.jpg)

In W23 in the wheat landscape, some of the most relevant trends included:

- In 2025, wheat output is forecast to decline in Australia by 10% YoY and China by 5% YoY due to prolonged drought and high temperatures affecting key growing regions.

- Iraq has regained self-sufficiency in production, supported by strong yields and subsidies, while Turkmenistan maintains stable production targets despite continued flour imports.

- Russia’s 2024/25 wheat exports are forecasted to drop by nearly 20% YoY, driven by weak shipments in early 2025, logistical challenges, and a stronger RUB.

- The US reports improved crop conditions, with 52% of winter wheat rated good to excellent. Progress is slightly behind last year but on par with the five-year average.

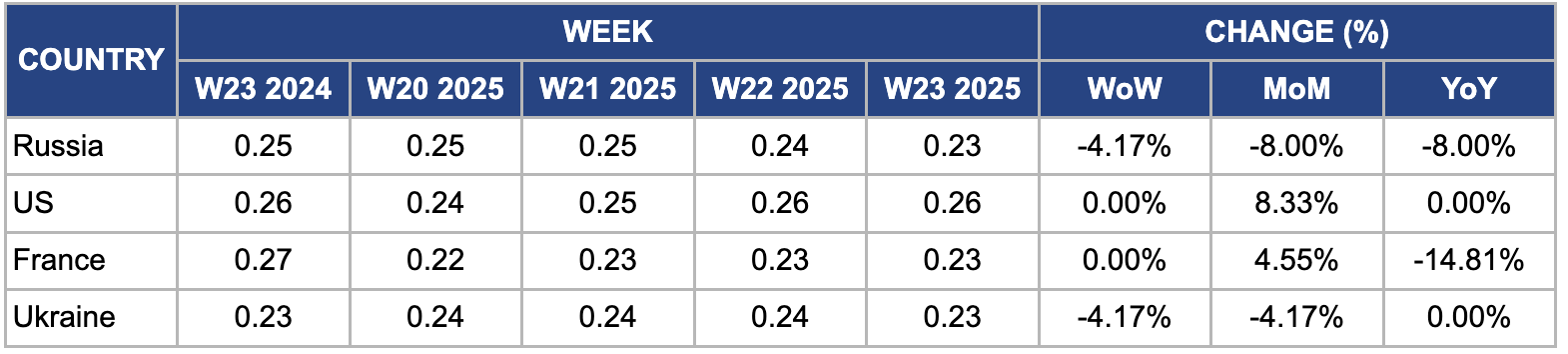

- In W23, wheat prices declined WoW in Russia due to projected record harvest. Meanwhile in Ukraine prices fell due to increased supply. In contrast, US FOB prices rose MoM due to harvest delays, tighter supply concerns, and firm international demand.

1. Weekly News

Australia

Australia’s 2025 Wheat Output Expected to Drop 10% YoY Amid Dry Conditions

Australia's wheat production is forecasted to decline by 10% year-on-year (YoY) to 30.6 million metric tons (mmt) in 2025 due to dry conditions in key growing areas. Despite the declines, production remains above the 10-year average. Reduced planting in southern New South Wales (NSW), Victoria, South Australia, and Western Australia (WA) reflects poor soil moisture, with many crops now relying on June rains to germinate. Meanwhile, crop conditions in Queensland, northern NSW, and southern WA are more favorable, and forecasts suggest above-average winter rainfall could support yield potential if forecasts hold.

China

China's 2025 Wheat Harvest Expected to Drop to 6-Year Low Amid Drought and Heatwave

China's 2025 wheat harvest will drop by 5% YoY from 135 to 133mmt, the lowest since 2018 due to prolonged drought and high temperatures in key farming regions. While emergency irrigation has helped mitigate some losses, farmers await rain to plant corn. Despite the lower output, analysts expect no key wheat shortage thanks to high stockpiles and weak domestic demand. Still, the situation raises concerns for China’s food security strategy. The government is providing emergency support, but pest outbreaks and increased irrigation costs are adding pressure on already low-margin farms.

Iraq

Iraq Declares Wheat Self-Sufficiency in 2025 Amid Surplus and Strategic Reserves

According to Iraq’s Trade Minister, the country has regained self-sufficiency in wheat production, citing robust yields supported by government subsidies and favorable rainfall. Due to surplus production of 1.5 mmt, strategic reserves now exceed 5.5 mmt, enough to meet national demand for a year. The government continues to pay farmers over twice the global market price to maintain production in arid regions. Iraq previously achieved self-sufficiency between 2019 and 2021 but faced setbacks due to water shortages and desertification.

Russia

Russia’s 2024/25 Wheat Exports to Drop Nearly 20% Due to Logistical and Market Pressures

Russian wheat exports in the 2024/25 marketing year (MY) will decline by 19.8% YoY to 41.7 mmt, primarily due to a sharp decline in shipments in the latter half of the season. Shipments plummeted 40% YoY from Jan-25 to Apr-25. Contributing factors include low stocks in southern regions, high railway tariffs, a stronger ruble (RUB), and falling global prices. Although the government raised export quota limits, only 76.4% of the original quota was utilized, and experts remain skeptical about the profitability of further exports.

