In W23 in the tomato landscape, some of the most relevant trends included:

- Kazakhstan faced export rejections from Russia over virus concerns.

- Meanwhile, Mexico and the US are embroiled in a trade dispute, with the US imposing a 17.09% anti-dumping duty on Mexican tomatoes, impacting export revenues and market stability.

- Tomato prices rose WoW in Morocco, France, and Mexico, but declined in Spain and Türkiye due to increased harvest volumes and easing demand. Meanwhile, Almería’s seasonal tomato pricing showed volatility driven by shifting supply dynamics and intensified international competition.

1. Weekly News

Kazakhstan

ToBRFV Dispute Emerges as Russia Returns 46 MT of Kazakh Tomatoes

In late May-25, Russian authorities returned 46 metric tons (mt) of tomatoes exported by a Kazakhstani company, citing suspected contamination with Tomato brown rugose fruit virus (ToBRFV). However, Kazakhstan’s Agriculture Ministry stated that accredited national laboratories, including the Central laboratory in Astana, conducted comprehensive testing and found no trace of the virus. Russia’s Rosselkhoznadzor office in Omsk had flagged three shipments in total, including a 15-mt batch of Merlis tomatoes that they returned after initially clearing it, along with two more shipments totaling 31 mt. Despite these incidents, Kazakhstan exported 317.7 mt of tomatoes to Russia since mid-May-24, and authorities rejected only these three batches without reporting any prior quarantine violations.

Nigeria

Nigeria’s Tomato Market Strained by 'Tomato Ebola', Rising Fuel Costs, and Supply Gaps

The Tomato Out Growers Association of Nigeria (TOGAN) has attributed the recent surge in tomato prices to a combination of seasonal scarcity, pest outbreaks, and rising transportation costs. The ongoing off-season has led to a significant drop in tomato supply, a trend expected to persist until the new harvest begins on Sept-25. Households are feeling the pinch, forced to spend more on tomatoes amid slow production recovery. The National TOGAN President further explained that an outbreak of Tuta Absoluta, commonly known as “tomato ebola”, has severely damaged farms across key producing states like Kano, Kaduna, and Jos, worsening the supply crisis. Moreover, logistical bottlenecks, including rising fuel prices and bribes at checkpoints, have inflated transport costs, further driving up retail prices. Despite efforts to restore farming activity, these overlapping challenges continued straining Nigeria’s tomato market.

Spain

Almería’s 2024/25 Greenhouse Tomato Prices Show Volatile Trends Across Season

As Almería's greenhouse fruit and vegetable season nears its end, weekly auction data highlights significant price fluctuations in the region’s key tomato varieties, particularly long-life tomatoes. The season began on Sept-24, with an average price of USD 1.20 per kilogram (kg), peaking in Oct-24 at USD 1.42/kg, the highest monthly value of the season. However, prices declined to USD 1.13/kg in Nov-24 and to USD 1.07/kg in Dec-24, reflecting increased supply and reduced European demand heading into winter. A brief rebound occurred on Jan-25, with prices rising to USD 1.34/kg, likely driven by tightened supply during colder weather. Yet, this recovery was short-lived, as Feb-25 saw a sharp drop to USD 0.92/kg amid competition from Moroccan imports and stabilizing logistics. By Mar-25 and Apr-25, prices recovered modestly to USD 0.98/kg, supported by steady demand and the gradual winding down of the local season.

