In W24 in the apple landscape, some of the most relevant trends included:

- Brazil is expanding apple cultivation in South Minas Gerais, where growers supported by Emater-MG expanded orchard size. They target 60 mt in annual production to reduce reliance on imports and supply local programs like the PNAE.

- Chile forecasts a 13% YoY increase in apple exports for the 2025 season, reaching 576.9 thousand mt. Supported by favorable weather conditions, the growth is led by strong demand for Pink Lady and Fuji varieties..

- India is strengthening the apple industry in Himachal Pradesh by enforcing standardized packaging and improving cold storage access. It is also investing in infrastructure to support growers facing import pressure and climate risks.

- Ukraine is experiencing a 75% surge in apple prices due to low stock levels, rising transportation costs, and poor weather, with limited expectations for near-term relief.

1. Weekly News

Brazil

Brazil Expands Apple Cultivation in South Minas Gerais to Meet Local Demand

Apple cultivation is expanding in South Minas Gerais, Brazil, as 20 growers from Arceburgo, Areado, and Alfenas increase their orchards from 7.2 to 10.2 hectares (ha) with support from Emater-MG and the acquisition of 2 thousand seedlings. Focused on the Eva and Princesa varieties suited to local conditions, the initiative aims to produce up to 60 metric tons (mt) annually, with early harvests already yielding 30 mt. This development is helping reduce reliance on refrigerated imports while strengthening supply for local markets, including institutional buyers such as the National School Feeding Program (PNAE). To ensure long-term success, Emater-MG is training regional technicians and growers in pruning and crop management practices that promote sustainable and efficient production.

Chile

Chile Forecasts Stronger Apple Exports for 2025 Season

Chile projects apple exports to reach 576.9 thousand mt for the 2025 season, reflecting a 1% rise from the initial estimate and a 13% year-on-year (YoY) increase, supported by favorable weather that improved yield and fruit quality. Pink Lady apples are leading the growth with forecasted exports of 136.6 thousand mt, a 32% YoY increase. On the other hand, Fuji exports are expected to grow 5% to 61.4 thousand mt. In contrast, Gala shipments may decline by 4% to 238.7 thousand mt. Based on updated reports from producers and exporters covering most national shipments, these projections highlight Chile’s strong market position and the rising global demand for its premium apple varieties.

India

Himachal Pradesh Strengthens Apple Sector with Packaging Standards and Infrastructure Reforms

In Himachal Pradesh, India, authorities are enforcing standardized apple packaging by weight using standardized cartons to ensure fair pricing and prevent trader exploitation ahead of the new harvest. These efforts include legal enforcement of a 2019 packaging mandate, expanded cold storage access through decentralized infrastructure, and scientific yield assessments to improve transparency. As local growers face pressure from rising United States (US) apple imports and potential tariff adjustments, the government is cracking down on non-compliant traders and enhancing Agricultural Produce Market Committee (APMC) oversight. Additional support measures include subsidies for anti-hail nets and the USD 144 million HP Shiv Project, aimed at modernizing apple farming and shielding growers from climate and market risks.

Ukraine

Apple Prices Soar in Ukraine Amid Low Stocks and Rising Costs

Apple prices in Ukraine have jumped by 75% in recent weeks, with some varieties exceeding USD 2.40 per kilogram (UAH 100/kg). This sharp increase is driven by shrinking stockpiles from the last harvest, rising logistics costs, and continued adverse weather. While growers remain hopeful that the upcoming crop will ease supply pressure, analysts caution that prices are unlikely to fall significantly in the near term due to the scale of current constraints and the time needed for recovery.

2. Weekly Pricing

Weekly Apple Pricing Important Exporters (USD/kg)

Yearly Change in Apple Pricing Important Exporters (W24 2024 to W24 2025)

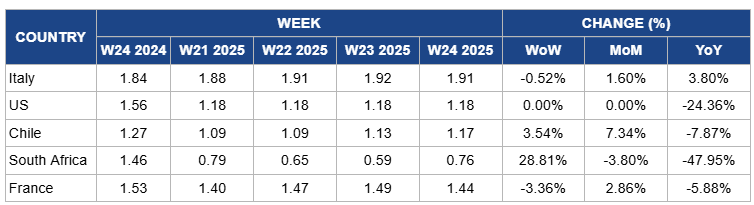

Italy

In Italy, apple prices slightly decreased by 0.52% week-on-week (WoW) to USD 1.91/kg in W24 due to subdued domestic demand and ample availability of stored apples from the previous harvest, which has kept short-term prices under mild pressure. However, prices increased by 1.60% MoM and 3.80% YoY due to lower overall production volumes from the 2024 harvest. This decline was caused by adverse weather conditions, particularly spring frosts and hail events, which limited supply and supported higher pricing trends over the medium to long term.

United States

US apple prices remained stable WoW and MoM at USD 1.18/kg in W24, with a 24.36% YoY decrease due to significantly higher apple production in the 2023/24 season, particularly in Washington state, the country’s top-producing region. Improved growing conditions, including favorable weather and fewer disease pressures, led to a bumper crop that boosted supply and pushed prices down compared to the previous year. Additionally, slower export demand and increased competition from imported apples have contributed to sustained downward pressure on prices.

Chile

Apple prices in Chile increased by 3.54% WoW to USD 1.17/kg in W24, with a 7.34% MoM increase due to reduced availability as the harvest season nears its end, tightening local supply and supporting higher prices. However, YoY prices decreased by 7.87% due to a larger overall crop in the 2024 season compared to the previous year, coupled with subdued export demand and strong international competition, particularly from Northern Hemisphere suppliers offering lower-priced fruit earlier in the year.

South Africa

In South Africa, apple prices rose by 28.81% WoW to USD 0.76/kg in W24 due to a temporary tightening of supply in the local market as harvest volumes decline toward the end of the picking season. However, MoM and YoY prices dropped by 3.80% and 47.95%, respectively, due to a larger overall crop this season. This increase in production was driven by favorable weather and improved yields, which have boosted cold storage volumes and intensified market competition, keeping long-term price levels significantly lower than the previous year.

France

France's apple prices decreased slightly by 3.36% WoW to USD 1.44/kg in W24, with a 5.88% YoY decrease. This decline was driven by continued high inventory levels from the 2024 harvest and sluggish domestic demand, particularly for older varieties still in cold storage, which are being sold at discounted rates to clear space. However, there is a slight increase in MoM prices of 2.86% due to the growing scarcity of premium-quality apples as the season progresses, along with steady demand from retail chains and export markets seeking consistent supply ahead of the summer fruit transition.

3. Actionable Recommendations

Boost Storage and Forward Contracting to Manage Price Volatility

Apple producers should invest in better-controlled atmosphere storage facilities and use forward contracting to manage tight off-season supply and reduce price spikes. Upgraded storage helps preserve quality and extend availability into high-price windows, while forward contracts with retailers or processors secure predictable returns. For example, producers in Poland, Ukraine, or northern India can use long-term cold storage to release apples strategically and sign price agreements before harvest to buffer against logistics cost surges.

Standardize Grading and Improve Market Access to Strengthen Price Leverage

Apple producers should adopt consistent grading and packaging standards based on weight and quality to ensure transparent pricing and reduce dependency on middlemen. For example, using uniform cartons and digital scales at farm-level collection points can help prevent underpayment. In parallel, producers in regions like Himachal, Poland, or Chile should build direct relationships with retailers and cooperatives to bypass traditional commission agents. Pooling volumes through grower associations can also increase bargaining power and ensure fairer market access.

Sources: Tridge, Abrafrutas, ANI News, Freshplaza, Kyiv1, Redagricola