) biofuel sector. Furthermore, the ongoing US-China trade tensions have shifted China’s sourcing from the US to Brazil, tightening US supply and lending further support to soybean oil prices, especially in Malaysia

United States

USDA Lowered 2024/25 Soybean Oil Biofuel Use, Maintains 2025/26 Forecast

In its Jun-25 World Agricultural Supply and Demand Estimates (WASDE) report, the United States Department of Agriculture (USDA) maintained its 2025/26 forecast for soybean oil use in biofuel production at 13.9 billion pounds (lbs). However, it revised its 2024/25 estimate downward from 13.1 to 12.9 billion lb, slightly below the 12.99 billion lb used in 2023/24. The outlook for 2025/26 United States (US) soybean supply, use, and prices remained unchanged, with soybean prices forecast at USD 10.25/bushel, soybean meal at USD 310/mt, and soybean oil at USD 0.46/lb. Globally, soybean beginning stocks were raised by 1 mmt due to a reduction in China’s prior-year crush. Meanwhile, soybean crush was increased by 100 thousand mt due to stronger demand in Pakistan, South Africa, and the United Kingdom (UK). With exports unchanged, global ending stocks were lifted to 125.3 mmt, mainly on higher stocks in China.

2. Weekly Pricing

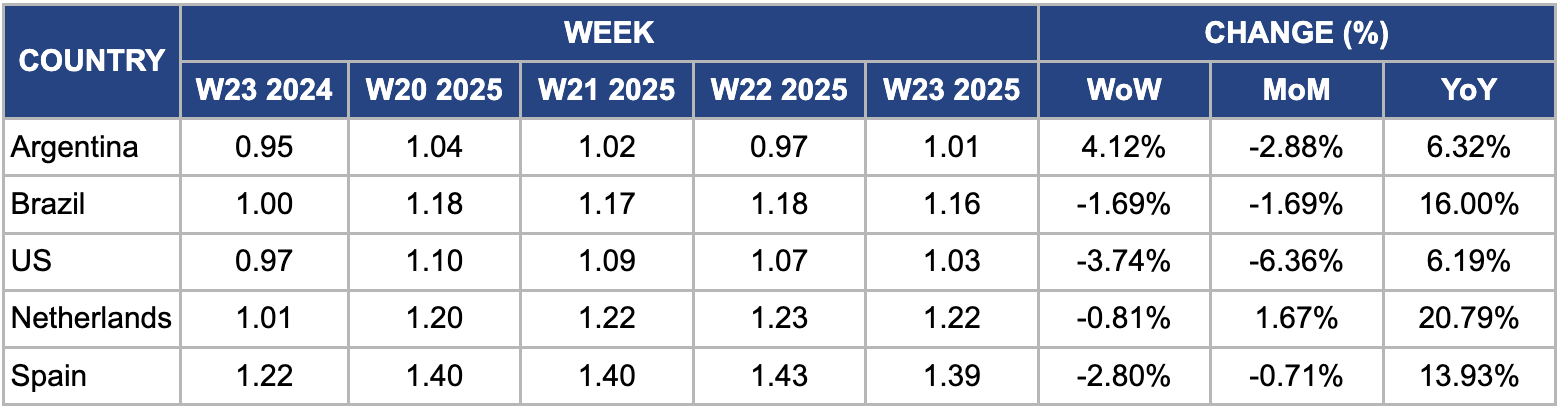

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W23 2024 to W23 2025)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Argentina

In W23, Argentina's wholesale soybean oil prices increased by 4.12% week-on-week (WoW) to USD 1.01 per kilogram (kg) from USD 0.97/kg in W22. This rise was driven by tight domestic supplies and strong international demand, particularly from major importers like India and Nepal, which turned to Argentine supplies following recent duty hikes on competing oils such as palm and sunflower. Moreover, soybean oil premiums in Argentina rose above US basis levels for the first time since 2022, reflecting tight availability and rising export interest. The recent reopening of the Vicentin crushing plant also contributed to higher processing capacity, increasing the volume of oil available for domestic use and export. Furthermore, favorable crush margins and continued biodiesel blending mandates have supported steady demand, helping maintain upward pressure on prices despite broader volatility in global vegetable oil markets.