United States

US Tomato Trade at Risk Amid Policy Shift

Tomato is among the most widely consumed vegetables in the United States (US), with fresh tomato imports often taking the top spot alongside avocados. This critical trade flow is now under threat due to the President's administration’s revival of longstanding efforts to restrict imports. According to economists specializing in agricultural trade, imported tomatoes play a vital role in ensuring year-round availability, stabilizing prices, and sustaining billions of dollars in economic activity and thousands of jobs across the US supply chain. Fresh tomato imports help fill the gap that domestic production alone cannot meet, and trade limitations could lead to reduced consumer access, higher prices, and job losses across related industries. Efforts to correct trade imbalances by imposing new restrictions may backfire, causing harm to the broader economy than the perceived benefits of protecting local producers.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

* Varieties: All tomato pricing is for round tomatoes

Yearly Change in Tomato Pricing Important Exporters (W23 2024 to W23 2025)

* Varieties: All tomato pricing is for round tomatoes

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

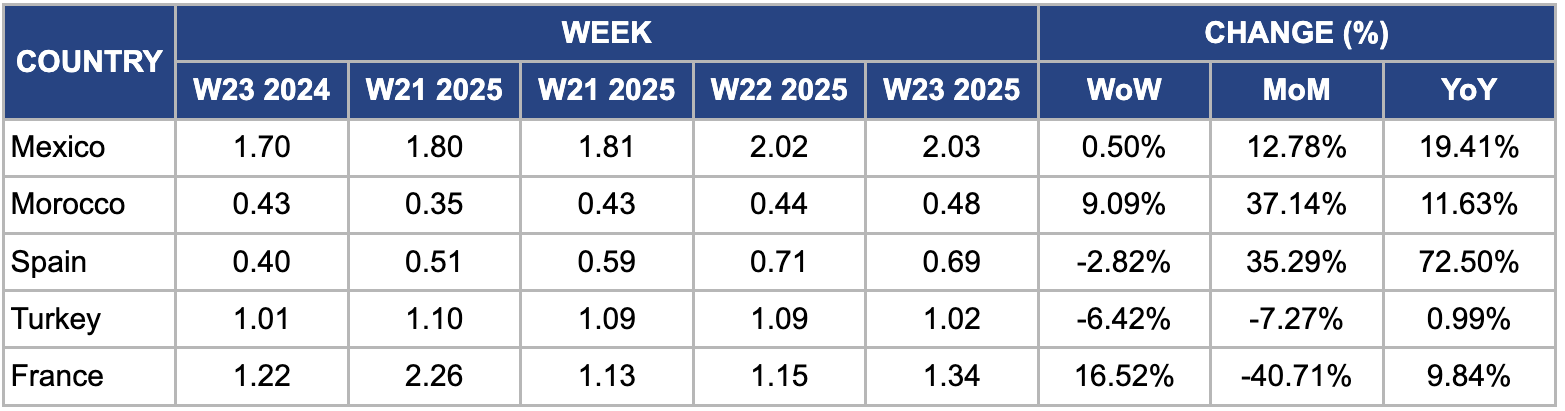

Mexico

In W23, Mexican tomato prices rose slightly by 0.50% week-on-week (WoW) to USD 2.03/kg, with sharper increases of 12.78% month-on-month (MoM) and 19.41% year-on-year (YoY). These price movements largely reflect growing trade uncertainty following the US decision to impose a 17.09% anti-dumping duty on Mexican tomatoes starting July 14, 2025. The announcement has already contributed to a 3.2% decline in Mexican agricultural exports and a 7.8% drop in tomato export revenues, which fell to USD 859 million in early 2025. Since over 50% of Mexico’s tomato production is exported to the US, a market that depends on Mexico for nearly 70% of its fresh tomato imports, the pending tariff poses serious risks to price stability and the economic vitality of key producing regions like Baja California.

Morocco

In W23, Morocco’s tomato prices increased by 9.09% WoW and 37.14% MoM to USD 0.48/kg, mainly due to production shortfalls and strong export demand. According to local agricultural sources, key producing regions such as Souss-Massa experienced prolonged drought and higher-than-average temperatures, which stressed plants and led to a 15% YoY drop in national tomato output compared to 2024. This weather-induced decline in yields directly reduced volumes available for domestic markets. Furthermore, ongoing labor shortages aggravated during the peak harvest window slowed harvesting operations, especially in regions where manual labor is critical due to limited mechanization. On the demand side, heightened interest from European buyers, particularly from France and Spain, has pulled more supply into export channels as Moroccan exporters seek higher returns in foreign markets.