Turkmenistan

Turkmenistan Launches 2025 Winter Wheat Harvest With 1.4 MMT State Target

Turkmenistan has started its 2025 winter wheat harvest, aiming to collect 1.4 mmt from 690 thousand hectares (ha), matching 2024's target. Harvesting is underway, with the remaining regions set to begin in a week due to changing climatic conditions. While officials claim the state target will meet national wheat needs, imported flour from Russia, Kazakhstan, and other countries remains available in local markets.

United States

US Winter Wheat Planting Progresses Ahead of Average

As of June 1, the United States Department of Agriculture (USDA) reports that 83% of the United States (US) winter wheat crop was planted, slightly ahead of 2024 progress and the five-year average. Harvesting has begun on 3% of the area, lagging 2% behind last year but on par with the five year average. Crop conditions have improved, with 52% rated good to excellent, an increase from W22. In Kansas, the top-producing state, 51% of the crop was rated good to excellent.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W23 2024 to W23 2025)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Russia

In W23, Russian FOB wheat prices fell by 4.17% week-on-week (WoW), 8% month-on-month (MoM), and 8% YoY to USD 0.23 per kilogram (kg), driven by expectations of a record 2025 harvest projected at 88 mmt, supported by favorable weather and expanded planting. Government-imposed export quotas at 10.6 mmt from Feb-25 to Jun-25 have boosted domestic supply, putting further downward pressure on prices. At the same time, the strengthening RUB has reduced export competitiveness, while rising production and logistical costs continue to erode exporter margins, compounding the bearish sentiment in the Russian wheat market.

United States

In W23, US FOB wheat prices held steady WoW, but increased 8.33% MoM to USD 0.26/kg, an increase from USD 0.24/kg in W20, driven by concerns over tighter supplies amid delays in the winter wheat harvest caused by wetter-than-average conditions in key producing states such as Kansas and Oklahoma. Strong global demand, fueled by buyers seeking alternative suppliers amid geopolitical uncertainties, also supported prices. Furthermore, limited export competition from other major producers facing production setbacks contributed to the upward momentum in US wheat prices during this period.

France

In W23, wholesale wheat prices in France held steady WoW at USD 0.23/kg, supported by a reduced 2024/25 production estimate of 25.78 mmt due to slightly lower yields of 6.15 metric tons (mt) per ha caused by unfavorable weather. Despite this stability, prices were down 14.81% YoY as exports outside the European Union (EU) were forecasted at just 3.5 mmt, the lowest in decades due to weaker demand from key buyers like Algeria and China. Increased competition from major exporters such as Russia, offering cheaper wheat, further pressured the market by limiting France’s export potential and amplifying global supply, leading to a significant annual decline.

Ukraine

In W23, Ukrainian wheat prices declined 4.17% WoW and MoM to USD 0.23/kg, mainly due to increased domestic supply pressure and the seasonal slowdown in export activity. As the 2024/25 harvest approaches, traders are clearing old stock to make room for the new crop, contributing to price softening. Furthermore, logistical disruptions at Black Sea ports and competition from Russian and EU wheat in international markets have limited Ukraine's export opportunities, putting further downward pressure on prices. Expectations of a stable upcoming harvest, supported by favorable weather in key growing regions, also weighed on market sentiment.

3. Actionable Recommendations

Secure Long-Term Wheat Supply Contracts from the US

With US wheat prices holding steady, now is a strategic time to secure long-term supply contracts. The US crop condition has improved, particularly in Kansas, and buyers looking for consistent quality and reliability should act before tighter supplies and harvest uncertainties cause further price increases. Locking in contracts early can provide price stability and ensure uninterrupted supply amid ongoing geopolitical risks and weather-driven disruptions in other exporting countries.

Capitalize on Cheaper Russian and Ukrainian Wheat for Immediate Needs

Russian and Ukrainian wheat prices have declined due to seasonal supply pressure, reduced export activity, and growing domestic stock levels. These lower prices present a short-term cost advantage for importers seeking immediate supply. Buyers should consider securing spot volumes from these origins while prices remain subdued but remain mindful of logistical risks, particularly in Ukraine, where Black Sea port operations face ongoing challenges. Leveraging flexible shipping contracts and comprehensive insurance coverage can help mitigate these risks while capitalizing on the current pricing window.

Monitoring Weather Developments

Wheat production in Australia and China is projected to decline in 2025 due to dry weather, raising potential supply concerns later in the year. Australia’s reliance on Jun-25 rains for crop germination and China’s drought-affected yields could increase global prices if weather conditions deteriorate further. Buyers should closely monitor weather developments in these countries and consider advancing purchases or hedging positions before any negative revisions in production forecasts occur. This proactive approach can secure supply at lower prices ahead of market tightening.

Sources: Tridge, Agro Link, Hellenic Shipping News, UkrAgroConsult