Brazil

In W23, Brazil's soybean oil prices declined 1.69% WoW and month-MoM to USD 1.16/kg, mainly due to abundant domestic supply and reduced export availability. Brazil’s 2024/25 soybean crush reached record levels, with nearly 12 mmt of oil produced, driven by strong demand from the biodiesel sector, which absorbed a significant portion of the output. As a result, soybean oil exports will decline by 16% YoY from 1.55 mmt to 1.3 mmt. Despite Brazil producing a near-record soybean crop of approximately 166.3 to 170.9 mmt, the prioritization of biodiesel blending (B14) over external sales limited oil supply to international markets. Moreover, increased global competition from other vegetable oil producers weighed on export prices, contributing to the overall decline in Brazil’s soybean oil price.

United States

In W23, US soybean oil prices fell 3.74% WoW and 6.36% MoM to USD 1.03/kg but remained 6.19% higher year-on-year (YoY). The short-term price drop was due to favorable US planting conditions and abundant South American supplies, which dampened market sentiment. However, strong global demand and tight availability of substitute vegetable oils supported prices. According to the Food and Agriculture Organization (FAO), global vegetable oil prices rose 2.3% MoM in Apr-25, mainly due to soybean and rapeseed oil. Still, Argentina’s more competitive soybean oil export prices are expected to limit US price recovery in the short term. Looking ahead, the USDA projects record global soybean output and increased crush in 2025/26, while a potential rebound in biodiesel demand and improved trade flows may offer medium-term price support.

Netherlands

In W23, soybean oil prices in the Netherlands slightly decreased by 0.81% WoW to USD 1.22/kg due to ample global supply and weaker demand from the biodiesel sector within the European Union (EU). South American countries, especially Brazil and Argentina, continued to ship large volumes of soybean oil following strong harvests, leading to oversupply in the global market. At the same time, EU biodiesel producers, a key demand segment, reduced their procurement due to high stock levels and lower blending margins, further pressuring prices.

Spain

In W23, soybean oil prices in Spain decreased by 2.80% WoW to USD 1.39/kg from USD 1.43/kg due to ample import supply from South America, particularly Brazil and Argentina, which kept local inventories high and pressured wholesale prices. At the same time, domestic demand weakened, especially from the biodiesel sector, as major Spanish fuel producers increasingly shifted toward hydrotreated vegetable oil (HVO), reducing reliance on conventional soybean oil. Furthermore, steady crushing activity focused more on exports than local consumption, further contributing to a mild domestic oversupply and driving prices down.

3. Actionable Recommendations

Diversify Export Markets for Major Producers like Brazil and Argentina

Brazil and Argentina, as top global suppliers of soybean oil, should proactively diversify their export destinations beyond traditional markets like India and the EU. This includes negotiating trade agreements, reducing non-tariff barriers, and participating in food trade expos targeting emerging economies such as Bangladesh, Pakistan, Egypt, and Sub-Saharan Africa. Exporters should also consider developing logistics and marketing strategies tailored to these new regions. By tapping into underutilized or growing demand in alternative markets, producers can secure more stable revenue streams, mitigate the impact of trade restrictions or price competition from rivals, and maintain export volumes even when key buyers reduce purchases.

Invest in Domestic Biodiesel Infrastructure in Import-Dependent Countries

Import-reliant countries such as India and EU members should accelerate investment in local biodiesel production facilities that use soybean oil as feedstock. This includes offering subsidies or tax incentives to refiners, mandating higher blending rates, and supporting R&D for more efficient biodiesel technologies. Encouraging public-private partnerships can also help scale up production quickly. This will enhance domestic demand for soybean oil, reduce overdependence on palm oil, and create long-term stability in vegetable oil supply chains. It also aligns with climate goals by promoting renewable energy and supports job creation within rural and industrial sectors.

Establish Regional Strategic Reserves of Edible Oils

Governments in major import-dependent countries such as India and China should establish or expand strategic reserves for edible oils like soybeans. These reserves can be activated during periods of price spikes or supply disruptions. To ensure efficiency, governments should work with private sector partners for warehousing and rotation systems to avoid spoilage. A well-managed reserve provides a buffer that helps stabilize domestic prices, improves food security, and reduces vulnerability to global market shocks such as export bans, weather-related crop failures, or geopolitical conflicts affecting supply routes.

Sources: Tridge, Bio Mass Magazine, Market Screener