Spain

In W23, Spain’s wholesale tomato prices eased by 2.82% WoW to USD 0.69/kg, down from USD 0.71/kg in W22. This slight price dip was driven by a modest increase in supply as planting progressed in regions such as Andalusia, aided by recently improved weather in early Jun-25. However, longer-term challenges are weighing in: Spanish tomato output has fallen nearly 19% over the past decade, from about 4.89 mmt in 2014 to around 3.97 mmt in 2024, indicating a structural decline in production. Moreover, import competition from lower-cost producers like Morocco and the Netherlands, who now account for most of Spain’s fresh tomato imports, adds pricing pressure.

Türkiye

In W23, Türkiye's tomato prices declined 6.42% WoW and 7.27% MoM to USD 1.02/kg as post-peak domestic demand eased and early-season harvests gradually boosted supply. Favorable weather in key growing areas like Antalya and Mersin supported consistent crop development, helping stabilize market conditions. Despite the modest price decline, levels remained slightly higher compared to W23 2024, mainly due to persistent challenges such as elevated input costs and logistical inefficiencies affecting supply chain operations.

France

In W23, France’s tomato prices rose by 16.52% WoW to USD 1.34/kg, driven by delayed production and steady demand. A cooler-than-normal spring in major producing regions like Brittany and Provence pushed back the start of the greenhouse harvest by 7 to 10 days, curbing early-season volumes. This seasonal delay compounded structural issues such as ongoing labor shortages, especially in harvesting and post-harvest handling, further constrained supply entering the market. On the demand side, consumption remained strong from retailers and food service providers ahead of the summer, tightening market conditions. This imbalance between lagging supply and steady demand led to the notable price increase recorded in W23.

3. Actionable Recommendations

Strengthen Kazakhstan–Russia Phytosanitary Coordination

Kazakhstan should establish a joint phytosanitary surveillance and certification mechanism with Russia to prevent future rejections of tomato shipments with contamination concerns such as ToBRFV. Although Kazakh authorities confirmed the safety of rejected shipments through accredited labs, the lack of mutual trust and protocol alignment with Russia’s Rosselkhoznadzor led to unnecessary trade disruptions. Creating a bilateral framework that includes pre-export inspections, certified lab networks, and digital traceability systems would improve transparency and reliability. This initiative would safeguard Kazakhstan’s tomato exports and reinforce its position as a credible agri-exporter in the region.

Scale Up Climate and Pest-Resilient Tomato Varieties in Nigeria and Morocco

To counter production disruptions caused by pests and extreme weather, Nigeria and Morocco should urgently scale up the deployment of climate-resilient and pest-tolerant tomato varieties. In Nigeria, the outbreak of Tuta absoluta ("tomato ebola") has devastated farms in major producing regions, driving up prices and reducing supply. Distributing resistant seed varieties, introducing pheromone traps, and training farmers in integrated pest management (IPM) can drastically reduce losses. Promoting drought-tolerant and heat-resilient varieties adapted to local growing conditions can stabilize production and ensure a steady domestic and export supply.

Diversify Mexico’s Export Markets Amid Rising US Trade Barriers

With the US set to impose a 17.09% anti-dumping duty on Mexican tomatoes starting Jul-25, Mexico must reduce its dependence on the US market, which accounts for over 70% of its fresh tomato exports. A strategic export diversification plan should target alternative high-value markets such as Canada, the United Kingdom (UK), and the Gulf Cooperation Council (GCC) countries. Investment in cold chain infrastructure and marketing initiatives like regional branding such as Baja Vine-Ripe Tomatoes can help Mexican producers tap into premium retail segments abroad. These actions will mitigate immediate tariff-related losses and build long-term market resilience.

Sources: Tridge, Horti Daily, Fresh Plaza, The Conversation